KYC verification is often time-consuming, costly, and frustrating for customers — yet it remains surprisingly easy for fraudsters to bypass. This friction during onboarding leads to higher churn rates and demands significant resources to manage.

Globally, KYC standards are shaped by anti-money-laundering (AML) laws such as the Bank Secrecy Act and USA PATRIOT Act in the US, the EU’s AML Directives, and the UK’s Money Laundering Regulations. Despite regional differences, all aim to prevent money laundering, terrorist financing, and identity fraud through proper identity checks and continuous monitoring.

For banks, the average annual cost of Know Your Customer (KYC) checks exceeds $60 million, driven by the need for comprehensive verification, ongoing due diligence, and compliance. The process typically includes three components: Customer Identification Program (CIP), Customer Due Diligence (CDD), and ongoing monitoring.

What Is KYC Verification?

Know Your Customer verification is the process of confirming a customer’s identity to ensure they are who they claim to be. It’s a fundamental part of KYC and AML compliance, helping regulated organizations like fintechs, gambling organizations and financial institutions meet regulatory obligations while protecting themselves from fraud.

During KYC verification, a customer’s personally identifiable information (PII) — such as their name, date of birth, and address — is validated against official documents like passports, ID cards, or driver’s licenses. Depending on the organization’s risk tolerance and regulatory expectations, this may be supplemented with biometric checks, database lookups and AML screening against sanctions and watchlists.

However, verifying identity alone does not guarantee trustworthiness. As fraud increasingly involves real, stolen or AI-generated identities, effective KYC verification must also consider whether a customer’s behavior and activity align with legitimate use. This broader risk perspective is what allows KYC programs to move beyond formality and into practical risk detection and fraud prevention.

How Does KYC Verification Work?

To complete KYC verification, businesses must follow these key steps:

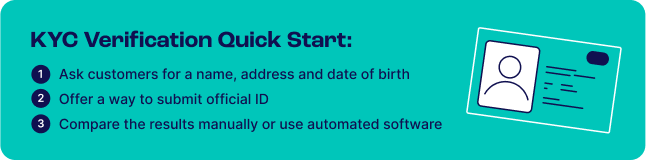

- Collect customer details: Request essential information like name, address and date of birth.

- Obtain official ID documents: Ask for government-issued identification (e.g., passport, driver’s license).

- Cross-check information: Compare the provided details with the ID documents and other biometric information to ensure they match.

Once these checks are complete, the organization determines whether the applicant can be approved, requires further review or should be rejected.

Cross-Checking Methods

The verification process can vary depending on automation levels:

- Automated checks – Some organizations use identity verification (IDV) software to scan and extract details from ID documents.

- Manual review – Others prefer human oversight, where documents are checked visually for inconsistencies.

- Hybrid approach – Combining software detection and human verification improves accuracy and helps spot tampered documents.

KYC verification is complete when the organization confirms the applicant’s eligibility and approves them for onboarding.

Why Is KYC Verification Important?

The KYC process is essential for businesses to maintain compliance and prevent fraud. Without it, businesses lack visibility into who they are onboarding and how those customers may behave over time, helping organizations.

- Establish defensible identity standards

- Detect higher-risk customers earlier before KYC

- Allocate investigative resources more effectively

- Maintain oversight as customer behavior changes

KYC software is not a guarantee against fraud or regulatory action. Rather, it provides a structured framework and controls process for identifying, assessing and responding to risk in a consistent way.

3 Components for a Successful KYC Verification

A successful KYC verification process involves three key steps: a customer identification program (CIP), customer due diligence and ongoing monitoring.

1. Customer Identification Program (CIP)

The CIP requirement stems from the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism (USA PATRIOT) Act of 2001. The Act’s goal is to deter and punish terrorist acts in the US and globally, including by strengthening anti-money laundering measures.

For financial institutions, this means verifying the identity of account holders. An individual can open an account with basic details (name, date of birth, address, and identification number). The financial institution must then verify those details, for example by checking the individual’s identity documents and/or looking them up on public databases, consumer reporting agencies, and similar.

2. Customer Due Diligence

The next step of the KYC verification process concerns assessing the customer’s trustworthiness. At the simplified due diligence end of the scale, it may be sufficient to verify the customer’s identity and location. Enhanced due diligence takes this further, including checking blacklists, watchlists and lists of politically exposed persons (PEPs).

Customer due diligence can also delve into an individual’s occupation, the types of transactions they make, their expected activity patterns, and more. The goal is for the financial institution to understand the particular risks associated with that individual while keeping detailed records of the checks undertaken.

3. Ongoing Monitoring

A successful KYC verification process is not a one-time activity. Monitoring must continue throughout a customer’s time with the financial institution in question. Ongoing monitoring flags changes in activity patterns: these could include unusual cross-border payments, higher-value transactions, changing payment methods, a higher volume of transactions and/or the addition of the account holder to a sanction list. The financial institution may need to file a Suspicious Activity Report if an account holder’s behavior changes sufficiently to warrant this.

