Transaction monitoring is a key part of any anti-money laundering (AML) program. It helps financial institutions review transactions in real time and after the fact to spot suspicious activity such as money laundering, terrorist financing or other financial crime.

In this guide, we explain what AML transaction monitoring is, how it works and why it’s essential for compliance and risk management.

What Is Transaction Monitoring in AML?

AML transaction monitoring is the ongoing process of reviewing customer transactions to detect suspicious or high-risk activity. It plays a central role in anti-money laundering programs by helping institutions identify potential money laundering, terrorist financing or fraud.

Analysts use transaction monitoring rules to decide when a transaction looks suspicious. These may involve:

- Unusually large or frequent transfers

- Deposits into personal or non-personal accounts

- Withdrawals or payments inconsistent with customer history

Modern systems have made this process faster and more accurate. Automation and machine learning help identify suspicious behavior in real time, reducing false positives and supporting compliance across all transaction types.

How Does the AML Transaction Monitoring Process Work?

The AML transaction monitoring process works by continuously reviewing customer transactions to spot activity that falls outside expected behavior. Instead of relying on one-off checks, institutions use ongoing monitoring to catch potential money laundering or financial crime as it happens.

It does this by collecting transaction data, comparing it with each customer’s risk profile and flagging unusual patterns for further review or investigation.

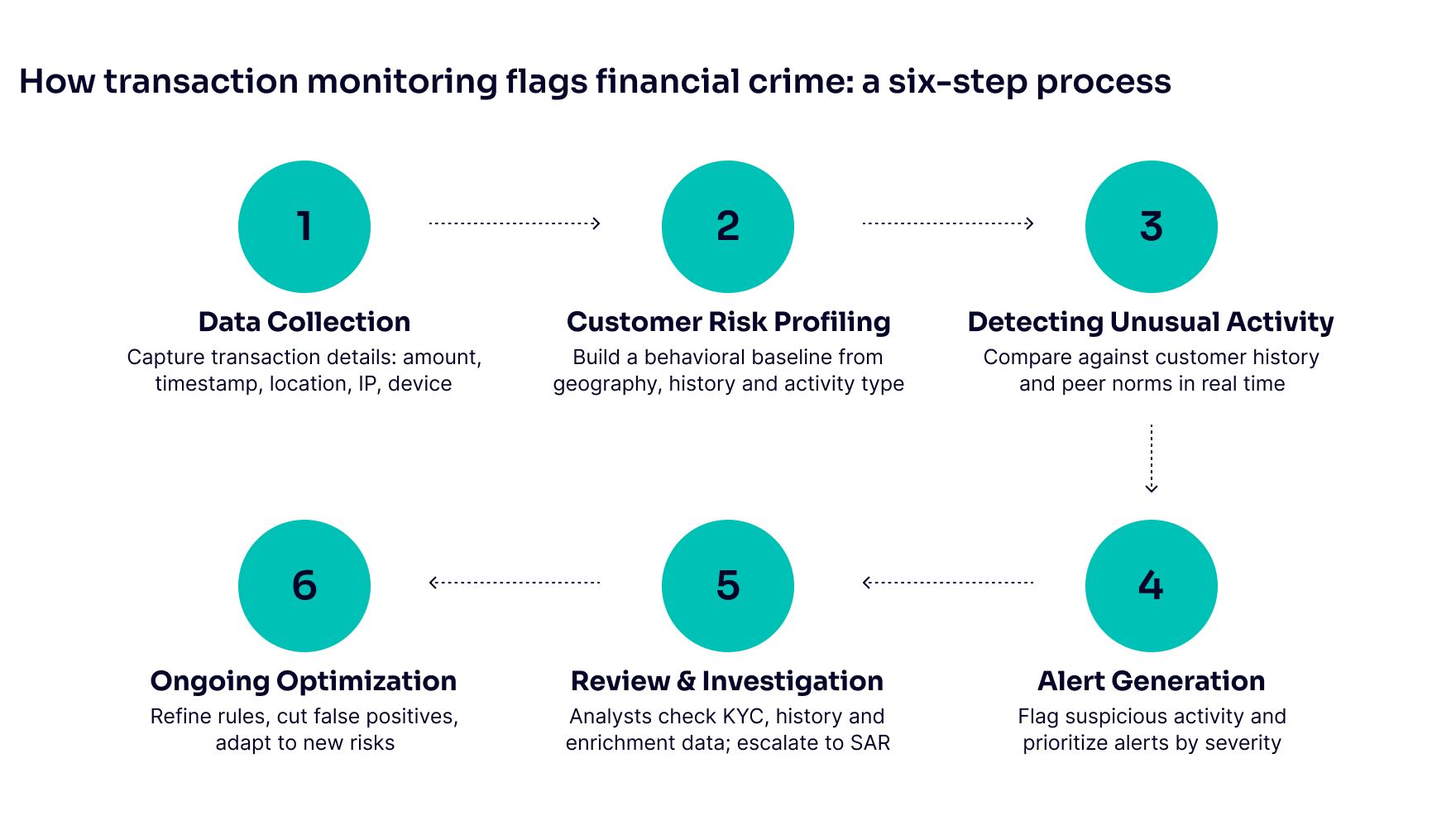

1. Data collection

The process starts with gathering detailed information about each transaction, including amounts, timestamps, locations, IP addresses, and device types. This comprehensive data forms the foundation for spotting unusual patterns and training monitoring systems to detect suspicious activity more effectively.

