Payment card fraud costs merchants hit $33.41 billion in 2024, according to the Nilson Report, yet one of the most reliable early signals is in plain sight: the first digits of the card number. A Bank Identification Number (BIN) lookup is the fastest way to automatically retrieve that data, giving fraud teams instant context about a card before a transaction is approved.

This guide covers what a BIN lookup returns, how it detects fraud and what it cannot do on its own.

Key Takeaways

- Automated BIN lookups via API are faster and more consistent than manual searches on free third-party sites, which often use outdated data.

- The first 6 to 8 digits of any payment card identify the issuing bank, card type and country of origin.

- Real-time BIN lookups return card brand, level, type and issuing bank instantly, giving fraud teams the context needed to act.

- When the BIN’s issuing country does not match the customer’s location or shipping address, that mismatch is a reliable fraud signal.

What Is BIN Lookup?

A BIN lookup is the process of querying a database using the first 6 to 8 digits of a payment card to identify the issuing bank, card type, card level and country of origin, giving fraud teams instant context to flag suspicious transactions.

Those digits are known as the Bank Identification Number (BIN) and are sometimes called the Issuer Identification Number (IIN) because they identify which financial institution issued the card. Every credit card, debit card, prepaid card, gift card and charge card carries one, which means the lookup works across card types, not just credit.

What Data Does a BIN Lookup Return?

The data returned by a BIN lookup goes beyond simply identifying the card issuer. Each field serves a specific purpose in fraud scoring, which is why the lookup is most useful when the results feed directly into a risk rules engine rather than being reviewed manually.

A standard BIN lookup returns:

- Card brand: Visa, Mastercard, American Express, Discover and others

- Card type: credit, debit or prepaid

- Card level: classic, gold, platinum, corporate or business

- Issuing bank name: the name of the financial institution that issued the card

- Issuing bank country: the country where the card was issued

- Bank contact details: phone number and website for the issuing institution

The card type and level fields are particularly useful for compliance use cases. A corporate card flagged on a gambling platform, for example, can trigger an automatic review before the transaction completes.

For anyone transacting with customers online, card fraud can be a huge pain point. Find a better way to address it here.

How to detect card fraud

How to Perform a BIN Lookup

You can run a BIN lookup through a standalone third-party website, or integrate it directly into your existing anti-fraud tools. The manual route is straightforward: enter the card details into an online checker and read the results. Automated lookups run through API calls instead, returning the same data in milliseconds without an analyst lifting a finger.

