Digital wallets make checkout faster and more convenient, but that speed also creates new openings for fraud. As adoption grows, so do attacks that target wallet accounts, linked payment methods, and the blind spots created by tokenized transactions.

In this article, we’ll break down what digital wallet fraud is, the most common ways it happens (from account takeovers to wallet-enabled friendly fraud), and the practical steps merchants and wallet providers can take to prevent it and reduce chargebacks, without adding unnecessary friction for legitimate users.

What Is a Digital Wallet (and How Does It Work)

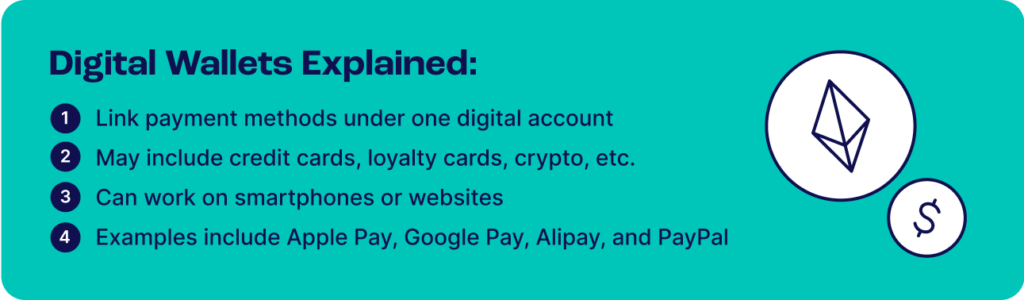

Digital wallets let you link all your payment methods under one account. This account can store credit card numbers but also funds or even cryptocurrencies. It’s accessible online, through your smartphone, or through a website.

To pay with a digital wallet, you must have an account, top up the wallet, or link it to a working credit or debit card number. You can also store discount codes and coupons, among others.

You’ll find the option to use your digital wallet at checkout when you pay online. Most POS (Point of Sale) terminals, now also support digital wallet payments.A key feature of digital wallets is that transaction data is encrypted and tokenized (turning sensitive data into a token – or non-sensitive digital equivalent). This improves privacy and security but also makes it harder for merchants to spot credit card fraud.

The Most Popular Digital Wallets

According to Statista, digital wallets account for nearly half of all online payments worldwide. Usage is led by China, where Alipay has over 1.3 billion recurring users, followed by WeChat Pay.

Outside China, Apple Pay is the most widely used wallet in Western markets, with Google Pay and Samsung Pay also among the top options. PayPal remains the most popular e-wallet not tied to a specific device ecosystem, followed by Paytm in India.

Are Digital Wallets Safe?

When it comes to high risk payment methods, digital wallets are one of the most secure and safe for individuals. This is because payments are encrypted and tokenized, making it virtually impossible for attackers to steal your money during a transaction.

However, the weakest link in that chain is your account’s login details. If someone manages to usurp your login information, they can access your digital wallet and drain it of funds.

What Are the Risks of Digital Wallets?

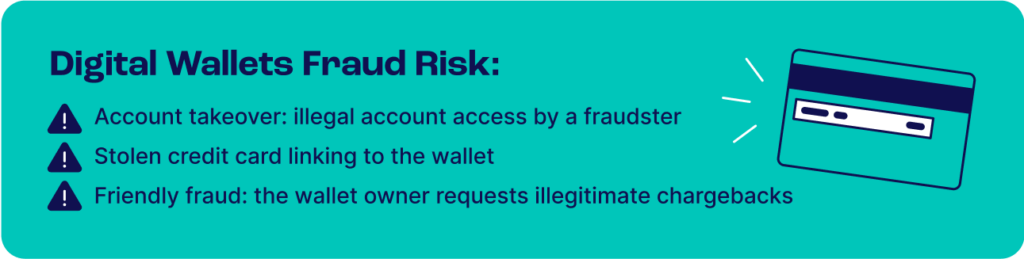

Digital wallets are often safer than traditional card-not-present payments, but they still carry real risks for both users and merchants. The main threats typically fall into four buckets: account takeover, stolen payment methods, friendly fraud and scams.

1. Digital Wallet Account Takeover

The main risk of a digital wallet is that the account may fall into the wrong hands. This is called an account takeover, and it tends to happen for one of the following reasons:

- Targeted attack: A fraudster has set their eyes on an account and targeted the owner through spearphishing (targeted phishing) to get them to enter your account details on a fake website. Malware can also be deployed to log the account name and password.

- Credential harvesting and credential stuffing: Groups of fraudsters have obtained lists of login details from data breaches, and they use bots to try every variation possible systematically. Since password reuse is common, the breach doesn’t have to be linked directly to the specific digital wallet service to yield results.

