A standard digital commerce merchant typically has one main payment problem, and that’s stopping fraudulent buyers at checkout. A marketplace, however, has two. When a platform connects thousands of sellers with millions of buyers, fraud can enter from both directions simultaneously, and most payment fraud tools are built to catch only one of them.

The buyer checkout flow is where most detection logic lives, and the seller payout flow, where fraudulent sellers extract funds through legitimate-looking transactions, is where most detection logic stops. It is this structural gap that makes payment fraud on two-sided marketplaces a category of its own, and why native payment tools often fall short at scale. Instead, operators today must build a screening layer that protects both sides, without slowing either one down.

Key takeaways

Why Payment Fraud on Marketplaces Differs From Standard eCommerce

A single-sided merchant has one payment flow, in which the buyer submits card details, the payment processor approves or declines and the merchant fulfills the order. Fraud prevention sits at that single checkpoint, which is why tools built for this model work well there. For a full breakdown of payment fraud types and detection methods, see our guide to payment fraud.

A marketplace has at least two flows. Buyers pay in and sellers receive payouts, and each direction carries its own fraud surface. Fraudsters also rarely operate through a single account: coordinated buyer and seller account networks are commonly used to distribute fraud activity, evade bans and manipulate platform trust systems.

A fraudster on a marketplace does not have to target checkout at all — they can create a seller account, build apparent legitimacy through a small number of completed transactions and then exploit the payout flow directly.

The platform, the actual conduit for market exchange, sits between both parties and is responsible for the integrity of the transaction, which is a structural difference from other retail operations that makes detection logic built for single-sided merchants consistently underperform in this context.

The Two Attack Surfaces: Buyer Checkout Fraud vs Seller Payout Fraud

Understanding where fraud enters a marketplace requires separating two distinct attack surfaces, because the detection approach for each is fundamentally different.

