Banking is one of the sectors most commonly targeted by fraudsters, criminals, and money launderers, as we saw in SEON’s Global Banking Fraud Index.

Let’s break down what counts as a banking high-risk customer, and explore how to identify them.

What Is Considered a High-Risk Customer in Banking?

Most of what makes a high-risk banking customer is dictated by regulators, specifically regarding the Bank Secrecy Act (BSA) and Anti-Money Laundering (AML). This may include:

- Politically Exposed Persons: You will find them on PEP lists. They are people who are more likely to be involved in bribery or corruption. These individuals tend to work in government and hold executive or judiciary roles.

- People in sanctioned countries: Another AML requirement is to ensure you don’t deal with customers in sanctioned countries. The lists are kept by government officials, and they can vary from one country to the next.

- Identity thieves: This is a KYC requirement to ensure that you can verify your customer’s identities. In other words, anyone who uses fake data to create an account should be considered high risk, as they are committing identity fraud.

- Money service businesses (MSBs): For banks, companies can be customers. And some companies are high-risk by virtue of their dealings with cash transactions. This makes them more vulnerable to money laundering.

Establishing strong BSA AML monitoring processes is key to identifying high risk customers early on, and avoiding costly compliance fines.

Learn how FairMoney, a Nigerian neobank, onboards more customers while reducing risk with SEON.

Read more

How Do High-Risk Customers Impact Banks?

One of the biggest challenges faced by banks when it comes to dealing with high-risk customers is compliance fines. Compliance fines may be punitive – and damaging to your bank’s reputation. Therefore, establishing strong AML in banking processes is key to managing risks and avoiding large fines.

However, there is also the issue of onboarding people who may attempt to exploit your financial institution. This may result in:

- higher chargeback rates and acquiring costs

- defaulting loan customers, which will hurt your bottom line

- account takeovers, where fraudsters take control of your existing customers’ accounts, which damages your reputation and potentially also finances

- data leaks, which also incur reputational and regulatory risk

How to Detect High-Risk Customers in Banking

When it comes to the tools that banks and financial institutions rely on to detect risk, you will find the following:

- identity verification software

- AML risk detection systems

- fraud prevention and transaction monitoring solutions

These may be built internally or outsourced to third-party vendors.

It’s also important to keep in mind how the products you select to cover these needs stack and integrate with each other. Sometimes, an end-to-end solution may be available for all of the above, but most neobanks and other types of banks are likely to deploy more than one product to ensure efficient fraud prevention, compliance and security.

Top 3 Custom Rules to Detect Banking High-Risk Customers

Here are three examples of custom rules worth implementing by financial institutions hoping to detect high-risk customers.

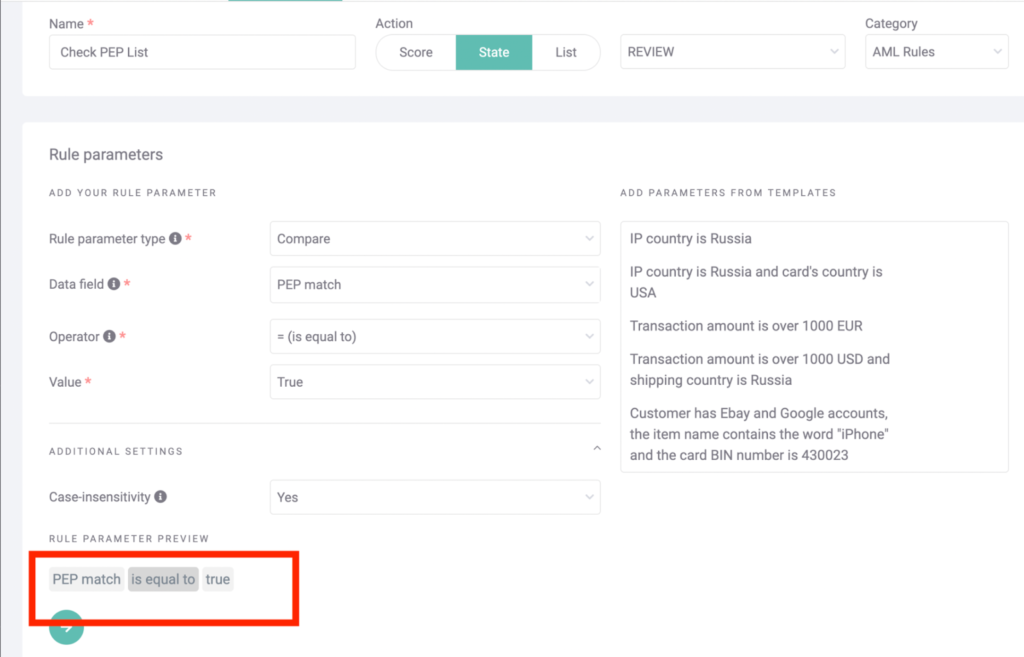

#1: Customer Appears on a PEP List

Politically Exposed Persons have to be identified to comply with AML regulations. You should therefore have an automated solution designed to check whether customers’ names appear on any of these lists.

The key is to look at the person’s full name, as well as possible spelling variations in different languages.

You should also of course ensure that the rule does not automatically block the onboarding process, as there could be false negatives due to people sharing the same name worldwide.

