Fraud Prevention Solution

Fraud Prevention Built for Speed, Precision and Scale

SEON connects 900+ first-party signals across digital footprint, device intelligence and behavioral data to automate real-time fraud decisions across the customer journey.

Trusted by the World’s Most Ambitious Companies

how seon stops fraud

Unified Fraud Detection & Prevention System

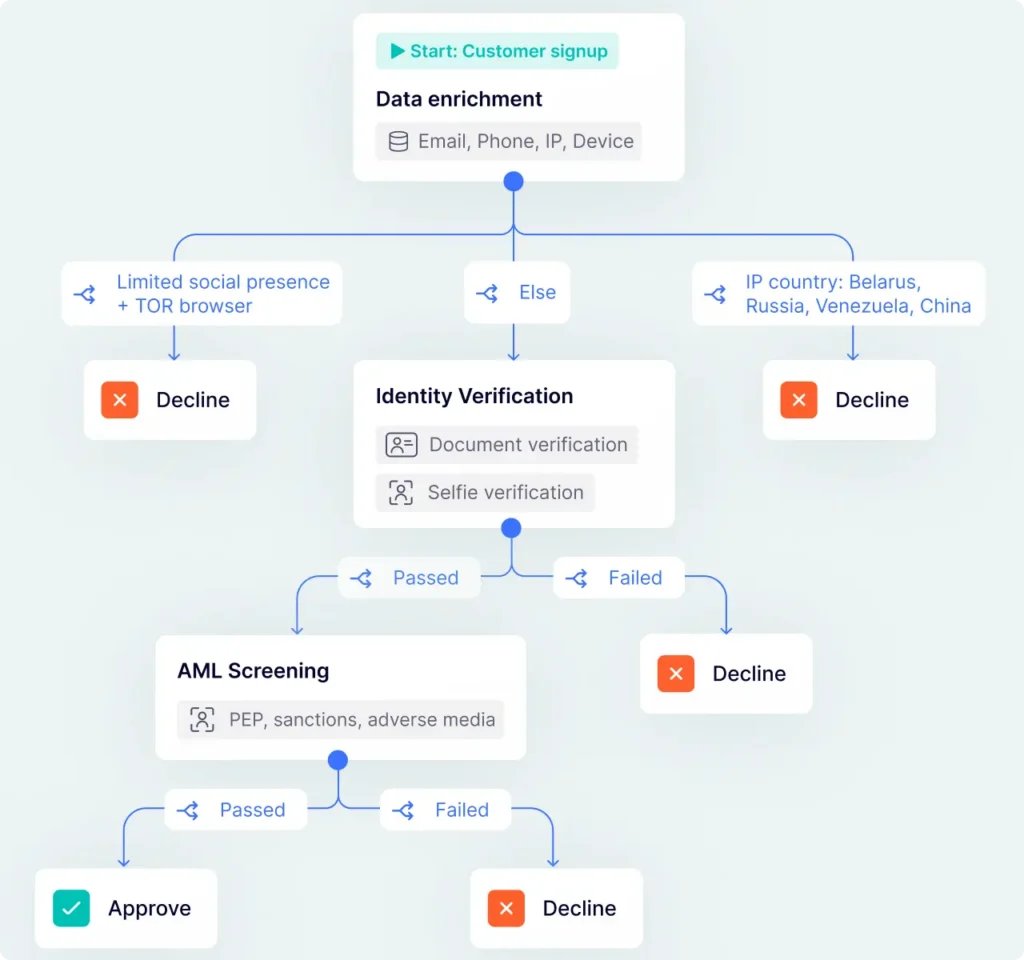

Pre-Screen Bad Actors Before KYC

