76% of US firms experienced payment fraud in 2025, despite most already running some form of transaction monitoring. The technology exists. It’s the configuration that tends to break down.

Fintechs feel this more than most. Rules get shipped fast and tuned slowly — the default when fraud teams are lean and transaction velocity is high. Thresholds drift, new attack patterns outpace the review cadence and teams end up layering controls without understanding signal quality. It is how a rule engine becomes operationally expensive to run and nearly impossible to audit.

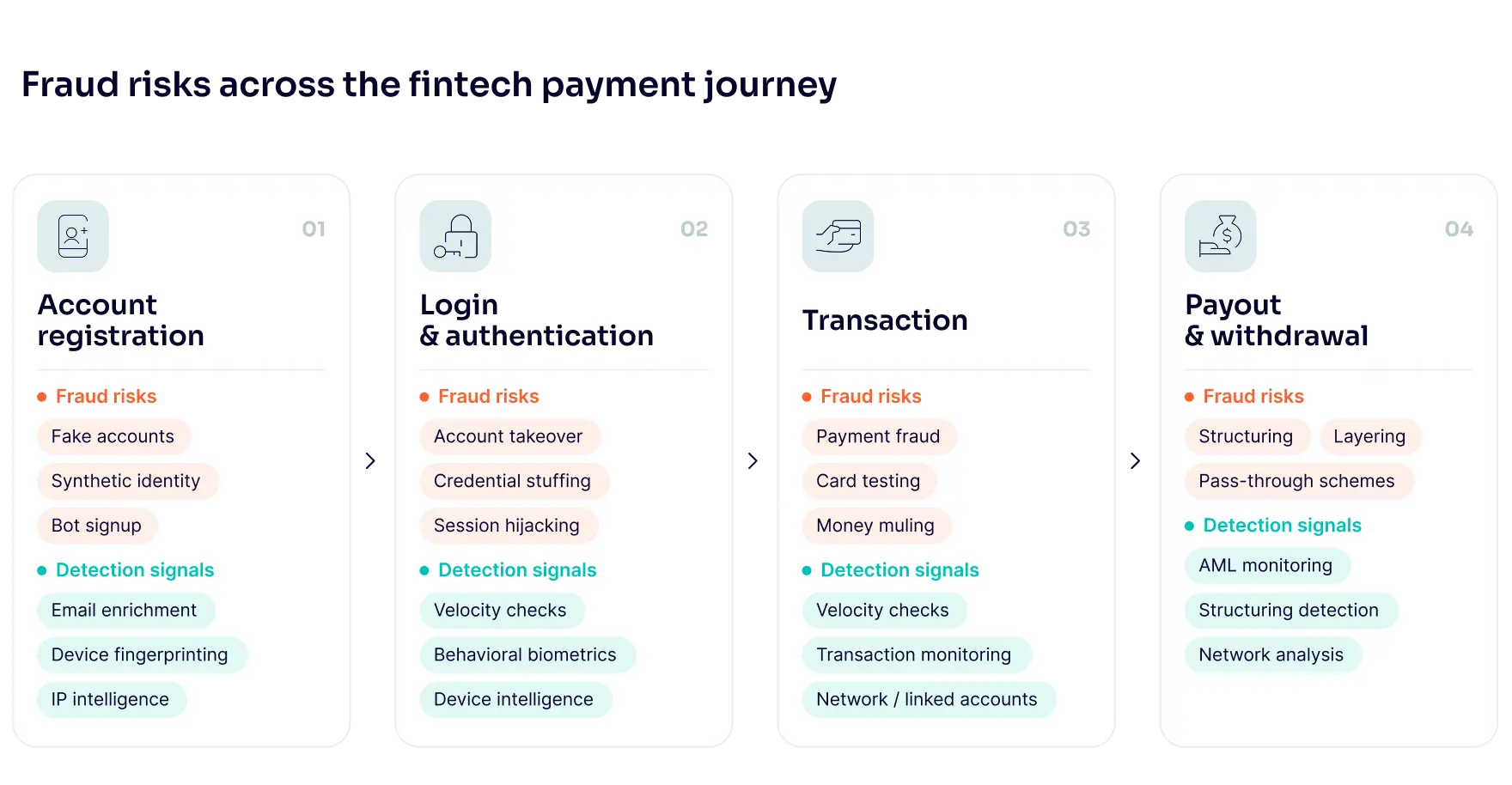

The rule types below are where this gap does the most damage and where getting the implementation right has a measurable impact on both fraud losses and the customers caught in the crossfire.

