KYC (Know Your Customer) is a critical requirement for online lenders, ensuring that loan applicants are trustworthy before disbursing funds. However, executing an effective KYC process involves more than just compliance — it requires careful consideration of various factors to safeguard both lenders and borrowers. In this article, we’ll explore the essentials of KYC in online lending and key considerations for a secure, efficient process.

Why Is KYC Essential for Online Lenders?

Simply put, KYC helps online lenders verify who they’re offering loans to. Loaning money is always a sensitive process, but it’s even more so when done online instead of in person. KYC is also essential for online lenders: Know Your Customer checks are a legal requirement for any organization issuing loans, and non-adherence to KYC obligations can result in prosecution.

SEON leverages digital footprints and device data to evaluate risk early, cutting costs without adding friction.

Speak with an expert

Requirements for Online Lenders?

One legal requirement for online lenders is the implementation of KYC checks, but with that requirement come many others that they must adhere to.

These KYC-related requirements typically include verifying a customer’s face, ID card and documentation. This is why online lenders should ask prospective customers to provide documents such as utility bills to confirm the customer’s address, among other details.

While the law requires online lenders to carry out KYC checks, specific requirements will depend on their jurisdiction.

For example, online lenders based in the US must follow KYC laws at the federal level, meaning that they must adhere to the Bank Secrecy Act. This dictates that they must undertake and record certain activities, such as ensuring that they complete a Suspicious Activity Report (SAR) when such a need arises.

Meanwhile, EU-based online lenders are legally required to comply with KYC rules in line with 6AMLD and GDPR. These two regulations ensure that online lenders record their KYC processes for anti-money laundering purposes and protect customers’ personal information throughout the process.

Three Risk Rules for KYC for Online Lenders

SEON’s fraud prevention streamlines the KYC process by identifying suspicious activity early, even before the KYC checks start. Here are three key risk rules that can help online lenders effectively monitor and manage KYC compliance.

#1: Disabled Cookies & Suspicious Browsing Behavior

Many users disable their browser cookies for privacy or convenience, but fraudsters may do so to avoid detection. In online lending, malicious actors might disable cookies to make their browsing behavior harder to track, fearing that leaving a digital footprint could result in failing a KYC check and being denied a loan.

SEON can flag such suspicious activity by monitoring for disabled cookies or outdated browser versions — common tactics used by fraudsters to circumvent modern security measures. Setting rules to identify this behavior helps online lenders assess risk early, assigning fraud scores to users with potentially suspicious browsing patterns.

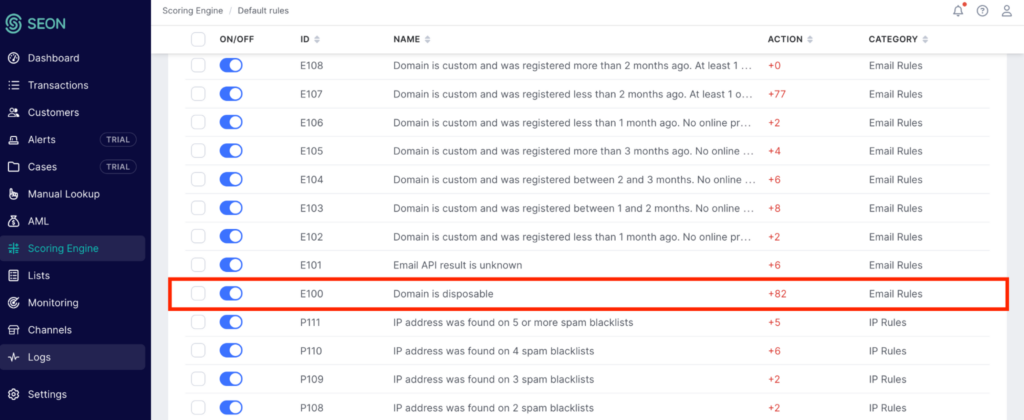

#2: Email Address Is Disposable

Using disposable email addresses is a red flag, as it often signals an intention to remain untraceable. SEON can flag disposable email addresses during the KYC process, assigning a high fraud score to these accounts. While it might seem obvious that such users could pose a risk, this simple rule allows lenders to identify suspicious entities before they even enter the KYC process. Early identification helps mitigate potential fraud risks, saving time and resources.