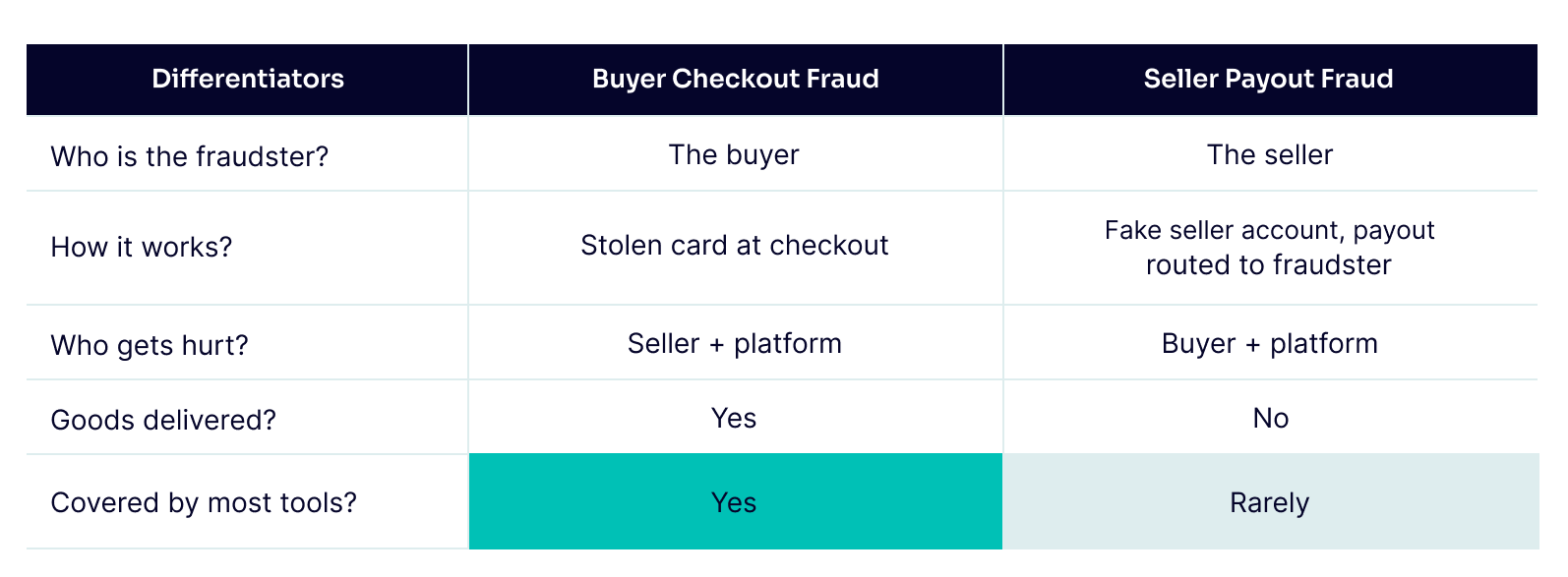

- Buyer checkout fraud follows a familiar pattern where stolen card details are used to make purchases, often for high-value or easily resellable items. The damage lands on the seller, who ships goods that generate chargebacks, and on the platform, which absorbs dispute costs and reputational risk.

- Seller payout fraud is less commonly addressed but equally damaging. In this form of fraud, a fraudster creates a seller account, lists products, processes payments from real buyers using stolen card credentials and routes payouts to a controlled account. Goods are never delivered, chargebacks follow and the platform is left managing disputes and navigating buyer trust damage. Card testing is one of the most common ways fraudsters exploit this flow.

Most payment fraud tools are configured to catch buyer checkout fraud. Catching seller payout fraud requires a separate detection layer, one that evaluates seller account behavior, payout velocity and cross-account signals from the moment of seller registration.

How Card Testing Works on Marketplaces and Why It’s Harder to Catch

Card testing is the process of using stolen card details to make small transactions that confirm whether a card is active before using it for larger fraud initiatives. On a standard eCommerce site, the attack happens at checkout, where multiple small transactions from different cards in a short window trigger velocity rules, and thus the fraudulent action is identified and stopped.

On a marketplace, the attack surface is wider. A fraudster who creates a seller account can use the seller-initiated payment flow to test cards outside the standard checkout path. Because the transactions look like legitimate seller activity rather than suspicious buyer behavior velocity rules calibrated for buyer checkout do not flag the actions, and the cards are validated without detection.

Catching this pattern requires monitoring seller account behavior from registration onward, not just transaction patterns at checkout. Device consistency, email and phone signal quality, payout timing relative to account age and cross-account links to previously flagged sellers are all signals that card testing via seller accounts generates before a single fraudulent transaction completes.

Payment Abuse Patterns Specific to Two-Sided Platforms

- Triangulation fraud exploits the three-party structure of a marketplace by creating an invisible layer between the buyer and the fraudster. A fraudster lists items at competitive prices, collects payment from a legitimate buyer, then purchases the item from a third-party retailer using a stolen card, shipping it to the buyer’s address. The buyer receives the order, the fraudster receives the payout and the legitimate retailer receives the chargeback.

- Promo and referral abuse exploits marketplace incentive structures through multi-accounting: creating multiple buyer or seller accounts to claim referral bonuses or promotional credits repeatedly. Each individual transaction looks legitimate, and the pattern across accounts reveals the abuse — which is why cross-account signal matching is necessary to catch it.

- Refund fraud targets marketplaces with buyer-protection policies by exploiting the asymmetry between buyer protection and seller recourse. A buyer purchases an item, claims non-delivery or a defect, receives a refund and retains the goods. On platforms where the marketplace mediates disputes, fraudsters exploit the gap between what buyers can claim and what sellers can prove.

Acceptance Rate vs Fraud Rate: Why the Trade-Off Is Harder on a Marketplace

Every fraud team manages a trade-off between catching fraud and approving legitimate transactions. On a single-sided eCommerce site, this trade-off affects one population the most, thebuyers. Tighten rules too far and genuine customers are declined; loosen them and fraud gets through.

On a marketplace, the same trade-off affects two populations simultaneously. Aggressive fraud rules at checkout decline legitimate buyers, while aggressive rules at seller onboarding or payout block legitimate sellers. Both outcomes damage the platform, and solving one without considering the other is not a solution.

A marketplace operator processing around three million transactions per year described this tension directly during a product evaluation: the priority was maintaining a high acceptance rate for legitimate transactions while blocking card testing and preventing chargeback liability from accumulating on the seller side. Rule sets that addressed one flow in isolation consistently fell short on the other.