Note that opportunistic fraudsters may also strike if you accidentally leave your digital wallet account unlocked somewhere – for instance, on a lost device or a public or shared computer.

2. Stolen Cards Added to Digital Wallets

Unfortunately, digital wallets make it a lot harder for merchants to flag transactions made with stolen credit cards. Because the transaction appears as a token instead of the credit card number, fraudsters can simply move their operations to a different account if they get blocked, or add a new stolen card to peruse.

In this way, the online wallet functions somewhat like a bank drop, where the fraudster is layering stolen funds to allow it to enter the financial system without any issues.

In fact, the lack of friction and security checks involved with adding a credit card payment to a digital wallet is quickly making them the top vehicle for transaction fraud online – up by 200% in Q1 2022 alone, according to statistics by Sift, as reported by The Fintech Times.

This is very much unlike paying with your card directly, where SCA calls for additional checks and verification.

3. Digital Wallet Friendly Fraud and Chargebacks

Last but not least, digital wallets also add to the challenge of dealing with friendly fraud, often making its appearance as refund abuse or dishonest chargeback requests – all made by the legitimate cardholder.

The reason why chargeback fraud enabled by digital wallets is such a big pain point is that merchants already struggle to prove they did nothing wrong with normal chargebacks, and the burden of proof is on them rather than the customer. Digital wallets add a layer of opacity, which gives merchants even fewer data points to work with during a dispute.

As a result, a merchant approached for a chargeback for a payment made via digital wallet is even less likely to be able to prove they did everything by the book, highlighting the need for effective chargeback fraud prevention measures.

4. Digital Wallet Scams (Phishing and Impersonation)

Finally, fraudsters have also been known to impersonate banks and fintech companies to phish for information. In a famous example, a fraud expert was convinced to submit their information ostensibly to create a Capital One digital wallet, which turned out to be a fraudulent scheme.

Similarly, you can imagine how fraudsters leverage the confusion of people who have never set up a digital wallet before or lost their login details. Because the technology is fairly new, bad actors have no trouble getting less tech-savvy users to share their login information.

How to Prevent Digital Wallet Fraud

For consumers, protecting a digital wallet is similar to securing any online account: avoid password reuse, enable multi-factor authentication or biometrics, and stay alert for phishing attempts.

For online merchants and fintechs, the real challenge is preventing digital wallet fraud without frustrating legitimate customers. That requires adding context to key actions, so you can tell normal behavior from risk signals in real time.

- Monitor signups: Fraudsters try to look like regular users, but early signals like VPN usage, emulators, virtual machines, or disposable emails can often be detected from the first interaction.

- Strengthen identity verification: Wallets authenticate users, but adding step-up ID checks at key moments (like adding a new payment method or changing account details) helps stop fraudsters who slip past basic login controls.

- Connect the dots with device intelligence: Fraudsters can rotate emails, cards, and IPs, but devices still leave consistent fingerprints that help link related accounts and transactions.

- Use real-time risk scoring and pattern detection: Static rules struggle with bots, stolen credentials, and fast-changing tactics. Signal-based models can spot suspicious patterns and connections that humans (and simple rules) often miss.

(For more on building real-time risk operations, including fast decisions, transparent scoring, and automation at scale, read out thought leadership piece: Strategies for Managing Real-Time Payments Risk)

How SEON Can Tackle Digital Wallet Fraud

Digital wallets are an obvious target for fraudsters, who hide behind disposable emails, burner phones and masked IPs. SEON makes those disguises harder to pull off.

Starting from a single data point, such as an email address, phone number or IP, SEON’s platform uncovers hundreds of digital signals across social networks, marketplaces and domain data — giving wallet providers the context to tell fake accounts from real customers before money moves.

Fraudsters may cycle through identities, but they can’t hide their devices and setups. SEON detects emulators, virtual machines and spoofed environments in real time, flagging suspicious accounts before they can cause harm.

The result is a risk score tailored to each user and transaction, powered by AI and machine learning models to enhance decision-making. Teams get both speed and clarity: the ability to block fraud at scale while letting genuine customers move through the flow without friction.

FAQ

Mobile wallet fraud happens when fraudsters take over your digital wallet account. Another scenario is that fraudsters use mobile wallets to pay with stolen credit card numbers, which is hard to detect for online merchants.

All digital wallets tend to be secure thanks to their encryption and tokenization technology. The weakest link would be the login stage, which should be protected by 2FA, MFA or biometrics.

Sources

- Business of Apps: Mobile Payments App Revenue and Usage Statistics (2022)

- The Fintech Times: Digital Wallet Payment Fraud up by 200% In Q1 2022 Finds Sift

- LinkedIn: How a Fraud Expert Fell For a Fraud Scam