Fintech Fraud Prevention

Don’t Let Fraud Hold Your Business Back

SEON helps fintechs, digital bank and crypto platforms stop fraud at onboarding, login and transaction while scaling into new markets and streamlining AML compliance.

Trusted by the World’s Most Ambitious Companies

Fintechs Using SEON See Results

90%

cut in fraudulent registrations

93%

decrease in manual review time

99%

reduction in multi-accounting attempts

PROTECT GENUINE CUSTOMERS

Block Suspicious Users Instantly

SCALE YOUR GROWTH

Defend Your Presence in Emerging Markets

IMPROVE EFFICIENCY

Proactively Prevent Fraud with AI

Go live in 14 days or less

Choose how you integrate directly with SEON’s APIs or through the AWS Marketplace.

Discover How Companies Win

“We chose SEON because it offers risk score transparency, which other platforms don’t offer, and because of the custom rules. Granular control is important because we can tailor our risk strategy down to the level of the region or city where our customers sign up from. Implementing SEON has enabled us to achieve a 90.6% auto-approval rate for genuine customers.”

Martina Virgilio

Anti-Financial Crime Manager

“We now see close to zero successful identity fraud cases. And as a BNPL company, this has a direct impact on other metrics, such as a 90% drop in fraudulent registrations and a 50% drop in chargebacks.”

Claus Linde

Chief Product Officer, Viabill

Learn More About Fintech Fraud

-

AFASA is reshaping fraud compliance in the Philippines. Learn how fintechs can use real-time monitoring and mule detection to drive…

-

Download our free guide to secure efficient digital bank onboarding and tackle evolving fraud risks.

-

Fraudsters target digital banks with ATOs, phishing, and synthetic identities. Learn how AI, ML, and compliance enhance security.

-

How crypto transaction monitoring works, which regulations apply, how it differs from traditional AML – all in one guide

-

Alternative credit scoring uses digital footprints and non-traditional data to improve credit access and risk assessment.

FAQ

What is fintech fraud prevention?