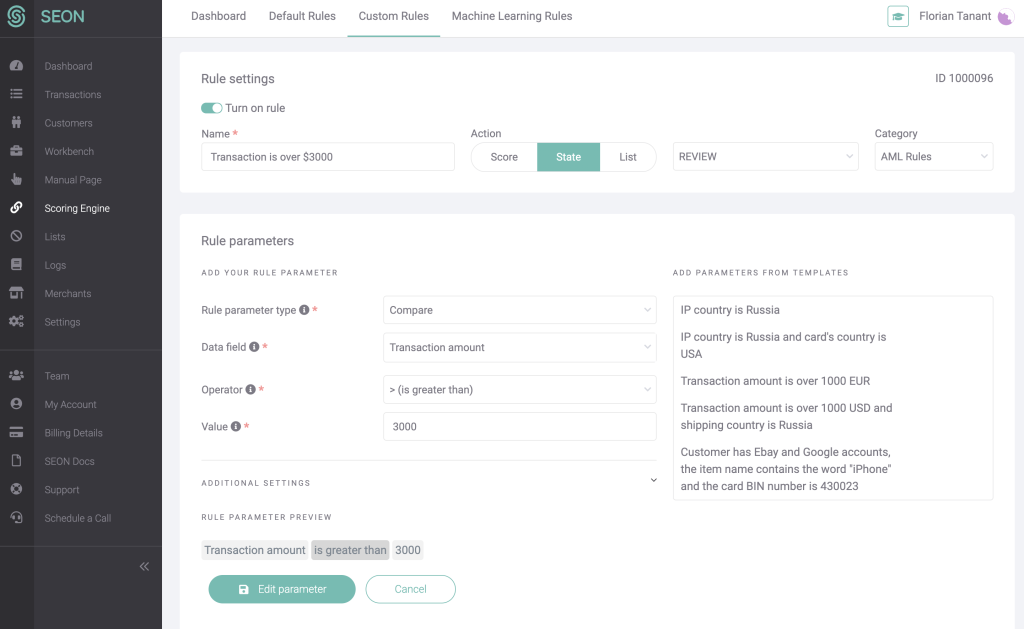

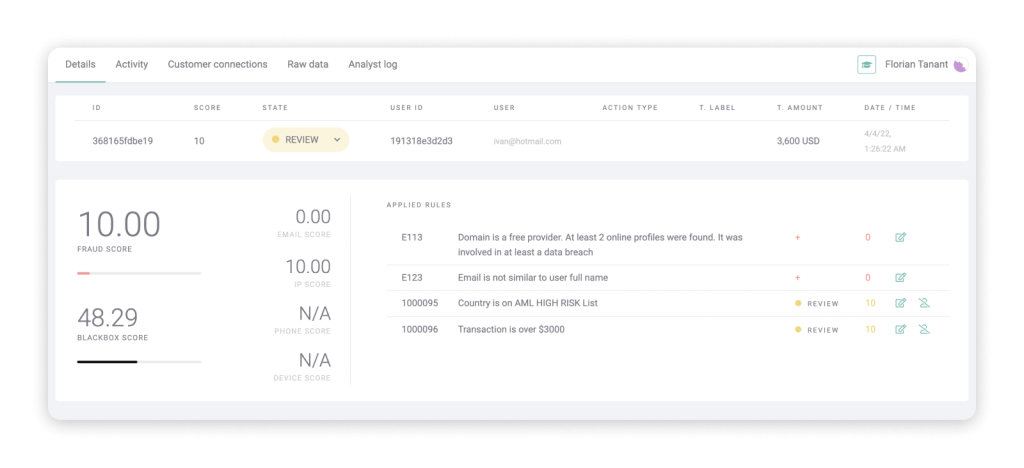

#2: Deposit Is Above the AML Threshold

Banks have to monitor the onboarding stage, but they must also remain vigilant throughout the duration of their relationship with the customer.

This is particularly evident when it comes to transaction monitoring. In fact, you should actively check and log deposits above a certain threshold to meet AML compliance requirements.

In the screenshot above, you can see that we’ve set that threshold at $3000, but also how easy it is on the SEON platform to change that to a different amount.

Below, the rule has been triggered, and all the data has been sent for review.

You should not automatically block such a transaction, of course, but having the data at hand in a manual review pile can be helpful, especially if you need to submit an SAR, short for suspicious activity report.

#3: No Social Media Profiles Found

Banks have to perform KYC checks. But what if you could save on these expensive checks by instantly filtering out obviously fake profiles using banking fraud detection software?

This is precisely what digital footprint analysis offers. It’s a unique feature to SEON and it’s particularly effective when looking at social profiles.

Why does it work? Fraudsters and criminals have to work at scale to create fake or synthetic identities, and creating a complete social profile is too time-consuming.

You can therefore flag fake profiles that have no social presence whatsoever, or at least increase the risk score for these users so that it is taken into account together with other data points to better assess how suspicious they are.

If you do this before a thorough KYC process, you will be able to remove more fraudsters, thus ensuring you don’t waste valuable KYC verification money on them.

Learn how a leading neobank automated 95% of their fraud checks and reduced their manual check times from 20 to 5 minutes

Read more

How SEON Helps Banks Identify High-Risk Users

SEON is a fraud prevention solution that includes AML checks, unique digital footprinting, strong device fingerprinting and hundreds of data points collected via various APIs.

The technology can also serve as a pre-KYC tool designed to help you understand if you can trust your customers based on their online presence.

The advantage? All the data is gathered, monitored, and leveraged for risk-scoring in one place. You get complete user activity monitoring over who is considered high-risk based on your risk appetite – as well as evolving compliance requirements.