Key Insights

More rules don’t equal better fraud protection. Signal quality determines whether a rule catches fraud or generates review volume, and false positives carry the same operational weight as misses: every blocked legitimate user is a churn event, and every unnecessary alert is analyst time diverted from genuine investigation.

Rules and machine learning work best together because they cover different ground, but in either approach, the ceiling is composite scoring. Device, IP, email and behavioral signals need to stack before a rule becomes actionable.

Why Rule Logic Still Outperforms Blackbox Machine Learning Alone

Rules and machine learning complement each other, each filling the gaps left by the other.

When a new fraud typology surfaces, a tuned rule fires within hours. A machine learning model trained on historical data needs volume before it shifts, and the lag between the two timelines costs money. Every fraudulent transaction completed is a chargeback or a write-off, and the speed of detection is exactly where rule-based logic earns its commercial case.

Rules also encode institutional knowledge about known patterns, documented in a form regulators can inspect. FinCEN, FCA and EBA all expect explainable monitoring logic, and a decision-making process without a defined, human-authored rule behind it creates compliance exposure rather than a control.

Rules, however, do have a real limitation: they’re brittle against novel attacks. Fraud patterns with no prior representation slip through defined logic, and ML fills the gap, handling behavioral drift and surfacing anomalies the rules weren’t built to recognize. The strongest fraud stacks run both deliberately.

Most fintech fraud teams have more rules than answers. Schedule a quick call with one of our fraud experts to find out exactly which controls are earning their place and sharpen the ones that aren’t.

Speak with an expert

The 8 Rule Types Worth Getting Right

Here are the rule categories with the highest signal quality and the widest gap between a well-implemented version and a poorly calibrated one. Each maps to a specific fraud behavior and each has a predictable failure mode worth understanding before the rule goes live.

1. Velocity Checks

Velocity checks are the most fundamental fraud control in payments — and one of the most frequently miscalibrated. They catch fraud that depends on speed and repetition, specifically any attack pattern that requires a high volume of the same action in a short window.

The underlying principle is straightforward: measure how often a specific action occurs from a specific device, IP or account within a defined time period and flag when that rate falls outside the normal range for that user cohort. A reliable indicator for card testing, for example, is a notable spike in low-value transactions from the same device within a short window.

The failure mode here is almost always a flat threshold applied across all users. A threshold calibrated for a consumer app will over-block on a platform serving high-volume merchants, and vice versa. Cohort-based thresholds — segmented by account type, tenure and expected behavior — are what separate a velocity rule that protects from one that penalizes.

2. Device Fingerprinting

Device fingerprinting identifies and tracks unique device characteristics across sessions, independent of cookie state or browser resets. It catches bot attacks and multi-accounting precisely because those attack types depend on creating the appearance of distinct users on the same underlying infrastructure.

The highest-precision signal in this category is a session originating from an emulator or virtual machine rather than a genuine consumer device. This distinction has a low false positive rate and a high fraud rate. A more nuanced pattern worth building detection around is a single device fingerprint appearing across multiple distinct user accounts within a defined window, which surfaces coordinated multi-accounting more reliably than per-account analysis alone.

A common implementation gap is over-reliance on cookie-based identifiers. A determined fraudster clears cookies in seconds. Hardware-level fingerprinting, combined with software telemetry and behavioral data, is a meaningfully different category of control, and the combination produces a signal that’s significantly harder to spoof.

