How Has the Use of BNPL Increased in Recent Years?

If you’ve paid for anything online recently, there’s a good chance that you’ve seen a new option popping up on the checkout page: Buy Now Pay Later (BNPL).

The attraction of delaying all or part of your payment is understandable, allowing you to spread out the cost of your purchase and make it more manageable.

BNPL schemes essentially act as interest-free loans, which appeals to people who have no credit history and those who have never used credit cards, making them very attractive to Gen Z in particular.

However, there are a couple of potential downsides to Buy Now Pay Later.

Not only can it end up being a slippery slope that leads to you spending beyond your means, but there’s also a very real threat of falling victim to fraud, which BNPL brands can protect themselves against using fraud detection with machine learning, device fingerprinting and other tools.

The growth of this sector has presented its own risks. As it is essentially acting as a wallet for a lot of customers, it has been identified as an attack vector thus attracting criminals and introducing buy now pay later fraud events.

We’ve taken a look at how BNPL schemes have taken off in the last couple of years, as well as found out who is most likely to use them.

How Has the Use of BNPL Increased?

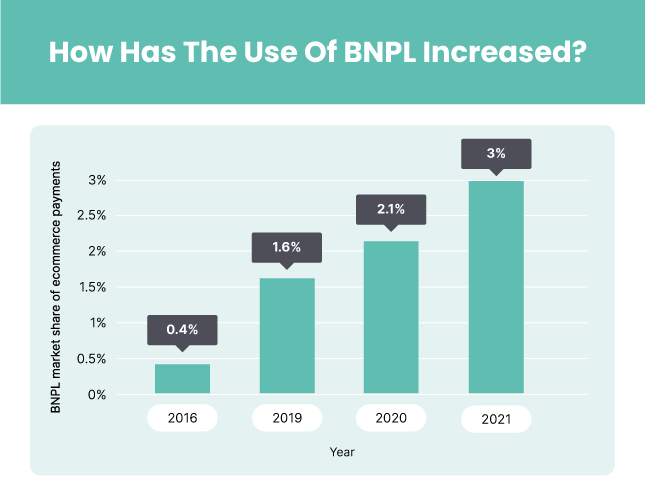

The boom in BNPL services is clear to anyone who shops online, but just how much have these schemes increased recently?

Globally, BNPL schemes accounted for just 0.4% of ecommerce payments in 2016 but by 2019 had quadrupled to 1.6% and by 2020 stood at 2.1%.

The UK’s biggest BNPL provider, Klarna, has seen its customer base double in the space of under two years, jumping to 15 million as of November 2021.

Which Countries Use BNPL the Most?

The country where BNPL has achieved the greatest popularity so far is Sweden, where it accounts for a quarter of all ecommerce payments (25%).

Like in the rest of the world, the BNPL market here has grown rapidly, by almost double since 2016 – although it’s interesting to note that the market share of BNPL actually dipped slightly in 2020, potentially as a result of the coronavirus pandemic.

Klarna was founded in Sweden, which could go some way to explaining just why these types of services are so popular in the country, which has also seen a sharp increase in its ecommerce market in general.

Fellow European nations Germany and Norway also have a strong appetite for BNPL, with Germany also being the locale that saw the greatest increase in interest between 2016 and 2021, growing from just 3% to 20%.

Who Is Most Likely to Use BNPL?