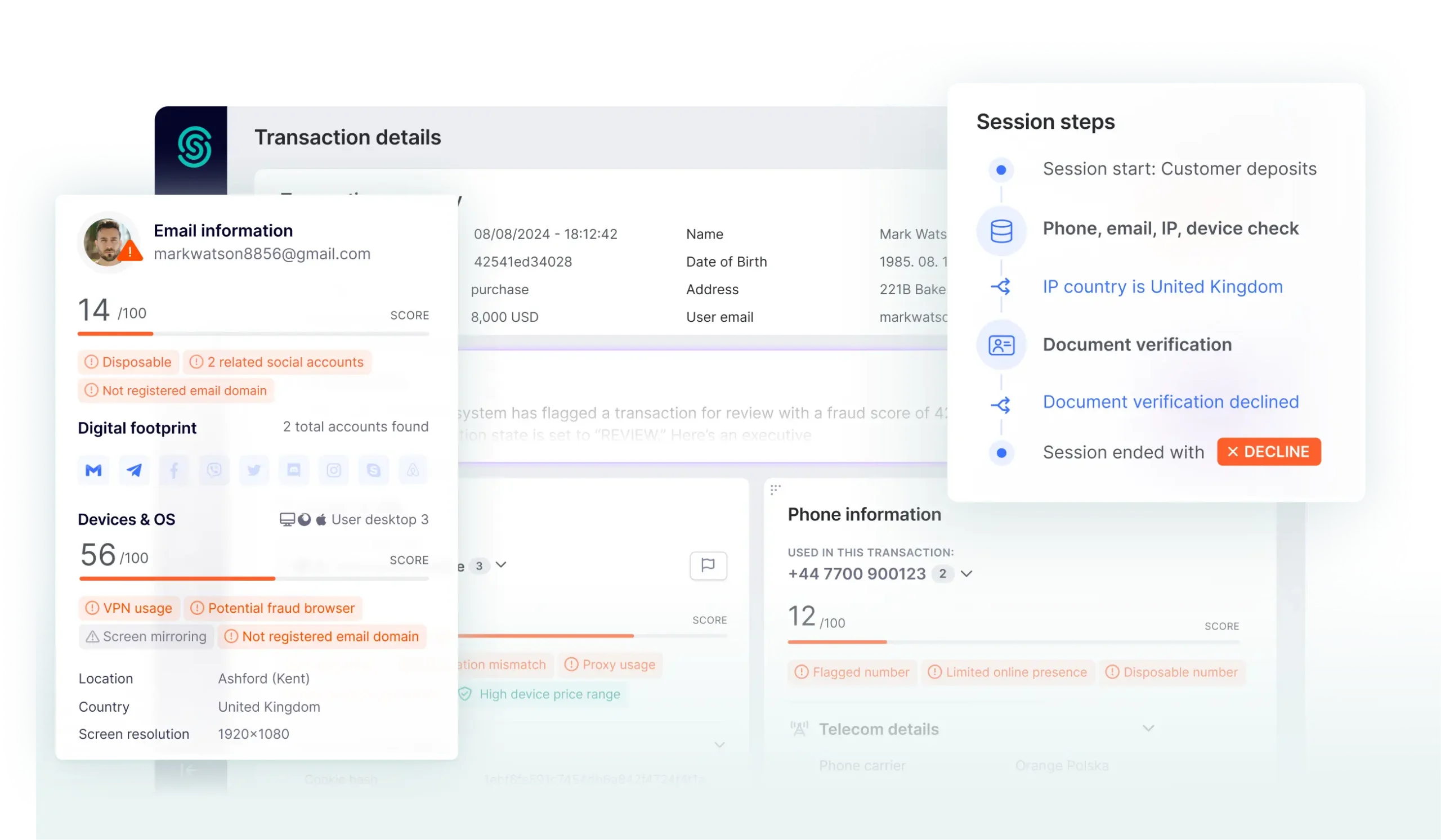

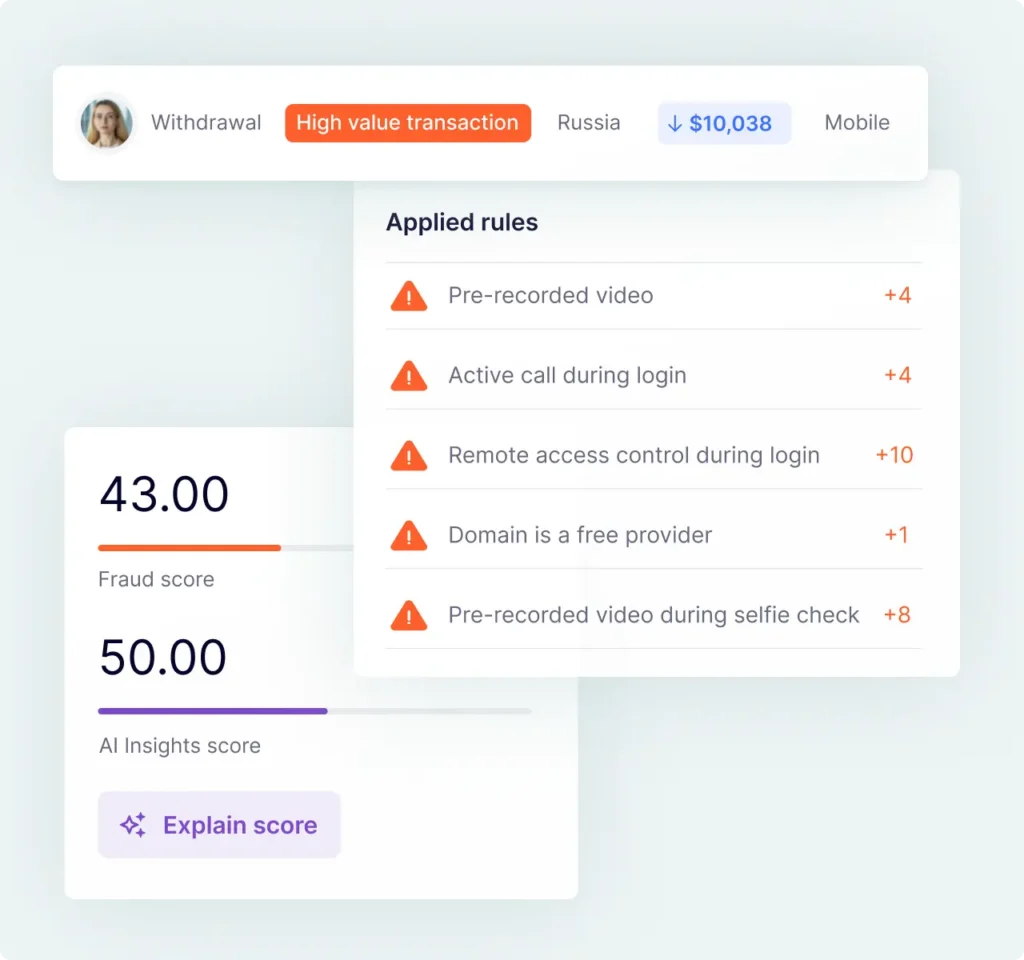

Detect Payment Fraud & Account Takeovers in Real-Time

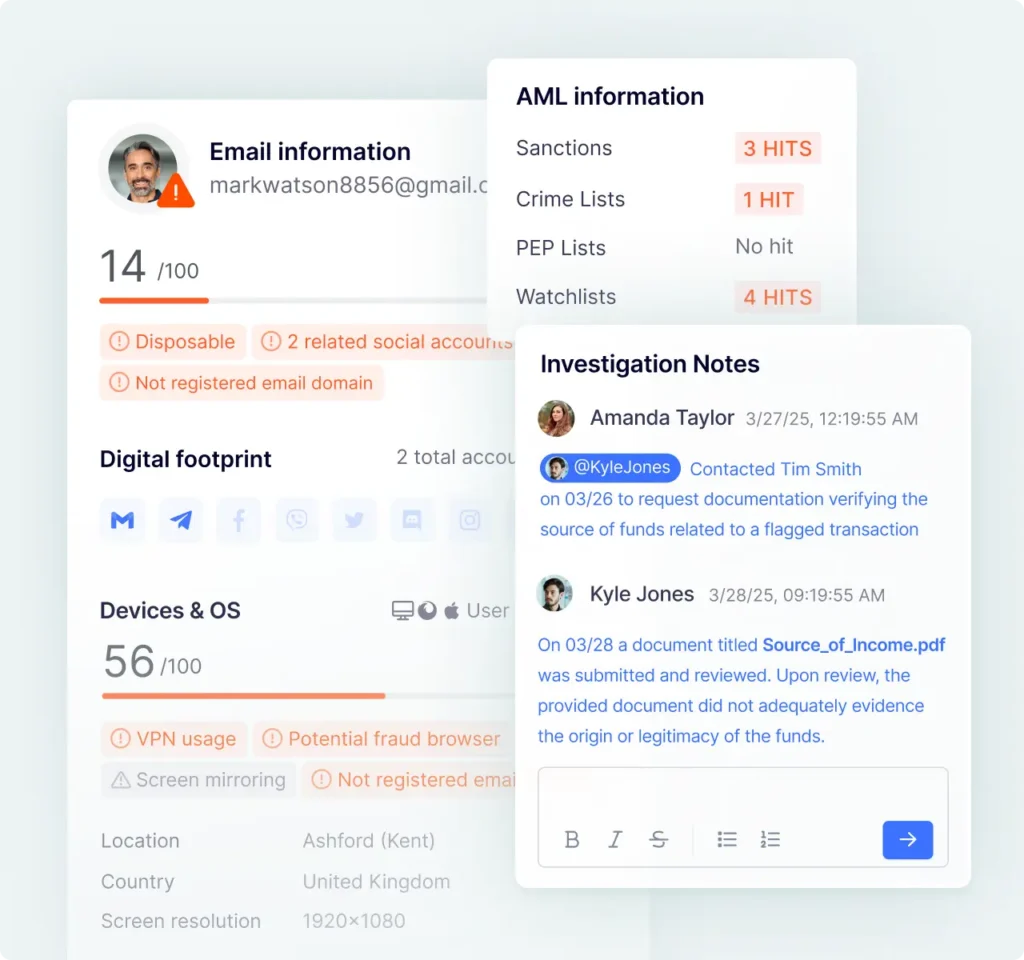

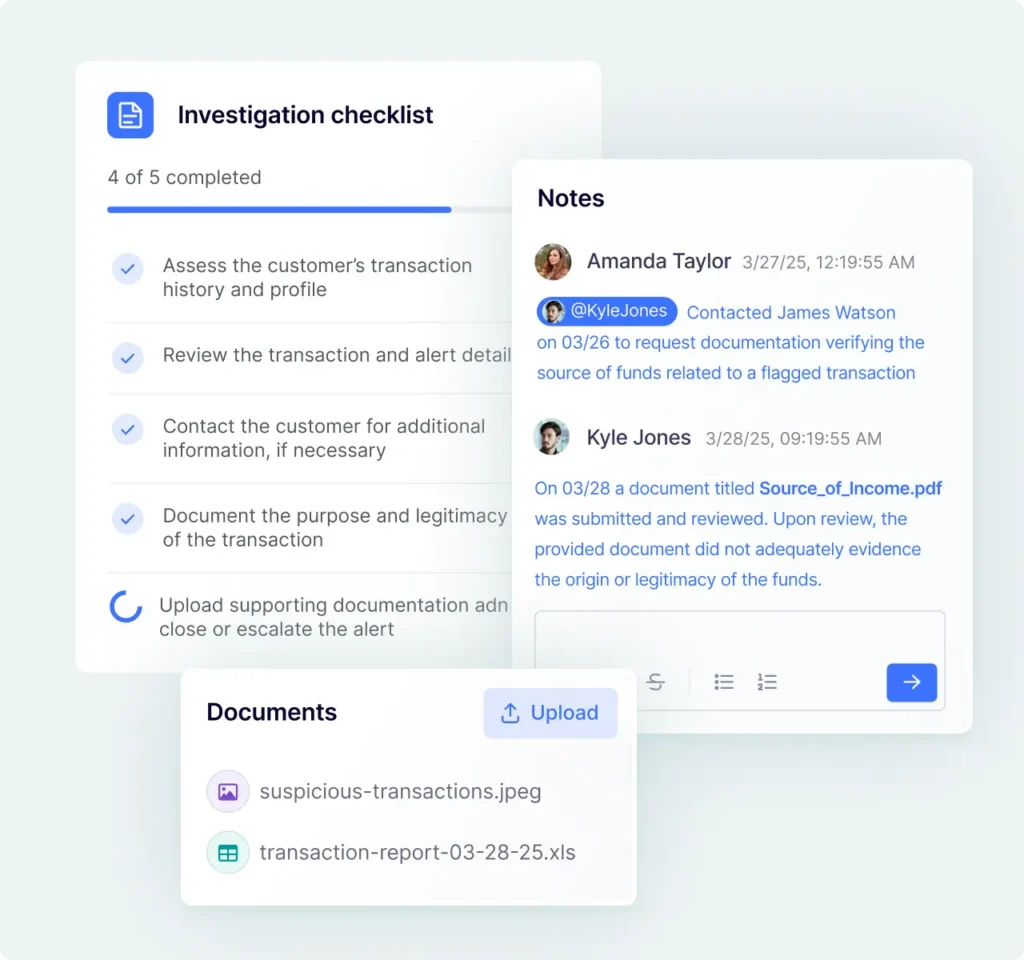

Investigate Cases Faster With Complete Customer Context

Unified Compliance and Fraud Prevention Solution

Fighting Fraud Across Different Risk Scenarios

Bonus Abuse

Real-time screening detects repeated or coordinated bonus misuse to protect revenue.