3. IP Intelligence

IP intelligence catches location spoofing, account takeover attempts and sanctions evasion by evaluating the source and nature of the IP behind each session. The signal is in the classification, not just the IP itself.

Not all high-risk IP traffic carries the same risk profile. Traffic routed through a Tor exit node warrants a categorical block at most fintechs. A datacenter IP on a first-time account with no prior history is a different signal, one that warrants review rather than an automatic block. Treating both scenarios identically wastes review capacity on the wrong cases and misses the distinction that actually matters operationally.

The false positive risk is concentrated among legitimate VPN users: privacy-conscious individuals and employees on corporate networks who will trigger overly broad IP rules with no fraudulent intent. Proxy type classification is what makes the difference. Routing residential proxy traffic to step-up authentication rather than a hard block preserves the customer relationship while still adding friction where the signal warrants it.

4. Digital Footprint Analysis / Email & Phone Enrichment

Legitimate users leave evidence, aka a digital footprint, of an existing online presence. A manufactured, synthetic identity leaves far less of a trace than a real one.

The core indicators are straightforward to monitor. An email address registered within the past 48 hours used in a high-value transaction is a meaningful risk signal in itself. A phone number that resolves to a VOIP carrier on a newly created account adds a second layer. This combination appears consistently in synthetic identity cases and rarely in genuine consumer behavior. Synthetic identity fraud costs an estimated $20–40 billion globally per year (BIIA, 2026), and a significant share of those cases leave exactly these kinds of footprint signals before the fraud completes.

The risk in over-indexing here is real. Users with minimal social presence — whether by choice or circumstance — share some surface characteristics with synthetic identities. A new email address is a risk signal, not a block condition. The signal becomes actionable when it stacks with device and IP context: a new email on a clean residential device is a different profile entirely from that same email arriving from a datacenter IP on an emulated device.

5. Behavioral Biometrics

Behavioral biometrics catch what other signals can’t: fraud happening during an active session, in real time, from an account that may otherwise look clean.

The signals are passive, collected during normal user interaction without adding friction. Two patterns have consistently high signal reliability. A full registration form completed in under two seconds falls outside the range of any real human user — the speed alone is a reliable bot indicator. In-session navigation that matches known remote access tool profiles, characterized by controlled and direct movement with no natural variation, is a strong account takeover signal that warrants an immediate response rather than a queued review.

The implementation risk is in baselining too broadly. Mobile users on touchscreens produce fundamentally different behavioral signatures than desktop users with a mouse, and a global baseline generates both false positives and false negatives. Channel- and device-specific baselines make the signal precise rather than noisy.

6. AML Transaction Monitoring

AML transaction monitoring rules catch layering, money muling and payment patterns designed to stay below regulatory reporting thresholds. This is also the rule category with the most explicit regulatory expectations attached to it.

FinCEN requires transaction monitoring programs with defined thresholds and documented logic for suspicious activity. The FCA’s PS19/26 sets equivalent requirements for UK-registered fintechs. Velocity rules that flag multiple transfers clustering just below the reporting threshold within a 24-hour window surface SAR candidates before the activity completes.

The tuning challenge is genuine. Round-number transactions and sub-threshold transfers occur regularly in legitimate payroll and vendor payments, so segmenting by counterparty type and relationship age keeps the rule precise.

7. Synthetic Identity Signals

Synthetic identity fraud in fintech targets account opening. The goal is to pass KYC with a fabricated or composite identity, establish an account that looks legitimate, then use it to commit payment fraud or exploit product features before the identity unravels.

The detection challenge is the same regardless of the fraud that follows: no single signal identifies a synthetic identity. A new email address, a VOIP phone number and a minimal digital footprint are individually explainable. Together, combined with device signals and IP context, they form a risk profile that looks very different from a genuine new customer. The composite picture is what makes the call.

Calibration matters here because the false positive risk is real. Users with limited social presence — recent arrivals to a market, younger users with thin digital histories — share surface characteristics with fabricated identities. A composite score calibrated against your actual customer base yields a meaningfully lower false positive rate than any single-signal block.