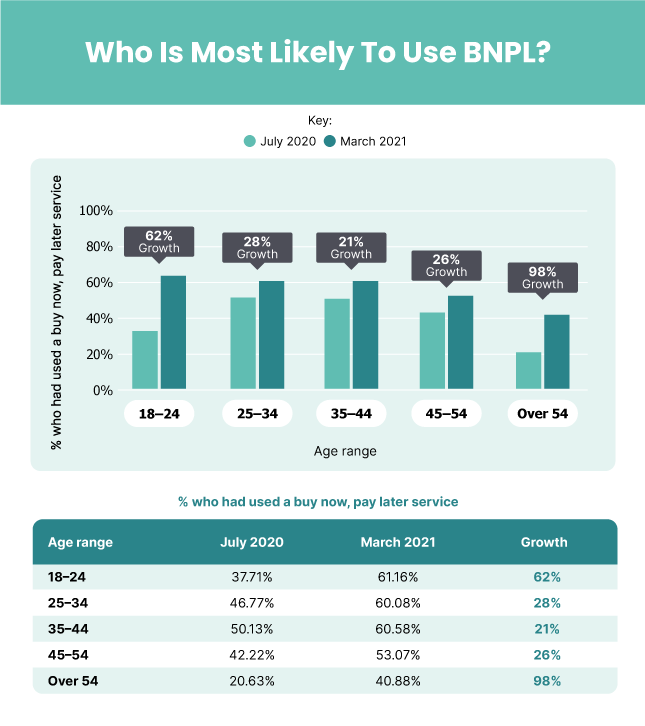

BNPL has been dubbed the future of millennial finance, but is it just the younger generation that is making the most of these schemes?

Looking at data for the United States, the picture is actually a bit more varied than you might think.

While it’s true that BNPL is most popular among Gen Z, with 61.16% of people ages 18–24 saying they have used such a service, those aged 25–34 (60.08%) and 35–44 (60.58%) weren’t far behind at all.

And while it’s the Baby Boomers who make use of BNPL the least, at 40.88%, it’s very interesting to note that usage among over 54s has increased substantially, growing by just under double between July 2020 and March 2021.

When it comes to gender, it appears that BNPL schemes are more popular with men, although only slightly, with 62.2% of men saying they had used BNPL compared to 51.36% of women (again, in the US).

And men were much more likely to be regular users of the schemes too, with 12.16% saying they use them more than once a week, almost twice as many as was the case for women (6.11%).

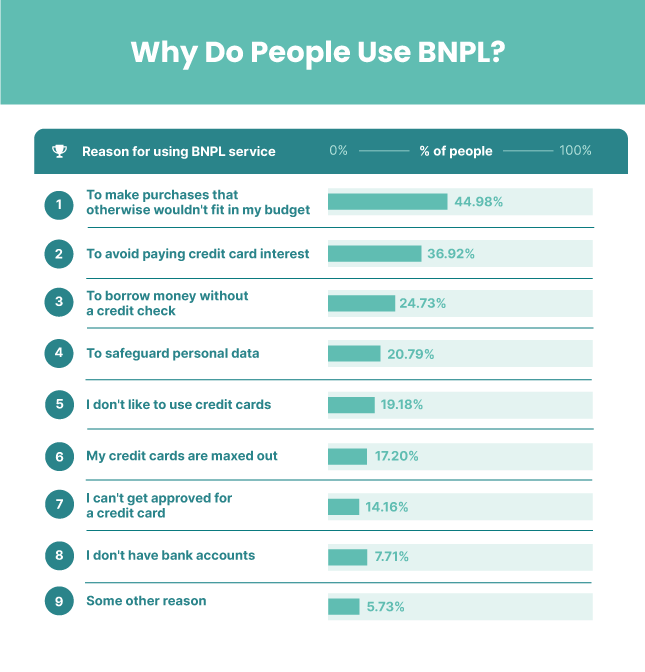

Why Do People Use BNPL?

So, we can see that interest in BNPL schemes is booming. But with the risk of fraud and the fact that they can potentially lead to unhealthy spending habits, why are so many people making use of them?

In the US, the most common reason that people use BNPL is to make purchases that otherwise wouldn’t fit into their budgets, with around 45% of people citing this as their main reason for doing so.

While the flexibility that BNPL offers can be handy, the fact that so many shoppers admit to using the schemes to pay for things beyond their means highlights how dangerous they can be.

Some of the other popular reasons for using BNPL include avoiding paying credit card interest (36.92%) and borrowing money without having to go through a credit check (24.73%).

Following the financial crisis of 2007–08, many individuals became very averse to taking out credit and loans, which is why the interest-free nature of BNPL appeals to so many and why adding BNPL options can be so lucrative for ecommerce retailers.

