In Europe, APP fraud losses are estimated to reach €2.4 billion, with an annual growth rate of 20-25 percent. Likewise, the United States is poised to witness authorized push payment (APP) fraud losses soar to $3 billion by 2027, up from $1.94 billion in 2022.

APP fraud, a form of social engineering that deceives victims into voluntarily transferring money to fraudsters, represents a growing challenge for the financial sector. With the integration of cutting-edge technologies like artificial intelligence (AI) and machine learning (ML), fraudsters are scaling their operations to unprecedented levels, as these technologies make it easier for less sophisticated actors to execute significant scams on a broad scale.

Facing this growing threat, the financial sector, consumers and businesses must adapt their defenses to combat the increasing volume and velocity of APP fraud. As these scams are expected to double by 2026 – companies need to adopt agile, scalable solutions that can keep pace with fraudsters. AI, ML and other technologies like device intelligence, digital footprint analysis and transaction monitoring offer a proactive approach, enhancing automation, improving decision-making accuracy and turning the tide against APP fraud.

Reduce APP fraud risks with clear communication, robust safeguards, and proactive education for businesses and financial institutions.

Read more

Adding Fuel to the Fire: Real-Time Payments

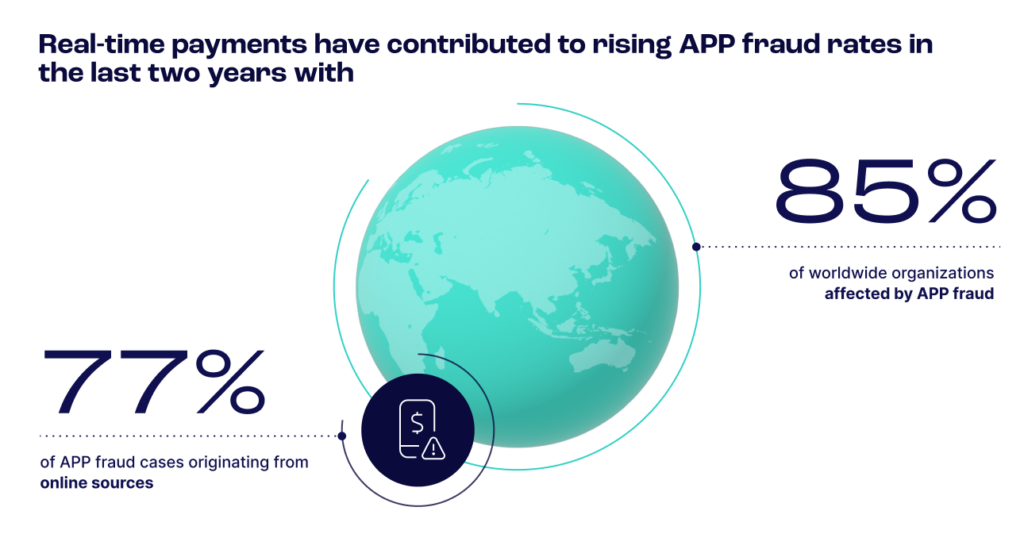

In the last two years, 77% of APP fraud cases originated online, impacting roughly 85% of global organizations. Spanning a variety of duplicitous practices that rely on tactics that manipulate trust and authority, APP fraud’s end goal is to prompt victims into transferring money to fraudster-controlled accounts. Whether through impersonation, romance scams or other social engineering techniques, the result is the same: victims willingly transfer money for goods or services that don’t exist.

Because APP fraud relies on victim-authorized payments, traditional fraud prevention methods often fail to intercept these transactions. The widespread adoption of real-time payments, driven by initiatives like FedNow in the US and the European Union’s revised Payment Services Regulation (PSR), exacerbates the problem. Fraudsters exploit these payments’ speed and irrevocability, making it easier to launder money and evade detection.

Earlier Fraud Intervention

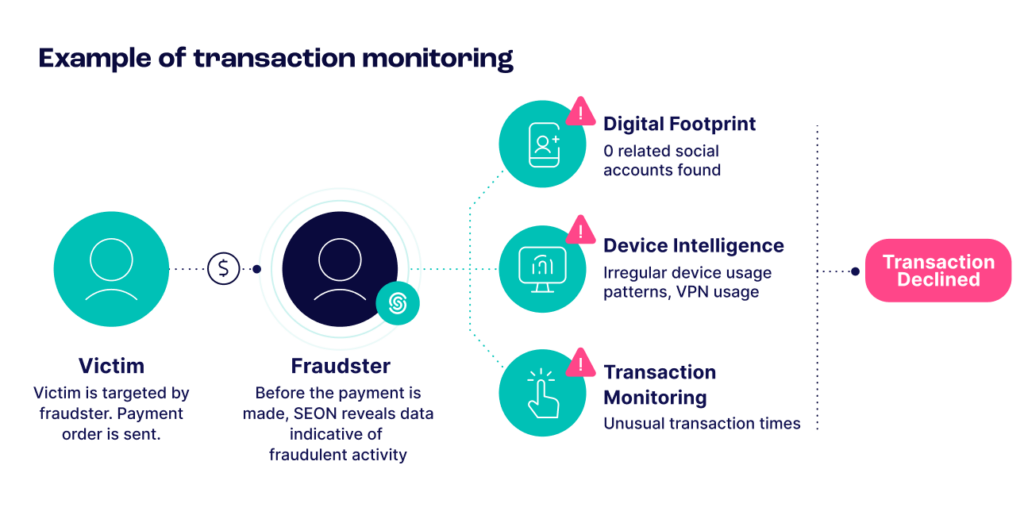

To counter APP fraud, companies must be able to identify bad actors and stop fraud earlier in the customer journey. By examining patterns, behaviors and connections that cut across the digital landscape, companies can detect anomalies and red flags that suggest fraudulent intent before a transaction is even authorized – working to offset the speed of real-time payments.