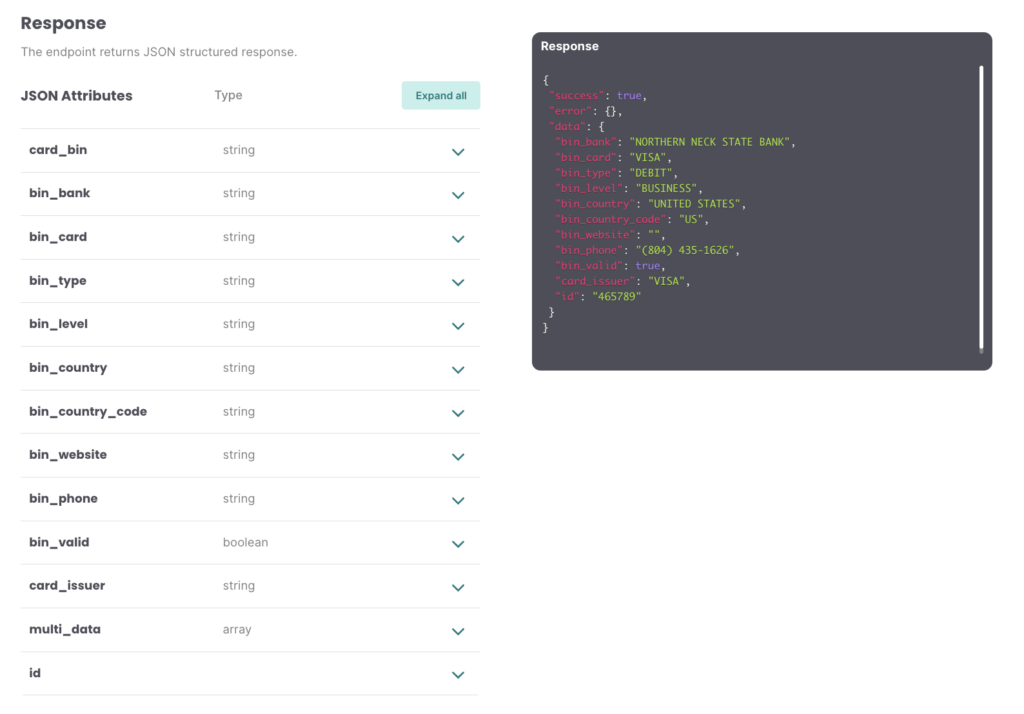

Here is an example of the kind of data you will get back when you call SEON’s Fraud API with a BIN query.

Manual Versus Automated BIN Lookups

Not all BIN lookup methods return the same results, and that inconsistency is the core problem with manual searches. Free online tools pull from different databases, some of which are months or years out of date, so the same BIN can return conflicting information depending on which site you use.

“We now have a constant source of truth for card BINs. If you go and type a card BIN on the internet you’ll get 50 different results because the lists are all over the place. But now with SEON we can be consistent when linking cards across the team.”

Rick Hiltbrunner SENIOR MANAGER OF FRAUD OPERATIONS at Patreon.

Automated BIN lookups via API solve both problems. Because the call happens within your existing fraud workflow, the data is consistent, the response is near-instant and there is no risk of accidentally sharing card details with an unvetted third-party site.

The advantage goes beyond consistency, though. When you feed BIN data straight into a scoring engine, the engine weighs it against every other signal automatically. A BIN country that matches the shipping address and IP location pulls the risk score down; a mismatch pushes it up, with any manual checks.

How Does BIN Lookup Help With Fraud Prevention?

BIN data earns its place because fraudsters cannot easily fake it. They can lie about a shipping address or mask their IP behind a VPN, but the BIN on a stolen card always points back to the real issuing bank and country. That gap between what a fraudster claims and what the card data reveals is exactly what a fraud team can act on.

Country mismatch

The most common fraud signal is a mismatch between the card’s issuing country and the customer’s stated location or shipping address. A card issued by a US bank being used to ship goods to a different region, combined with an IP address that does not match either location, is a strong signal worth reviewing.

Prepaid card flags

Prepaid cards are a preferred tool for fraudsters because they can be loaded with stolen funds and discarded after use. Identifying a prepaid card via a BIN check does not confirm fraud on its own, but it raises the risk score enough to warrant additional verification before approving the transaction.

Corporate card misuse

Certain regulations prohibit corporate cards from being used in specific contexts, gambling platforms being the clearest example. A BIN lookup that returns a corporate or business card level in a regulated environment can trigger an automatic block, reducing exposure to regulatory fines before any manual review takes place.

BIN attacks

A BIN attack is a method where fraudsters generate card numbers using a known BIN, running thousands of small test transactions to identify valid combinations. BIN lookup alone does not stop an attack, but it feeds the velocity rules that do, flagging when multiple transactions share the same BIN within a short time window.

Other Useful Data Enrichment Tools to Consider

A BIN Lookup is a great additional help to reduce fraud, but it’s only good in combination with other tools.

For instance, you’ll need to learn as much information about the user based on:

- The IP address: is the user truly where their IP says they are? Are they using a VPN, proxy, or TOR browser?

- The email address: does it point to a free or low-friction domain for creating email addresses? Has it appeared on spam blacklists in the past?

- The phone number: is it legitimate or from a virtual SIM card? Is it pointing to the same country as the BIN card suggests?