What Marketplace Operators Need That Native Payment Tools Don’t Cover

Most marketplaces start fraud prevention with the tools built into their payment processor. For early-stage platforms with low transaction volume, this is often sufficient. As volume grows, the limitations become structural rather than configurable.

Native payment tools assess transactions in isolation. They do not evaluate seller account behaviour, cross-reference signals across buyer and seller accounts on the same platform or provide the rule customisation required to segment fraud logic by flow type. The cross-account patterns that marketplace fraud rings generate — shared devices, IP clusters, linked phone numbers — are invisible to detection logic that only looks at individual transactions.

The operators who outgrow native tools consistently need the same things: custom rule logic that reflects their specific platform model, real-time signals beyond the transaction itself, cross-account visibility and the ability to adapt detection logic without waiting on vendor roadmaps or engineering cycles.

Build payment fraud detection across both sides of the platform.

Learn How

How to Build a Payment Fraud Prevention Layer for a Two-Sided Platform

Effective payment fraud prevention for marketplaces requires a layered system that covers each point where fraud can enter, applied in real time and continuously after approval.

- At seller registration: email intelligence, phone validation, device fingerprinting and digital footprint analysis establish whether the account behind a new seller is a coherent, legitimate identity. Thin or inconsistent signals at this stage are the earliest indicator of seller payout fraud or card testing risk.

- At buyer checkout: real-time transaction scoring evaluates card details, device signals, IP reputation and behavioral patterns against established baselines. Velocity rules tuned to marketplace-specific patterns reduce false positives for legitimate buyers without loosening controls on high-risk signals.

- At payout: monitoring payout velocity, account age relative to payout timing and destination account signals helps catch fraudulent sellers who passed onboarding and operated legitimately for a short period before exploiting the payout flow.

- Across accounts: cross-account signal matching identifies connections between buyer and seller accounts on the same platform — shared devices, overlapping IP ranges, linked phone numbers — that individual transaction checks cannot surface.

FAQ

What is payment fraud on a marketplace?

Payment fraud on a marketplace includes any fraudulent activity that exploits a platform’s payment flows, such as buyer checkout fraud using stolen card details, seller payout fraud where fraudulent sellers extract platform funds, and card testing run through seller accounts. Unlike single-sided eCommerce, marketplaces face risks from both buyers and sellers simultaneously.

How does card testing work on a marketplace?

On a marketplace, card testing can be run through seller-initiated payment flows rather than standard buyer checkout. A fraudster creates a seller account and uses it to process small transactions with stolen card details outside the checkout path, where buyer-focused velocity rules do not apply. Detection requires monitoring seller account signals from the time of registration onward.

Does buyer-seller messaging create payment fraud risk?

On marketplaces where buyers and sellers communicate directly, the messaging flow carries behavioral signals that matter. A fraudster contacting hundreds of sellers with identical messages, or a seller initiating the same conversation pattern across thousands of buyers, generates cross-account signals that precede any fraudulent transaction — making interaction behavior part of an effective detection layer, not an afterthought.

What is the difference between buyer checkout fraud and seller payout fraud?

Buyer checkout fraud occurs when a fraudster uses stolen card details to make purchases as a buyer. Seller payout fraud occurs when a fraudster creates a seller account, processes payments and routes the payout to a controlled account before delivering goods. Both exploit the marketplace’s payment infrastructure but require different detection approaches because they enter through different flows.

When do marketplaces outgrow native payment fraud tools?

Most platforms outgrow native tools when transaction volume grows, fraud patterns diversify across buyer and seller flows or when false positive rates start affecting legitimate seller acquisition and buyer conversion. The inflection point is when cross-account visibility, segmented rule logic and custom detection thresholds become necessary to maintain platform integrity.

How can a marketplace reduce payment fraud without hurting acceptance rates?

By segmenting fraud logic by flow — separate rules for buyer checkout, seller onboarding and payout processing — and tuning each independently. Cross-account signal matching reduces false positives by distinguishing legitimate users with unusual patterns from fraudsters with consistent fraud signals. Real-time decisioning at each touchpoint means friction is applied only where the risk profile warrants it.