- Flagging suspicious logins: By analyzing logins from unfamiliar devices, particularly from vulnerable age groups like those 60 and older, institutions can flag potential fraud early. Older adults are often targeted in scams, so detecting logins from such age demographics could be a valuable early warning system.

- Remote access detection: Identifying when a customer’s device is under remote control or accessed through screen sharing or mirroring can be a critical indicator of fraud. For example, if someone is logging in while sharing their screen with a third party, it could indicate coercion or manipulation. Device intelligence can further detect whether a customer is on a call during a login, providing more insight into potential threats.

- Device intelligence and behavioral signals: Analyzing factors like geolocation, typing speed, battery life and phone orientation enables institutions to detect anomalies indicative of phishing or fraud. For example, if a login occurs on a new device or during suspicious activities like screen mirroring, it may trigger an investigation before the fraud can proceed.

- Transaction monitoring: Institutions can better differentiate between legitimate and fraudulent activities by analyzing transactional behaviors, such as sudden large transfers to unfamiliar entities. Transaction monitoring provides a more holistic view, integrating behavioral data to assess risk comprehensively.

Meeting Scale with Scale

Since the problem of APP fraud isn’t one of complexity but one of scale, the same technologies fraudsters use to execute schemes must be harnessed to scale solutions for detection and prevention efforts. With the central challenge of APP fraud lying in the sheer volume of activities catalyzed by the proliferation of real-time payments, the integration of large language models (LLM), AI and ML into fraud prevention strategies is no longer a choice but a need.

AI Frees Valuable Time for High-Level Focus

Leveraging technology to automate processes and to surface patterns and anomalies such as unusual transaction volumes, geographic irregularities, inconsistent spending patterns and atypical access types at unprecedented speed with precision grants companies the power to prevent, detect and analyze for fraud while reducing manual workloads on risk and compliance teams.

Although manual intervention cannot be entirely eliminated – owing to the nuanced and sophisticated nature of certain fraud scenarios – the efficiency gains from automation allow human analysts to concentrate their expertise on more complex, high-risk cases. This strategic allocation of resources ensures that the fraud team is optimized, reducing bottlenecks caused by the overwhelming volume of cases and enabling more agile responses to APP threats.

Offering many benefits, advanced technologies like AI, ML, and other innovations allow for analyzing vast datasets at a velocity and quantity unattainable by human capacity alone. Blackbox machine learning is efficient in churning through data to provide rapid fraud detection scores but lacks transparency in its decision-making processes.

This obscurity can impede the ability to fine-tune or understand the basis of certain fraud alerts. But, when used in tandem with whitebox machine learning, an AI model that offers the transparent rationale behind AI decisioning, companies can refine choice-making based on customizable risk thresholds to fit their business needs at the scale required to thwart fraud today.

Safeguarding Trust and Financial Assets

Armed with a more nuanced understanding of behavior to inform transactional context and by harnessing the power of AI to meet the scale at which fraudsters are operating today, APP fraud is a combatable issue. By achieving the balance of providing customer convenience with security, the financial industry can address the problems posed by APP fraud in this era of emerging technologies.

Incorporating solutions that address scale, new regulatory frameworks and ongoing customer education initiatives can mitigate risks. The implementation of specific measures, such as the UK’s Confirmation of Payee (CoP) service, which cross-references bank details with the account holder’s name during online transactions, is an example of how regulatory bodies and industry oversight can press traditional banks and payment platforms to take more decisive actions against APP fraud.

Digital footprinting extends beyond the basic verification checks, like cross-referencing bank account details with account holder names; this type of confirmation isn’t enough. Financial institutions can leverage digital footprinting to scrutinize email or phone numbers associated with each transaction. Upon the initiation of a transfer, the system can analyze the digital footprint of the recipient, including their online behavior patterns, digital identity and historic transactional data to yield a risk score, providing an additional metric for assessing the transaction’s legitimacy.

Suppose the account is suddenly linked to a phone number or email associated with previous fraudulent activities or a dubious online presence. In that case, the system can trigger further investigation before proceeding with the transaction.

By aggregating and analyzing vast amounts of data to provide real-time insights into the risk associated with specific digital identities, insights can inform the transaction approval process, allowing financial institutions a more granular understanding of potential risks and enabling them to intercept fraudulent transactions proactively.

Unifying a Defense Against APP Fraud

Countering APP fraud requires a dynamic and holistic fraud prevention strategy in which advanced technologies like AI and ML afford the speed and scale needed to counteract the tactics of fraudsters. Further technologies like digital footprinting, device intelligence, and transaction monitoring augment and support the fight against APP fraud by delivering invaluable contextual insights into user behaviors and potential security risks.

A comprehensive approach supported by a fraud prevention software helps organizations connect these capabilities within a single framework and respond faster to emerging threats.

In combination with technology, the strengthening of regulatory frameworks, along with the active participation of consumers through education and awareness, forms a multi-layered and effective defense mechanism. The journey toward a more secure financial environment is complex, but a safer future is within reach with continuous innovation.

Sources:

- Payments Dive: Authorized payment scams climb in US

- Computer Weekly: APP fraud volumes expected to double by 2026, says report

- Finextra: 2023 APP fraud trends and changing liability at a glance

- Statista: Percentage of organizations worldwide experiencing cyberattacks from 2021 to 2023, by attack type

- EY: New draft Payment Services Regulation: overview of the main differences from PSD2

- Security Magazine: Combatting the next wave of AI fraud

- We Are Pay: Confirmation of Payee