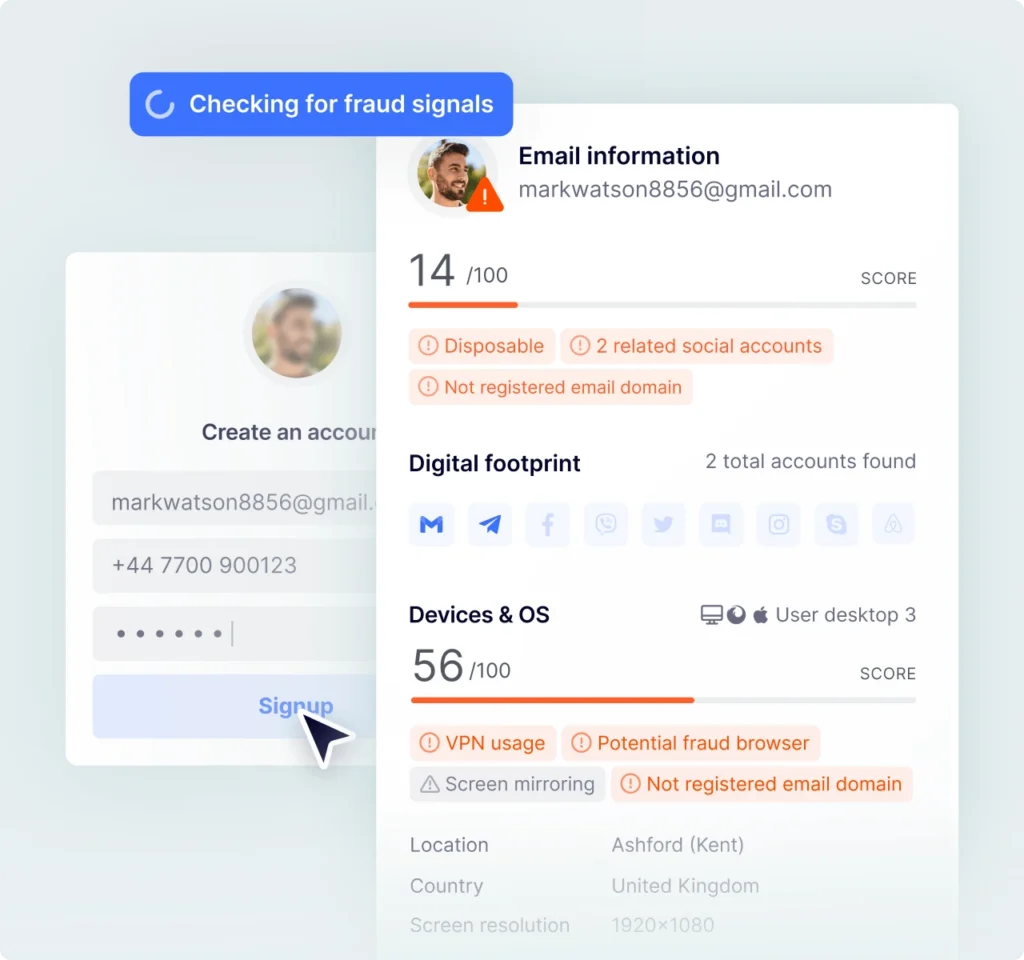

Fraud in financial services doesn’t just cause direct losses, it erodes customer trust and slows growth in markets where onboarding speed is a competitive advantage. Fintech fraud prevention is the use of technology to detect and block fraudulent activity across digital financial services, covering onboarding, login and transactions. It combines device intelligence, digital footprint analysis and AI-powered rules to identify suspicious users before they cause financial or reputational damage.

What is synthetic identity fraud in fintech?

Unlike stolen identity fraud, synthetic identity fraud is difficult to detect because the identity partially exists in real data systems. It occurs when fraudsters combine real and fabricated personal information to create a fictitious identity, which is then used to open accounts, access credit or exploit onboarding processes. Because no single real person is immediately harmed, it often goes undetected longer than other fraud types.

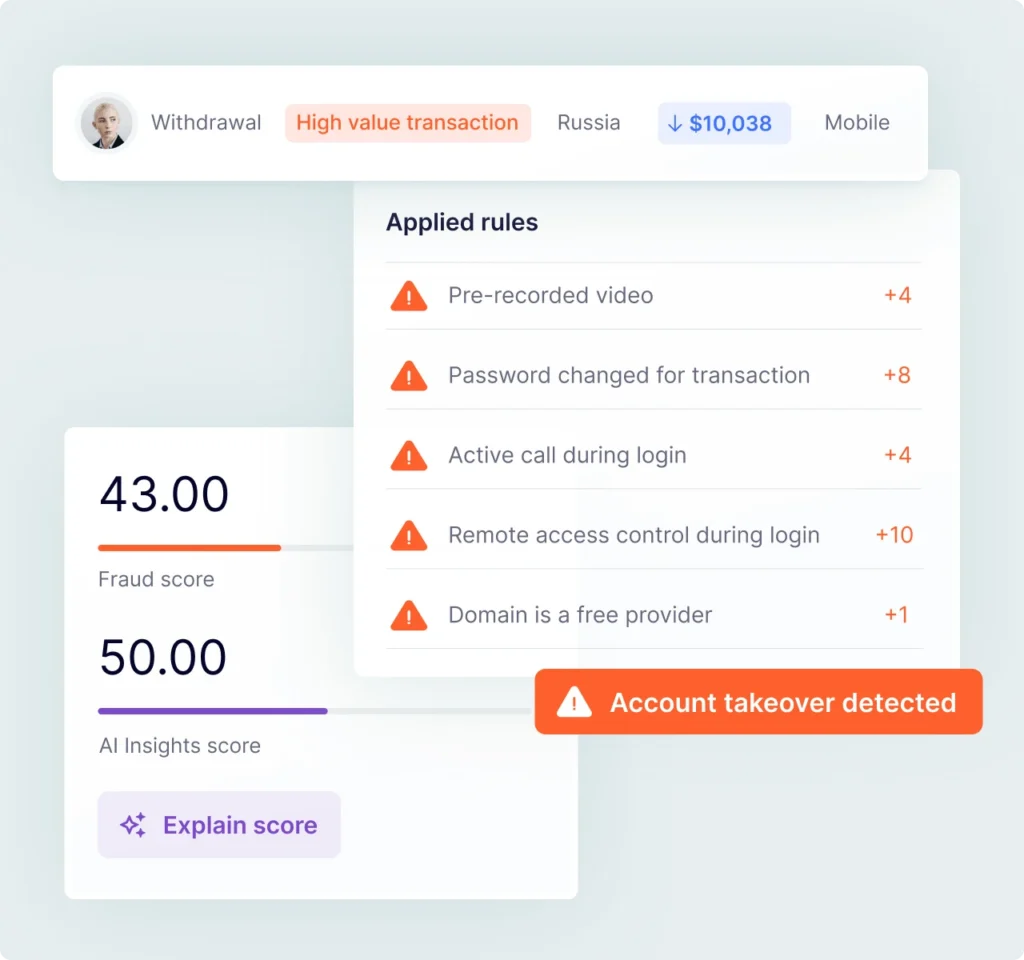

What makes account takeover fraud hard to detect in fintech?