2. Customer risk profiling

Next, institutions build risk profiles for each customer by looking at multiple factors, such as:

- Geography: where the customer lives or transacts from

- Transaction history: typical amounts, frequency, and patterns

- Type of activity: the nature of payments, transfers, or services used

Establishing this behavioral baseline makes it easier to spot unusual activity later, for example, a sudden spike in transfers abroad or a shift to high-risk payment methods.

Customer segmentation is critical here. A transaction that looks normal for a corporate treasury account may be highly anomalous for a retail savings customer.

3. Detecting unusual activity

Transactions are then analyzed in real time and compared against both the customer’s past behavior and peer group norms. Monitoring systems flag red flags like sudden spikes in volume, frequent transfers to high-risk jurisdictions, or attempts to stay just below reporting thresholds.

“Suspicious activity isn’t always easy to spot as it’s frequently embedded in patterns that appear mundane on the surface. However, when seen through the right lens, these signals become clear indicators of deeper risks.”

Nauman Abuzar, VP of AML Compliance and Risk

4. Alert generation

The system generates alerts whenever it detects unusual activity. Alerts are then prioritized by severity so compliance teams can focus on higher-risk cases without being overwhelmed by low-priority reviews.

Effective alert triage separates genuine suspicious activity from false positives. Many legacy systems struggle here because overly broad rules generate large volumes of low-quality alerts.

5. Review and investigation

Analysts review flagged transactions by examining customer KYC details, historical activity patterns and enrichment data such as device intelligence or digital footprint signals. This helps determine whether the activity fits the customer’s typical behavior.

If the activity appears suspicious, the case is escalated and may lead to a Suspicious Activity Report (SAR) being filed with regulators. Investigation steps are documented in a case management system to maintain the required audit trail.

6. Ongoing optimization

Effective AML transaction monitoring must evolve alongside new risks. Institutions regularly refine detection rules, adjust monitoring strategies and reduce false positives to keep systems accurate and efficient over time.

Modern platforms can also accelerate regulatory reporting by assisting with SAR narrative generation and automating parts of the reporting workflow.

Why Is Transaction Monitoring Important?

Transaction monitoring is essential because it ensures regulatory compliance, enables proactive risk detection and strengthens customer due diligence. Effective monitoring helps institutions uncover financial crime red flags early, protect customers and maintain trust by continuously assessing behavior and updating risk profiles in real time.

Why Is It Essential for Regulatory Compliance?

Global frameworks such as FATF, the EU’s 6AMLD and U.S. FinCEN guidelines require institutions to detect and report suspicious activity tied to money laundering and terrorist financing. Failure to meet these obligations can result in heavy fines, remediation orders, license loss and significant reputational damage, as seen in major enforcement cases like Westpac’s AUD 1.3 billion penalty for inadequate monitoring.

Core Capabilities of a Modern AML Transaction Monitoring System

Modern AML transaction monitoring requires more than static rulebooks. An effective system must adapt quickly to evolving risks, support regulatory expectations and give investigators clear visibility into suspicious behavior. The capabilities below define a scalable, compliant approach.

- Real-time detection: Screening transactions as they occur helps institutions identify unusual patterns immediately, reducing exposure to potential laundering and enabling faster escalation when needed.

- Contextual behavioral analysis: Strong systems look beyond transaction amounts by incorporating behavioral, device and geolocation signals. This added context helps distinguish genuine customer activity from hidden typologies.

- Flexible, configurable rules: Compliance requirements change frequently. No-code or easily adjustable rule builders allow teams to update thresholds and logic without engineering delays, ensuring monitoring stays aligned with policy and risk appetite.

- Prioritized, high-quality alerts: With rising volumes, systems must sort alerts by severity, customer risk and typology relevance. This reduces noise and directs investigators toward the most critical cases.

- Integrated sanctions and watchlist screening: Effective solutions screen customers and transactions against up-to-date sanctions lists, PEP data and adverse media, strengthening regulatory coverage and audit defensibility.

- Full investigation tools: A complete system supports the entire process — from alert to SAR filing — with case management, audit trails and collaboration tools that help teams document findings and meet reporting obligations.

Compare leading transaction monitoring software to see how each helps detect suspicious activity and maintain compliance.

Read more

Batch vs Real-Time Transaction Monitoring

Batch monitoring and real-time monitoring represent two different approaches to reviewing transactions for suspicious activity.