Best Features for KYC Verification Processes

Effective KYC verification depends less on individual tools and more on how well signals, workflows and decisions work together. Modern KYC systems must support depth, flexibility and context across the entire verification process.

Depth and Breadth of Fraud Signal Intelligence

Identity documents alone rarely provide enough context to assess risk. A strong KYC system evaluates identity alongside a broad set of fraud signals, including device behavior, network characteristics, digital footprint and usage patterns.

These signals help answer questions documents cannot: whether an identity has a credible digital history, whether the device has been seen before and whether the behavior surrounding the verification attempt aligns with legitimate use. Greater fraud signal depth improves detection accuracy and reduces reliance on traditional verification protocols that only provide surface level context.

Flexible, No-Code Verification Workflows

Changing regulatory requirements, risk tolerances and business expansion can result in the need for new KYC workflows. KYC systems must allow teams to adapt verification flows quickly without engineering support to ensure regulatory compliance, risk mitigation and the ability to scale.

No-code workflow builders enable compliance and fraud teams to define when verification is required, which checks apply and how exceptions are handled, based on risk, geography, regulation or other factors. This flexibility allows organizations to respond quickly to regulatory updates and evolving fraud patterns without rebuilding integrations or disrupting legitimate users.

Granular AML Screening with Contextual Inputs

AML screening is most effective when it uses more than static name matching. Advanced screening systems apply granular detection logic, fuzzy matching and risk weighting to reduce false positives.

When AML screening incorporates inputs from official documents from identity verification, alert quality flagging AML hits improves significantly. This reduces unnecessary reviews while maintaining robust coverage against sanctions, PEPs and watchlists.

Unified Risk Decisioning and Case Management

Fragmented tools create fragmented decisions. Operationally efficient KYC programs rely on KYC orchestration to centralize identity, fraud and AML signals within a single system.

A unified view allows teams to assess risk holistically, apply consistent rules and maintain a clear audit trail across onboarding and ongoing monitoring. Centralized case management ensures decisions are explainable, repeatable and easier to defend internally and externally.

How to Save on KYC Costs with Pre-KYC Checks

KYC checks can be expensive, particularly when expensive identity checks are applied uniformly. One way to control speond is to identify high-risk users before they upload KYC documents.

SEON can be used at signup as an early screening step using digital footprint and device intelligence signals, helping filter out suspicious activity so only higher-quality applicants move forward to KYC. This ensures that full verification is reserved for applicants who warrant it, reducing both cost and analyst workload.

This doesn’t just reduce KYC costs. It also lowers fraud exposure across your platform by blocking bad actors earlier in the journey. As explained in our guide on screening before KYC:

“By analyzing a user’s digital footprint at the point of registration, businesses gain critical context that traditional KYC simply misses.” – Nauman Abuzar, Director of Product, AML & Risk Solutions

How SEON Can Augment Your KYC Verification

SEON augments KYC by providing context alongside the identity verification,, helping teams apply risk controls more selectively. Here’s how SEON can help organizations verify identities while assessing user intent to ensure legitimate users enter your platform.

- Understand user intent, not just verify documents, using fraud signal intelligence

- Cut KYC costs and detect bad actors early before ID documents are captured

- Build custom identity verification workflows without code, eliminating engineering lift

- Apply dynamic friction by delaying KYC for low risk users (if regulations allow it) and tightening friction for high risk users.

- See one hollistic risk decision and audit trail for all identity checks, making all KYC outcomes defensible

This also lays the foundation for expanding financial services capabilities. For example, loan providers seeking to implement alternative credit scoring through digital ID profiling no longer need to rely on traditional financial data. Instead, they can leverage digital footprint analysis to build their scoring models, bypassing the need for information from banks and financial institutions.

By combining fraud, IDV and AML compliance in one KYC solution, regulated businesses can manage rules, risk thresholds and decisioning in one place, creating operational efficiencies for KYC teams, not disparte siloed decisions.

Frequently Asked Questions

How do businesses reduce KYC costs?

Companies reduce KYC costs by screening users before full verification, automating ID checks, and using digital data sources to assess risk early. This helps filter out fraudulent applicants and lowers manual review workloads without compromising compliance.

What tools combine KYC verification with AML screening in one platform?

Modern compliance platforms increasingly merge KYC and AML functions. They verify identities, screen for sanctions and politically exposed persons (PEPs), and monitor transactions in real time — helping compliance teams detect suspicious behavior and maintain audit-ready records efficiently.

What are the best KYC verification solutions for fintech startups?

Fintech startups benefit most from KYC tools that combine fast onboarding with regulatory compliance. The best options automate document checks, biometric verification, and data enrichment, helping reduce manual reviews and onboarding friction while staying aligned with AML and CDD requirements.

Sources

- Financial Crimes Enforcement Network. FinCEN.

- Accenture: Banking Consumer Study: Making digital more human

- World Bank: The Global Findex Database