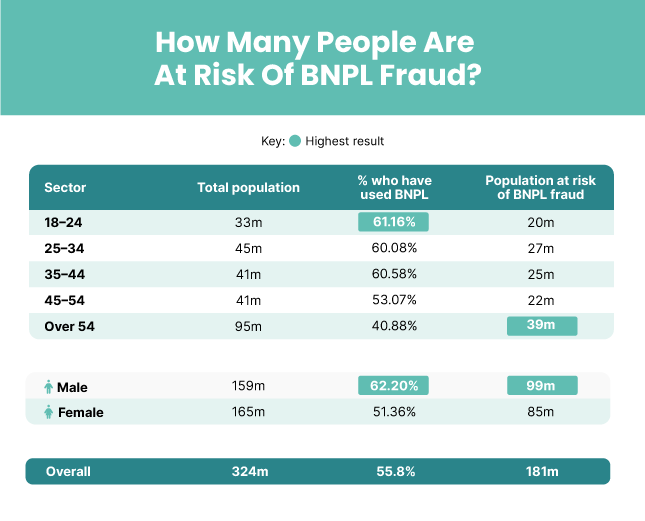

How Many People Are at Risk of BNPL Fraud?

BNPL companies are competing to become the default consumer wallet and will often offer to take the risk of chargebacks to convince more retailers to sign up.

However, this means that consumers’ BNPL accounts are becoming lucrative fraud targets, with fraudsters using BNPL to steal people’s identities and slip past fraud defenses in a “trojan horse” attack, a term coined by Karisse Hendrick, Principal of Chargelytics Consulting.

Taking all of the above into consideration, just how many people are potentially putting themselves at risk of becoming victims of BNPL fraud?

Looking at the US, over half (55.8%) of Americans say that they have used a BNPL scheme.

With the total population currently standing at around 324 million people in the country, this means that as many as 181 million people could potentially be exposed to fraudulent activity.

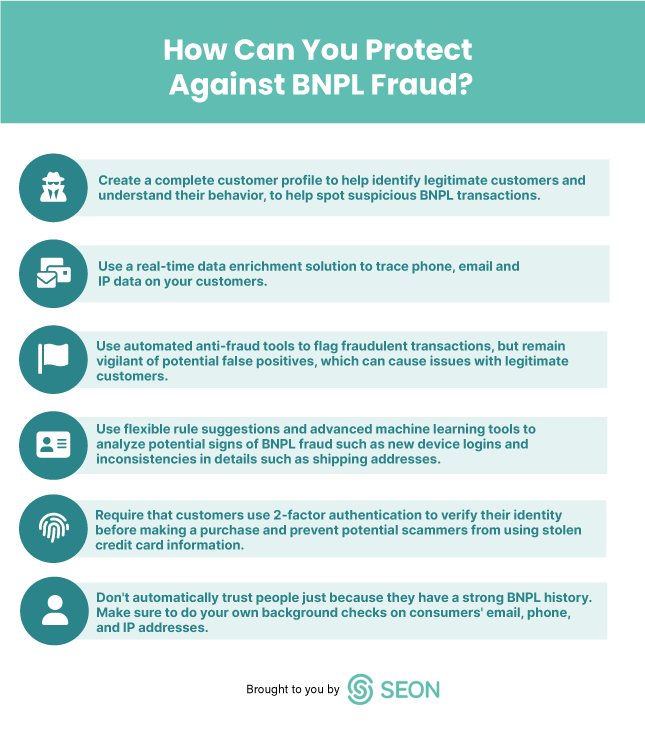

How Can You Protect Against BNPL Fraud?

Unfortunately, BNPL fraud is a very real threat, for consumers and merchants alike – as well as for BNPL companies, which can have even more to lose.

For merchants, there are a couple of ways in which fraudsters can strike, such as identity theft and account takeover attacks.

And while the BNPL provider itself should be held liable if anything goes wrong, your reputation as a retailer can still take a considerable hit, and if the customer files a chargeback complaint you can end up losing your inventory without payment, even if you’re not liable.

So, how can you go about protecting yourself against BNPL fraud?

Sources

- Information on the usage of BNPL schemes around the world was sourced from Statista.

- Information on the number of people using BNPL schemes in the US and breakdowns by age, gender and motivation were sourced from a study by The Ascent.

- To estimate the wallet share of BNPL users, we calculated the percentage of people who have used BNPL as a percentage of the total population of the United States, according to the United States Census Bureau’s Age and Sex Tables.