The difficulty is that account takeovers happen through legitimate entry points. A fraudster using stolen credentials looks identical to a returning customer at the login stage, which means detection has to rely on behavioural and device signals rather than identity checks alone. Velocity patterns, device fingerprinting and IP reputation data are what separate a genuine login from a takeover attempt.

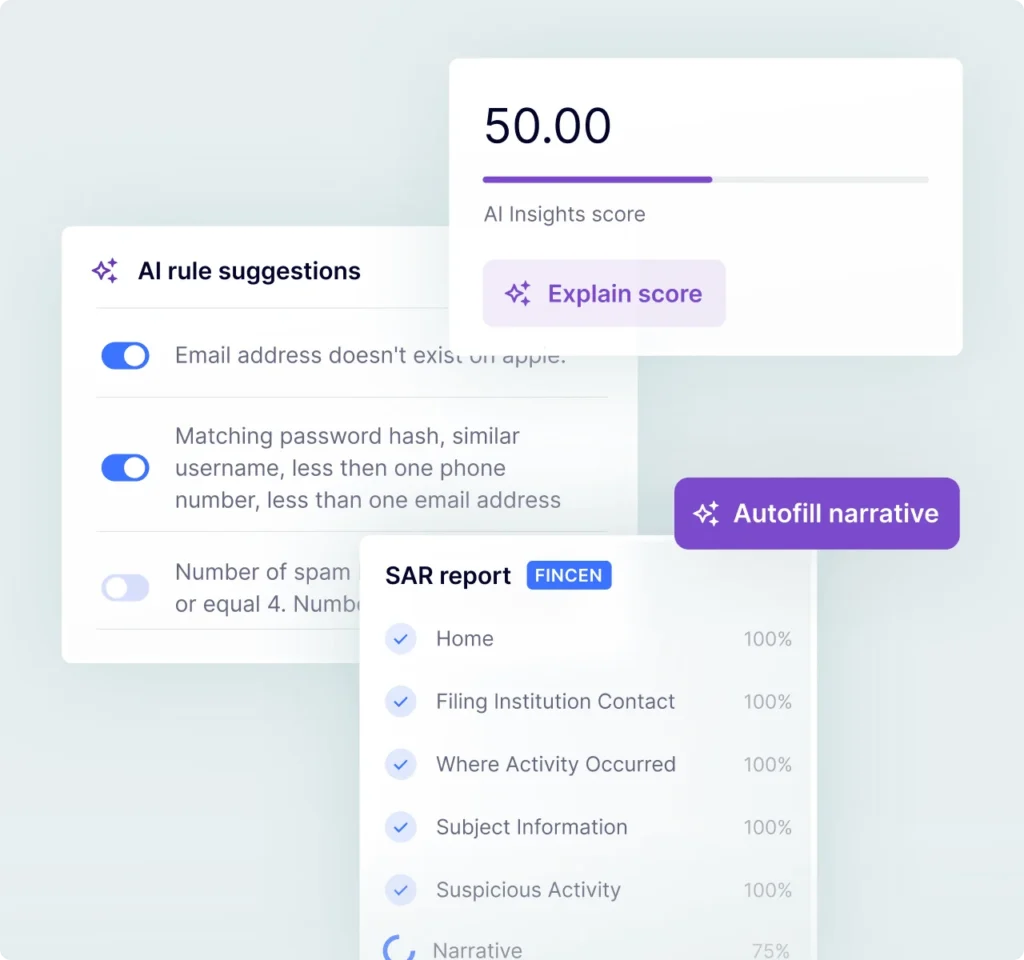

How do fintechs meet AML compliance requirements?

Regulators require fintechs to screen customers, monitor transactions for suspicious patterns and file Suspicious Activity Reports when illicit behaviour is identified. Meeting those requirements operationally means having continuous monitoring in place, not just point-in-time checks at onboarding. Fintechs that consolidate fraud prevention and AML into a single platform reduce the overhead of managing them as separate workflows while maintaining a complete audit trail.

How does SEON detect fraud at onboarding without adding friction?

Most fraud prevention checks happen after a user has already entered the funnel, which creates friction for genuine customers and delays detection of bad actors. SEON analyses email, phone and IP data at the point of onboarding to build a digital footprint of each user before KYC begins. Risk thresholds determine whether a user is approved automatically or flagged for step-up authentication, keeping the journey smooth for the majority while catching suspicious identities early.

Take the First Step Toward Transformative Fraud Prevention

“By leveraging the power of advanced analytics and data-driven insights, we were able to achieve our goals of expanding our customer base while effectively managing credit risk.”

Costin Mincovici, Chief Credit Officer, tbi Bank

Book Time With Our Experts

This form may not be visible due to adblockers, or JavaScript not being enabled.