You can learn more about data enrichment and how it can help reduce fraud rates.

Use Cases Where a BIN Lookup Can Reduce Fraud

Ecommerce and card-not-present fraud

Card-not-present (CNP) transactions are the highest-risk environment for payment fraud because there is no physical card to inspect. A BIN lookup is one of the fastest ways to cross-reference card data against transaction context, flagging mismatches in country, card type or card level before the payment is authorised.

iGaming and bonus abuse

Online gambling platforms face a specific challenge: fraudsters need unique payment details for each fake account they create. Prepaid cards are a common solution on their end, which is why a BIN check that identifies a prepaid card at registration, especially from a mismatched country, is a reliable early signal of multi-accounting or bonus abuse.

Fintech, BNPL and balance transfers

For fintech platforms and buy-now-pay-later providers, BIN data adds a useful verification layer at the point of a balance transfer or payment setup. Checking whether a card being linked to an account originates from the same country as the registered user is a low-friction step that catches a meaningful share of account takeover attempts.

Identity fraud and onboarding

When card payment is part of the onboarding or identity verification flow, a BIN lookup helps complete the user profile. A prepaid card from a country that does not match the user’s stated address of residence is a red flag worth escalating, particularly when combined with other weak identity signals.

Compliance

Regulatory requirements create hard rules around card types in certain industries. Corporate cards cannot be used for gambling; some prepaid cards cannot be used for regulated financial products. BIN checks make it possible to enforce these restrictions automatically at the transaction layer, rather than relying on manual review after the fact.

BIN Sponsorships and Digital Banks

A growing challenge with BIN Lookups are posed by digital banks and fintechs who issue their own cards (such as Monzo or Revolut). While they are very popular with consumers, these companies typically use something called a BIN Sponsorship to issue these cards, and the BIN ranges will constantly change. A BIN Lookup then might return the sponsorship partner bank, rather than the actual fintech who issued the card.

How SEON Does BIN Lookups

SEON integrates BIN lookup directly within the Fraud API, so the data is returned alongside email, IP, phone and device signals in a single call. There is no separate tool to query and no risk of exposing card details to a third-party site.

The BIN data SEON uses is selected for 99% accuracy, monthly refresh on a database of over 50 million results, and sub-second API response times. When a BIN country mismatch or prepaid card flag is returned, it feeds automatically into the risk score and can be weighted up or down depending on the specific context of your business.

For fraud teams that want to act on the signal without building custom rules from scratch, SEON’s default rule set applies BIN data out of the box from day one.

Improve your risk management with SEON’s real time data enrichment tools

Ask an Expert

Frequently Asked Questions About BIN Lookups

What is a BIN lookup?

A BIN lookup is the process of querying a card database using the first 6 to 8 digits of a payment card number to return information about the issuing bank, card type, card level and country of origin. It gives fraud teams instant context about a card before a transaction is approved.

Is BIN lookup the same as device fingerprinting?

No, they are complementary signals that operate at different layers. A BIN lookup tells you about the card being used; device fingerprinting tells you about the device making the transaction. Both feed into a fraud score, but neither replaces the other. Conflating the two is a common misconception among teams evaluating fraud tools for the first time.

What is a BIN attack and how does BIN lookup help?

A BIN attack is when fraudsters generate card numbers from a known BIN and run small test transactions to find valid combinations. BIN lookup does not stop an attack directly, but it supplies the BIN-level data that powers the velocity rules which do, flagging when an unusual volume of transactions share the same issuing bank and range within a short time window.

How can BIN lookups reduce fraud rates?

The more you know about the card, the more you can cross-reference that information with the user data. Mismatched or suspicious data should raise red flags and trigger manual reviews.

Learn more about:

Browser Fingerprinting | Device Fingerprinting | Fraud Detection API

Sources used for this article:

- binlist.net: Free Bin Checker Tool

- freebinchecker.com: Free Bin Checker Tool