8. Network / Linked Account Detection

Fraud rings, multi-accounting and referral abuse are invisible at the individual account level. The accounts involved are often clean in isolation, and the signal only appears when they’re connected.

Linked account detection works by building a cross-account view across shared device identifiers, payment instruments and behavioral clusters. A payment method appearing across more than two distinct user accounts is a signal worth investigating. A more specific pattern: a referral bonus claimed by two accounts sharing the same device fingerprint. Legitimate household device sharing exists, but that pattern at scale is engineered abuse rather than coincidence — and the difference is measurable.

The ceiling in most rule engines is that they operate per account, not per network. Catching fraud rings requires a graph view: a shared device ID alone is not conclusive, but a shared device ID linked to a previously flagged account and a newly registered email is a strong signal of a fraud ring. This is where rule logic and ML genuinely work in combination: rules surface the connection, ML scores the cluster and prioritizes the review.

The False Positive Problem

False positives carry a real operational cost, and most fraud programs undercount it. Every manual review consumes analyst time that could go toward genuine investigation. Every declined legitimate user is a customer who has a reason to leave. A rule firing 500 times a day at a 2% true positive rate generates 490 unnecessary reviews, and over time, that volume conditions analysts to treat every alert as noise, which is how real fraud finds room to hide.

Precision is what addresses this, and it comes down to measurement. Every live rule should have a defined expected true-positive rate and get audited against it on a regular cadence. Cohort-based thresholds and signal stacking improve that rate without reducing coverage. Trigger volume tells you how busy the queue is, and precision tells you whether the program is actually working.

What SEON Brings to Your Rule Engine

SEON’s AI platform for fraud prevention and AML compliance brings together 900+ first-party data points across devices, IP addresses, email and phone numbers.

Device Intelligence combines hardware fingerprinting with behavioral biometrics in a single SDK that covers web and native mobile environments. IP Intelligence classifies the connection type for every session, providing teams with the proxy context they need. Email and phone enrichment runs 250+ checks per address, covering domain age and social presence to surface synthetic identities at the point of onboarding.

The rule engine uses a natural-language builder, so fraud and risk teams can configure and tune logic without an engineering dependency. Machine learning runs alongside it, picking up behavioral patterns that fall outside the rule set, with every output fully explainable and audit-ready. Link analysis builds a cross-account graph across shared identifiers and payment instruments, surfacing coordination patterns that only become visible at the network level. AML Screening covers PEP and sanctions checks alongside transaction monitoring in a single workflow, with documented decision logic that satisfies FinCEN and FCA requirements.

FAQ

What is the difference between a fraud rule and a fraud model?

A fraud rule is a human-authored logical condition: if this signal is present, take this action. A fraud model is a statistical algorithm trained on historical data to estimate the probability of fraud. Rules are explicit, auditable and fast to deploy — models handle behavioral drift and surface anomalies that haven’t been formally defined. Mature fraud stacks run both.

How do velocity checks work in fraud prevention?

Velocity checks measure how many times a specific action occurs within a defined time window from a specific device, IP or account. When that count exceeds a defined threshold, the rule triggers a review or block. Thresholds need to be calibrated per user cohort.

What are the most common causes of false positives in payment fraud detection?

Flat thresholds applied across all users, regardless of account type or expected behavior. Overly broad IP blocking on VPN traffic is a close second, as it generates friction for corporate and privacy-conscious users without reducing fraud rates. Both problems stem from the same root cause: rules built without cohort segmentation.

How do you reduce false positives in a fintech fraud rule engine?

Segmenting thresholds by user cohort is the highest-impact fix. A threshold calibrated for one account type will over-block on another. Beyond segmentation, stacking signals rather than acting on any single indicator improves precision without reducing coverage. Regular per-rule audits that track true positive rate, not just trigger volume, are what keep the engine accurate as the product scales.