As technology rapidly advances, fraud prevention must evolve to counter sophisticated cyber threats. Traditional methods like OTP, static passwords and 2FA, once the bedrock of security, now struggle against modern cybercriminal tactics. At the same time, companies face pressure to deliver a seamless digital experience, as today’s users demand fast, frictionless interactions.

This calls for a shift toward digital-centric fraud prevention that leverages contemporary tools like digital footprint analysis to meet the needs of a digital-native generation.

Rising Digital Fraud: Combatting with Footprint Intelligence

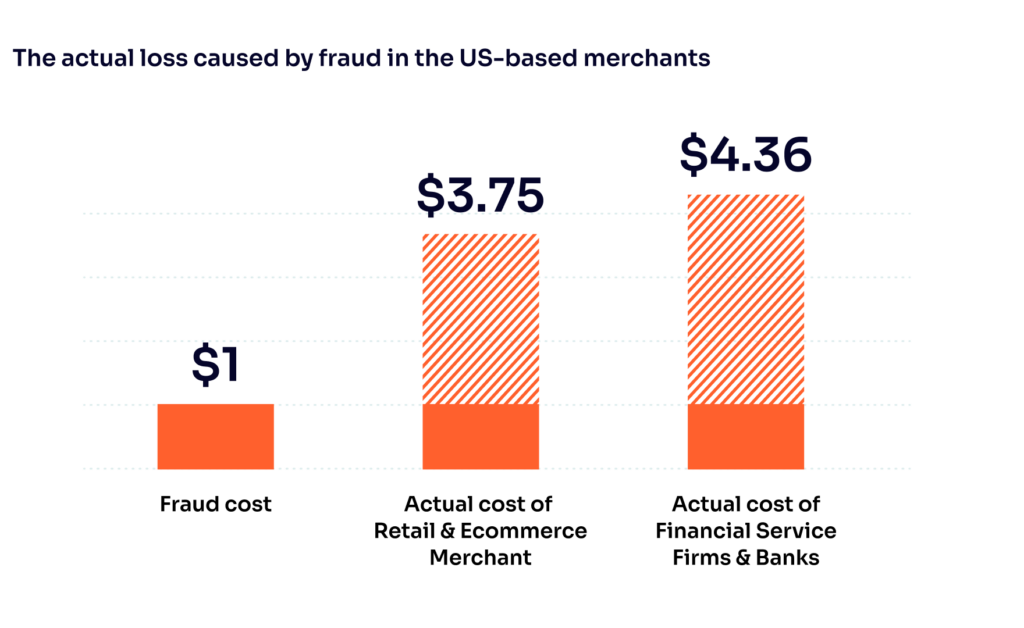

The digital age has ushered in a seismic shift in fraud, marked by increased costs and volume of fraudulent activities. For US-based retail and eCommerce merchants, every dollar lost to fraud now costs $3.75, which climbs to $4.36 for financial service firms and banks. With global fraud expenses soaring to $5.13 trillion annually, reflecting a 56% increase over the past decade, the urgency to address digital fraud has never been more acute.

This escalation is not merely a reflection of economic cycles but a direct consequence of advanced techniques cybercriminals employ to exploit digital vulnerabilities. For example, artificial intelligence (AI), machine learning (ML) and generative tools used alongside advanced data analysis can forge new, difficult-to-detect fraudulent schemes, including AI-based scams like creating synthetic identities, generating false information and sending out large-batch impersonation-based phishing messages. Digital footprint analysis plays a crucial role in identifying and mitigating such schemes, enabling a proactive approach to fraud prevention.

Fraudsters now have various tools to creatively combine accurate data with manufactured information to avoid suspicion, elude credit monitoring or fly under the radar of human analysts and risk teams. Additionally, the volume, variety and sophistication of fraud attacks can be attributed to modern technology fueling old scams while simultaneously making targeting more individuals online straightforward and lucrative.

Digital Footprint Analysis as a Critical Assessment Tool

As businesses bleed 5% of their annual revenues to fraud, the imperative to reassess and fortify their fraud prevention strategies mounts. The rise in fraud, including the growth of phishing attacks and synthetic identity fraud, demands more than what conventional fraud prevention techniques can offer.

At the heart of this new era of fraud prevention lies digital footprint analysis, a pivotal solution to these challenges. The process involves collecting and analyzing information generated by an individual’s online presence and activities, utilizing real-time data and a broad spectrum of social and digital signals. This layer of fraud prevention enhances the validation of customer details, allowing for more effective and efficient differentiation between legitimate and fraudulent transactions.

By conducting a digital footprint assessment, companies can achieve unprecedented accuracy, speed and precision with their fraud prevention, stopping fraud earlier in the journey by leveraging unmatched customer insights without introducing friction.

“By analyzing a user’s digital footprint at the point of registration, businesses gain critical context that traditional KYC simply misses.”

— Nauman Abuzar, Director of Product, AML & Risk Solutions

Examples of How to Use Digital Footprint Analysis

Transcending traditional verification methods by leveraging the complex web of digital traces that individuals leave online, digital footprint analysis holds a variety of applications to combat and mitigate fraud. From reverse email lookup and phone lookup to verification, IP lookup to device intelligence, digital footprint analysis is the most comprehensive online identity check, incorporating real-time behavioral data for quicker detection.