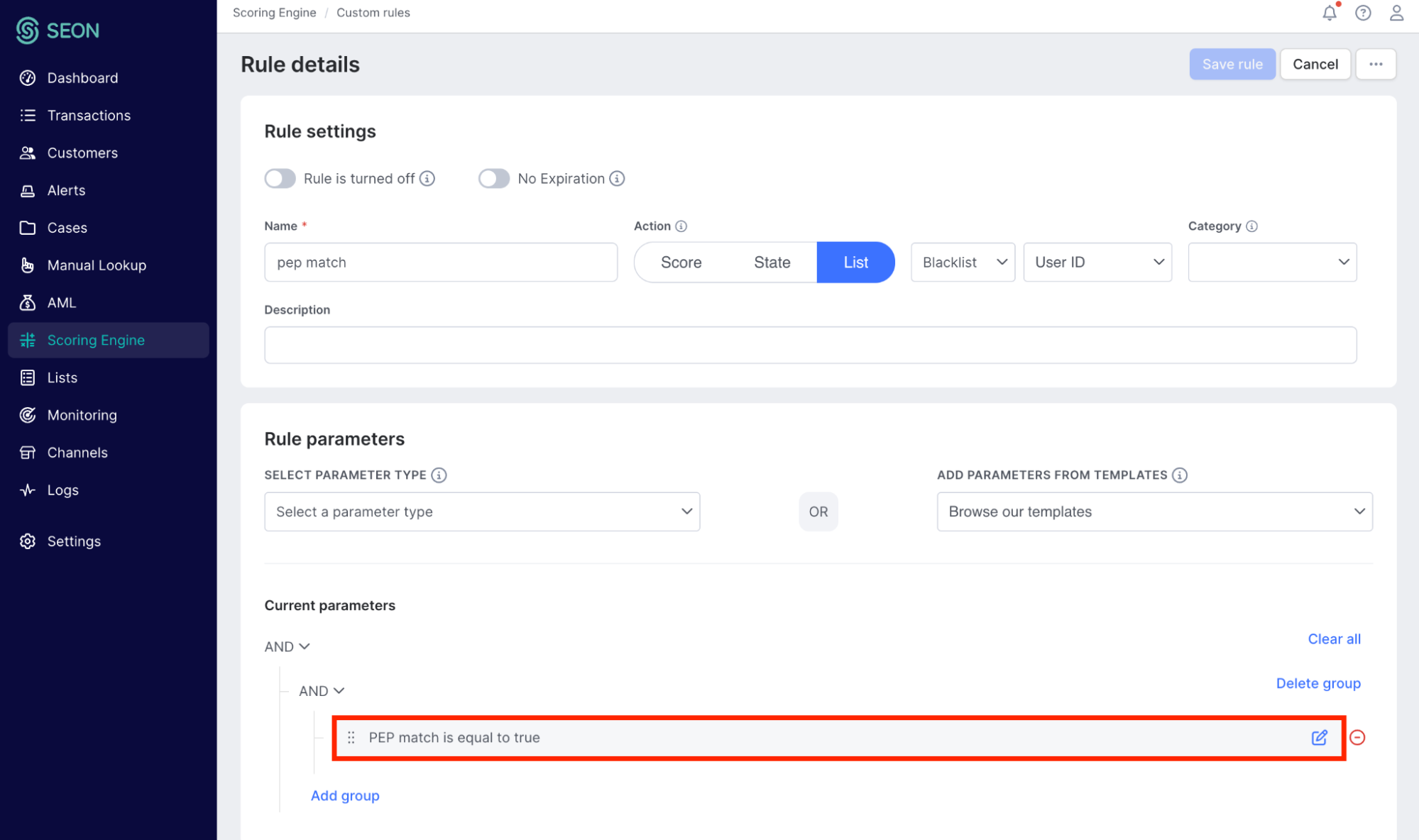

#3: User Matches a PEP Check

PEP (Politically Exposed Person) checks are crucial for identifying high-risk individuals, such as public figures who may be more susceptible to corruption or money laundering. SEON can flag users who match a PEP register, enabling lenders to review these accounts before proceeding with KYC checks. While being a PEP does not automatically indicate fraudulent intent, it provides an early warning to assess whether further background checks are needed before the onboarding stage of the KYC process. This precaution helps mitigate risks and ensures compliance with anti-money laundering regulations.

How SEON Supports Online Lenders with KYC Compliance and Beyond

SEON provides a comprehensive fraud prevention software that helps online lenders not only meet KYC compliance requirements but also optimize their fraud prevention and risk assessment strategies. By detecting suspicious behavior early, SEON enables lenders to filter out high-risk applicants before they reach the KYC stage, reducing costs, improving compliance and streamlining onboarding.

Beyond compliance, SEON’s pre-KYC checks offer additional value by supporting alternative credit scoring, helping lenders make smarter lending decisions while maintaining a frictionless user experience for legitimate applicants. With SEON, online lenders can enhance security, ensure regulatory compliance and improve operational efficiency — all in one integrated platform.

A practical look at pre-KYC screening, how it reduces false positives, and why earlier context helps compliance teams catch risk before onboarding.

Read more