Fake & Synthetic IDs

Digital footprint analysis uncovers fake or synthetic identities before registration.

Account Takeover

Device and behavioral monitoring highlights unusual logins to block unauthorized access.

Payment Fraud

Adaptive scoring detects high-risk payments without blocking genuine users.

Registration & Onboarding

Data-driven checks identify fake users early, protecting growth and customer experience.

Login & Activity Monitoring

Social engineering attacks happen, but you can keep customer accounts safe.

Transaction Monitoring

AI-driven analysis detects fraud and risk in real time across millions of transactions.

Chargeback Fraud

Automated workflows manage chargebacks efficiently, reducing effort and recovering more revenue.

What Fraud Prevention Teams Are Saying

02/28/2024

“I believe, the best thing about Seon is it’s user-friendly interface. You always have all the information gathered and efficiently operated in one place, and compared to my previous experiences…”

Ilya G.

Anti-Fraud Specialist

03/05/2024

“For me the most useful tool is the manual email check function where you can validate the account which was used to make a particular transaction. The system gives a score for the email…”

Peter K.

Fraud Analyst

05/10/25

“SEON is an excellent fraud prevention tool — easy to integrate, fast, and reliable. It helps us detect suspicious activity in real time and has significantly reduced chargebacks.”

Verified User in Gambling & Casinos

Mid-Market Company

05/06/2025

“Customer-friendly and customizable UI, ensuring a seamless user experience tailored to our needs. With comprehensive customer support, SEON’s team is ready to assist you with everything.”

Verified User in Banking

Enterprise Company

05/06/2025

“SEON provides real-time fraud detection and rich data enrichment without requiring heavy manual setup. The scoring engine is flexible, and the rules-based logic allows us to adapt quickly.”

Verified User in Banking

Mid-Market Company

Deploy in Days, Not Months

Middleware orchestration tools take months to onboard. On average, teams go live with SEON in around 14 days. Go live quickly with a single API, ready-to-use rules and hands-on support.

in-house fraud prevention expertise

How Leading Teams Prevent Fraud at Scale

Learn More About Fraud Prevention

-

Get our free guide to reduce chargebacks, prevent fraud, and protect your revenue.

-

Explore AI-driven fraud detection, key fraud types, and strategies to choose the right system for real-time protection.

-

Learn how payment gateway fraud works and compare detection tools to stop BIN attacks, fake transactions, and account takeovers.

-

Discover tools to detect and prevent payment fraud. Protect your business and secure transactions effectively.

-

APP fraud is rising, driven by real-time payments. Businesses must use AI, ML, and digital intelligence to prevent scams.

-

Download our iGaming fraud guide to stop threats early, stay compliant, and protect revenue.

Fraud Prevention FAQs

What is a fraud prevention solution?

A fraud prevention solution is a unified technology solution that detects, prevents, and manages fraudulent activity across digital channels. It combines data from multiple sources, including device intelligence, digital footprint analysis, and behavioral signals, to identify suspicious activity in real time and enable businesses to block fraud before it causes financial loss and downstream operational costs.

What types of fraud does SEON’s fraud prevention solution detect?

SEON detects fraud across the customer journey including synthetic identity fraud, bot attacks, promo and bonus abuse, multi-accounting, account takeover, payment fraud and chargebacks. The platform adapts to new patterns through configurable rules and AI models.

How fast does the fraud prevention solution return risk decisions?

SEON’s API responses return in milliseconds, enabling real-time decisioning at registration, login, event and transaction monitoring without impacting user experience. High-volume environments can process thousands of transactions per second.

How does a fraud prevention solution support compliance requirements?

The solution also offers AML screening, payment screening, transaction monitoring and case management alongside fraud prevention, bring a wealth of unique signals together in one system to support coordinated fraud and compliance workflows.

Protect Every Interaction With a Unified Fraud Prevention Solution

Book time with fraud specialists who understand your industry and map your clear path forward.

Trusted by 5,000+ global organizations:

Speak With a Risk Expert

This form may not be visible due to adblockers, or JavaScript not being enabled.