Batch monitoring reviews transactions after processing, typically at the end of the day or during scheduled intervals. Although this method meets basic compliance requirements, it delays the identification of potentially illicit behavior. By contrast, real-time transaction monitoring screens transactions as they happen, enabling institutions to respond instantly before further damage occurs.

Although real-time AML monitoring isn’t mandated by regulators, it is widely regarded as best practice, helping reduce risk, accelerate investigations, and ensure timely Suspicious Activity Report (SAR) filings. Modern AML tools achieve this by combining behavioral data, transaction velocity, and custom rules to detect threats faster and minimize false positives compared to batch screening.

To explore more about how this approach compares with batch screening, see our deep dive on real-time vs batch monitoring.

Common Challenges in Transaction Monitoring

Many compliance teams struggle to balance speed, accuracy, and regulatory demands. Legacy systems often generate too many alerts for legitimate activity, causing alert fatigue and slowing investigations. At the same time, siloed data and rigid rule engines make it harder to connect behavioral, transactional, and device signals, reducing visibility into real risk. When rules can’t adapt quickly enough to new typologies like structuring or rapid fund movements, real threats can slip through while resources are wasted on false positives.

The other challenge is scalability. High transaction volumes, changing regulations, and separate fraud and AML tools often result in duplicated work, delayed filings, and inconsistent audit trails. Without real-time monitoring and unified workflows, teams spend more time managing alerts than mitigating risk. The solution lies in modern, configurable systems that combine behavioral analytics, machine learning, and risk-based prioritization to cut through the noise, helping institutions detect true suspicious activity faster and stay fully compliant.

Why Effective AML Transaction Monitoring Matters

Modern AML transaction monitoring systems rely on real-time detection to spot suspicious activity the moment it occurs. By combining behavioral, transactional, device and IP data with AML alerts, institutions gain clearer visibility into risk and can more accurately distinguish genuine behavior from potential money laundering patterns.

Configurable rules and automation help reduce false positives and surface higher-quality alerts, while case routing ensures analysts focus on the most critical investigations. Direct integration with sanctions lists, crime databases and PEP registries supports accurate, defensible decisions. Meanwhile, built-in case management, audit trails and AI-assisted SAR filing streamline investigations and maintain end-to-end compliance coverage.

How SEON Strengthens AML Transaction Monitoring

In AML, transaction monitoring safeguards financial institutions from exploitation, ensures compliance with regulations, and maintains overall integrity. As a result, proactive oversight has become essential, especially as fraudsters leverage advanced technologies and real-time digital payments.

SEON’s AML transaction monitoring solution empower your anti-fraud and money laundering prevention strategy by providing access to hundreds of user identity and transaction data points. These insights enable the creation of customized, flexible, and powerful rules to mitigate AML risks while also protecting against other types of fraud.

Frequently Asked Questions

What AML typologies can be detected through transaction monitoring?

Transaction monitoring helps identify key AML typologies such as structuring, layering, mule activity, high-risk jurisdiction transfers and sudden account behavior changes. By analyzing transaction patterns, customer history and contextual data, institutions can detect abnormal movements that may indicate money laundering or other financial crimes.

What global regulations govern AML transaction monitoring, and what are the penalties for non-compliance?

Global AML regulations, such as the FATF Recommendations, the EU AML Directives, and the U.S. Bank Secrecy Act, require financial institutions to monitor transactions for suspicious activity. Failure to implement effective monitoring can result in significant penalties, including multimillion-dollar fines, regulatory sanctions and even criminal liability for compliance failures. Regulators like FinCEN, the European Banking Authority and the UK’s FCA actively enforce these obligations worldwide.

What are examples of suspicious activity detected by AML transaction monitoring?

AML transaction monitoring detects financial behaviors that may indicate money laundering, fraud, or terrorist financing — such as large or frequent cash deposits, transfers just below reporting thresholds, or movements involving high-risk jurisdictions. Automated transaction monitoring tools help uncover these patterns efficiently across large transaction volumes.

What role does transaction monitoring play in AML compliance?

Transaction monitoring is the primary mechanism for detecting suspicious activity on an ongoing basis. It connects the initial risk assessment performed during customer onboarding with continuous oversight throughout the customer relationship, supporting the identification and reporting of potential financial crime.

How does transaction monitoring work in banks?

Banks apply transaction monitoring across high volumes of retail and corporate activity. Retail accounts are typically monitored for structuring and unusual cash patterns, while corporate accounts are screened for anomalous cross-border transfers and trade finance flows. Banks are subject to direct regulatory examination of their monitoring programs, making consistent alert handling and documented audit trails especially important.

Sources

- UNODC: Money Laundering portal

- United Nations: Money Laundering

- Trading Economics: World Full Year GDP Growth

- Financial Action Task Force (FATF): Risk-Based Approach Guidance

- MarketsandMarkets: Transaction Monitoring Market Forecast