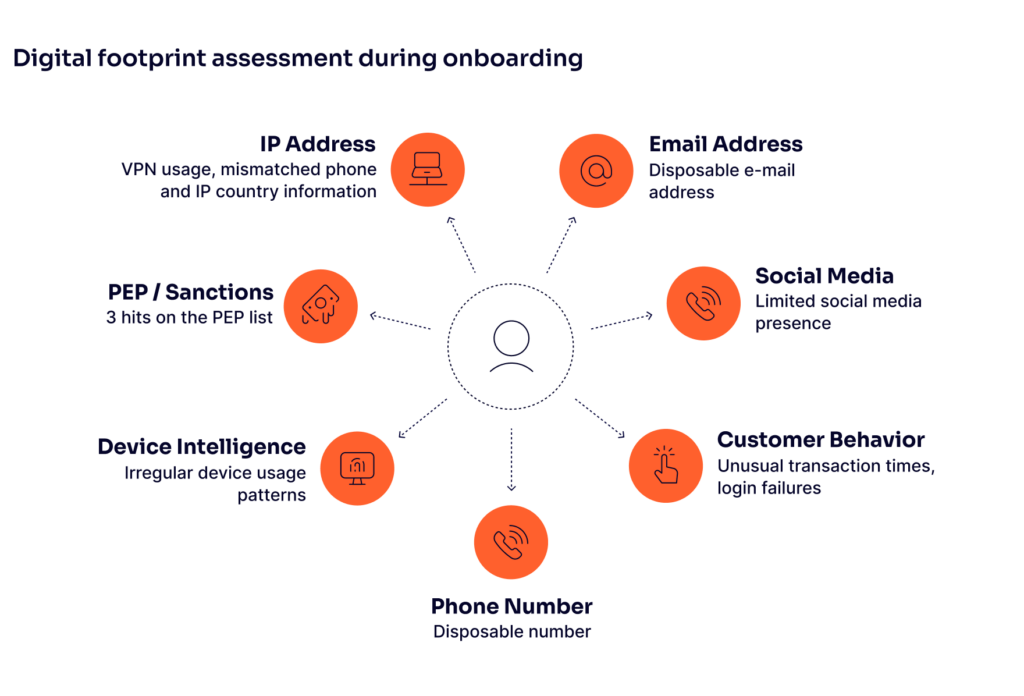

For instance, digital footprint assessment during the onboarding process can scrutinize patterns that may indicate fraudulent behavior, such as the use of mass-generated emails with similar naming conventions or the recurrence of shared password hashes among different users – indicators that are often overlooked by conventional systems but are red flags for fraud rings attempting to infiltrate a platform.

Beyond onboarding, digital footprint analysis strengthens overall risk assessment by giving companies a clearer view of how a user behaves online. That makes it easier to gauge both fraud risk and, in some cases, financial reliability. Because fraudsters rely on speed, even small amounts of early friction can push them toward easier targets — and a strong digital footprint check creates exactly that.

This approach is especially valuable in cash-based markets where traditional credit histories are limited. With more than 1.4 billion unbanked adults globally — including 7.1 million households in the US — digital and social signals offer a powerful way to verify legitimate customers and filter out bad actors using as little as an email address or phone number.

Advancing Fraud Prevention

Technologies such as AI and ML are essential in effectively utilizing the copious amount of data captured by digital footprint monitoring. These tools – the same ones used to orchestrate more complex fraud schemes – can now be harnessed to detect fraud more quickly, identify patterns with greater accuracy and enhance overall efficacy in the fraud prevention lifecycle.

Blackbox machine learning is common today, referring to the decision-making process where data inputs are processed and outputs generated without revealing the underlying logic or rationale. While blackbox ML can deliver rapid fraud scores, its opaque nature offers little insight into the decision-making process, making refining or adjusting risk thresholds challenging.

Conversely, whitebox machine learning provides a transparent and interpretable approach. It delivers decisions and explains the logic behind them and a breakdown of the process followed to reach them. This clarity underpins the ability for fraud prevention measures to be customized to align with the company’s specific risk tolerance, ensuring that security measures do not hinder the user experience.

By integrating blackbox and whitebox ML – an approach championed by SEON – organizations can achieve a balanced approach that prioritizes transparency and adaptability. This dual strategy leverages the power of digital footprint analysis to fuel a customizable rules engine, enhancing the capacity for real-time analysis and comprehensive decision-making. Such a methodology mitigates the risk of false positives and contextless correlations typically associated with blackbox models and fosters trust and engagement in digital platforms by aligning the imperative for security measures with the modern consumer’s expectation for a seamless digital experience.

Preparing for the Future

The future of fraud prevention is not static; it is a continuous battle against evolving threats. As digital natives produce more robust digital footprints and new technologies emerge in lockstep, fraud prevention solutions must remain agile, adapting to the increasing signals of our digital-first world.

Adapt your fraud prevention strategies with digital footprint analysis and advanced machine learning to stay ahead in the digital age.

Speak with an Expert

Additional Sources

- TotalRetail: Fraud is Taking a Financial Toll on the Retail Industry

- Crowe: Fraud costs the global economy over US$5 trillion

- Acfe: Organizations Worldwide Lose Trillions of Dollars to Occupational Fraud

- Worldbank

- Federal Deposit Insurance Corporation: How America Banks: Household Use of Banking and Financial Services