Online marketplace fraud is any scheme in which a buyer or seller deceives a digital marketplace or its users for financial gain, using tactics like fake listings, stolen-card purchases or triangulation schemes.

Effective marketplace fraud prevention stops those schemes early, usually at account creation, before a fraudster can list, buy or cash out. The earlier the intervention, the smaller the loss.

QUICK SUMMARY:

What Is Marketplace Fraud?

Online marketplace fraud covers everything from a one-off scam between two users to organized rings exploiting a platform at scale. Because these marketplaces host strangers transacting on trust, they attract fake listings, stolen-card purchases and identity theft in volumes a single-seller store never sees.

The damage rarely stops at one transaction, because a stolen-card purchase can rebound as a chargeback weeks later. That delay is what makes prevention so much cheaper than cleanup.

Types of Marketplace Fraud

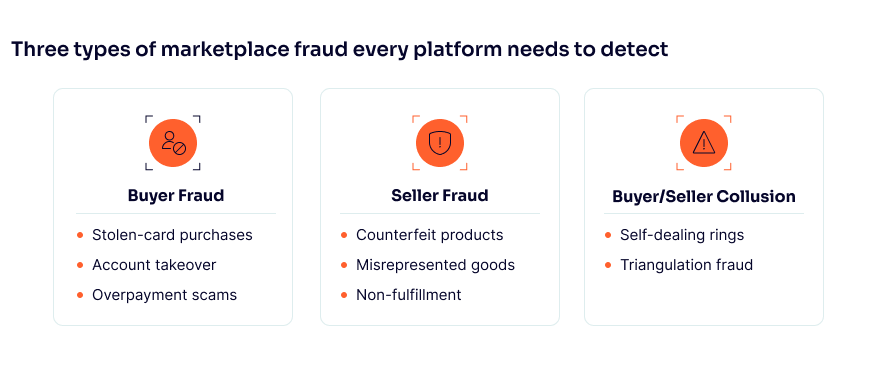

Because a marketplace runs two payment directions at once, buyers paying in and sellers cashing out, the threats group into three categories: buyer fraud, seller fraud and collusion across both.

- Buyer fraud covers stolen-card purchases at checkout, account takeover of trusted buyers and overpayment scams that trick a seller into refunding funds that never settle. Phishing for a seller’s personal data often rides alongside it.

- Seller fraud runs through the listing. Fraudsters post fake or counterfeit products, misrepresent goods or copy a legitimate seller’s profile, then collect payment for orders they never fulfill. Vetting these accounts is its own discipline, covered in our seller onboarding fraud guide.

- Buyer/seller collusion is the hardest to catch, because one ring controls accounts on both sides and trades with itself using stolen cards. In triangulation fraud, a related pattern, a fraudster fulfills a real order with a stolen card bought elsewhere.

How to Prevent Marketplace Fraud

Effective marketplace fraud prevention rests on one principle: stop bad actors at the gate rather than chase losses after a transaction settles. A blocked signup never becomes a chargeback, a dispute or a damaged reputation, so the earlier you act, the cheaper the outcome.

Verify identity at onboarding

Most abuse traces back to accounts that were too easy to open. Layered Know Your Customer (KYC) checks, from email and phone validation through to document verification for higher-risk users, filter out throwaway and synthetic identities before they transact. Sellers warrant the closest scrutiny, as our seller onboarding fraud guide explains.

Score risk in real time across both flows

Verification on its own is static, so it needs a dynamic layer. A risk-scoring engine weighs signals at signup, checkout and payout, then sorts users by risk: low passes freely, high is blocked and the uncertain middle goes to review. Buyer and seller flows need separate logic, as our payment fraud guide shows.

Cross-reference data points to expose rings

Fraudsters work at scale, which forces them to recycle data that a digital footprint analysis can surface. Two accounts sharing an email, device fingerprint, internet protocol (IP) address or payout detail are rarely a coincidence, they are usually one operator multi-accounting. Mapping those links lets a team dismantle a whole ring at once.

Monitor behavior after approval, not just at signup

Onboarding checks catch a lot, but the clearest signals often appear in the days just after approval. Sudden listing velocity, repeated pushes to move a chat off-platform or payout requests that do not fit the account’s age all flag risk that a one-time signup check would miss.

Educate users and enable reporting

Prevention is not only technical. Clear guidance on current scams, paired with a one-tap reporting tool, turns your user base into a detection network that surfaces abuse faster and feeds real examples back into your rules.

Choosing a Marketplace Fraud Prevention Tool

No single control stops every scheme, so marketplace fraud prevention ultimately depends on choosing technology built for two-sided risk. Coverage has to span both buyer checkout and seller payout, with real-time cross-account matching and rules your analysts can change without an engineering sprint.

Most tools were built for the single-merchant model and leave a structural gap on the seller side. Our guide to choosing a fraud detection tool for your marketplace breaks down the five criteria that matter and the questions to put to any vendor.

Why Marketplace Fraud Is Rising

The pressure on marketplace fraud prevention keeps climbing, and SEON’s own research shows why. Fraud is growing faster, threats are shifting earlier in the customer journey and the tools meant to catch them often look in the wrong place.

In SEON’s 2026 Fraud & AML Leaders Report, a survey of 1,010 risk and compliance leaders, the share who disagreed that fraud losses are growing faster than revenue fell by almost 40% year over year. In other words, more leaders now accept that losses are outrunning growth.

Account takeover (ATO) sits at the center of that shift. The same report names ATO as the most commonly cited threat vector, flagged by 26% of leaders, while financial accounts alone make up 32% of ATO breaches globally, a direct risk to marketplace accounts that store payment methods and balances.

Yet much of the defensive budget still lands downstream. In payments, 46% of artificial intelligence (AI) spend goes to transaction monitoring, the stage with the most data but the narrowest view of what came before it, which is exactly where marketplace fraud is seeded.

How SEON Helps Stop Marketplace Fraud

SEON lets marketplaces monitor, filter and block bad actors before they ever create an account, without adding friction for genuine users. It works from data you already collect, an email or phone number, enriched with passive signals from the device and IP address.

Powered by 900+ real-time, first-party data signals, the platform builds a digital footprint for every user and feeds it into configurable risk rules across onboarding, checkout and payout. You can auto-approve good customers, block clear fraud and route the uncertain middle to review and the same rules expose the account links that reveal a whole ring.

FAQ

How do you prevent marketplace fraud?

The most effective marketplace fraud prevention happens at onboarding, before a fraudster can list or buy. Combine layered identity checks, real-time risk scoring across buyer and seller flows, cross-account link analysis and behavior monitoring, then raise friction only for higher-risk users so genuine customers pass smoothly.

What is online marketplace fraud?

Online marketplace fraud is any scheme in which a buyer or seller deceives a digital marketplace or its users for financial gain, using tactics such as fake listings, stolen-card purchases, triangulation, overpayment scams or phishing.

Where does fraud enter a marketplace?

Fraud enters from two directions: the buyer checkout flow, where stolen cards drive purchases and chargebacks, and the seller payout flow, where fraudulent sellers cash out before disputes land. Organized rings often run linked accounts on both sides at once.

How do marketplaces stop fraudulent sellers?

Marketplaces stop fraudulent sellers by verifying identity at onboarding, analyzing the digital footprint behind each signup and monitoring payout behavior for accounts that pass checks then turn malicious. Thin or inconsistent signals at registration are the earliest warning.