After a decade of buying “just one more tool,” fintech companies are confronting an uncomfortable truth: fragmented stacks, not fraudsters, may now be their most serious vulnerability. Years of layering specialist applications for Know Your Customer (KYC), Anti-Money Laundering (AML), fraud prevention and detection, case management and reporting have left many organizations running architectures that are expensive to maintain, slow to adapt and nearly impossible to govern end-to-end.

Compounding the issue, global fintech funding is down 12%, from $120 billion to $105 billion, indicating that capital is rotating decisively toward scalable, AI-native platforms with credible paths to profitability, and away from the narrow point solutions that defined the previous era.

Colliding with mounting regulatory pressure and deep tech-stack fatigue, the industry’s long-deferred vendor reckoning is finally here, and with it, choices that will determine which providers endure, which get absorbed into broader platforms and how operators will create the strong foundations risk and compliance infrastructure needs.

A Decade of Accumulation in Fintech Stacks

The hyper-specialization wave that swept fintech in the early 2020s left a complicated legacy. Every new risk category or regulatory demand seemed to justify its own dedicated tool, each sold as best-of-breed, each promising painless integration. The cumulative effect was something far messier: integration debt, deepening data silos and a total cost of ownership that crept steadily beyond what anyone had budgeted for.

Now the bill is due. With less than half of the world’s top 70 fintechs achieving profitability, standalone niche tools face an equation that no longer works. It’s a catch-22; they cannot grow without capital, and they cannot raise capital without profits. Consolidation pressure has become a permanent feature of the market, and the most fragmented architectures are already its most visible casualties.

The Forces Driving Fintech Vendor Consolidation

The buyer motion across enterprise fintech has fundamentally shifted. Organizations are no longer running quiet pilots in departmental silos and worrying about integration and governance later. Recent CIO and IT leadership research shows a clear pivot toward consolidation, as more organizations streamline overlapping tools and commit to a smaller set of core providers.

Centralized vendor management, rigorous security reviews and compliance gating now sit at the front of most buying processes, raising the bar for any new tool entering a stack and accelerating the exit of tools that cannot clear it. The operating logic has moved from test-and-expand to audit, consolidate and commit.

Regulatory expectations are further amplifying the pressure. Supervisors are raising the bar on AI explainability, AML typology coverage and cross‑border fraud surveillance, and they are asking firms to demonstrate precisely how decisions were made and which policies governed each step. As more institutions deploy AI and real‑time monitoring in their risk programs, regulators expect transparent, auditable models and integrated controls across jurisdictions, not opaque engines bolted onto the edge of the journey.

This level of accountability is nearly impossible to provide when risk signals and enforcement actions are scattered across siloed tools with no shared context. Platform consolidation has consequently shifted from a cost‑cutting initiative to a compliance and governance program, a way to close gaps before auditors and supervisors surface them in reviews or enforcement actions.

What Consolidation Looks Like in Practice

Consolidation in 2026 shows up directly in how vendors position themselves. The players winning deals are expanding laterally by adding adjacent modules, pulling former point solutions into their orbit and positioning themselves as the control plane across multiple workflows. Instead of solving a single slice of onboarding or transaction monitoring, they offer connected coverage across the journey, using shared data, policy engines and reporting to keep everything in sync.

The 5.15‑billion‑dollar acquisition of Brex by Capital One illustrates this shift: a major bank chose to buy an AI-native platform already spanning cards, spend and workflows rather than assembling those capabilities tool by tool. Vertical SaaS M&A follows the same logic, with investors favoring suite‑level platforms that can cross‑sell into adjacent workflows over niche products with uncertain paths to scale.

The bar for surviving renewal season has never been higher, and buyers are now applying a four‑part test. First, proof: measurable outcomes tied to live deployments, not roadmap promises. Second, compliance by design: built‑in audit trails, explainable decisions and controls that satisfy regulators without a separate integration. Third, total cost of ownership: licensing, integration, maintenance and headcount. Fourth, time‑to‑value: deployment in weeks, supported by prebuilt connectors and repeatable playbooks.

Tools that cannot win on all four dimensions may survive a pilot, but their odds of clearing the next renewal cycle are shortening fast.

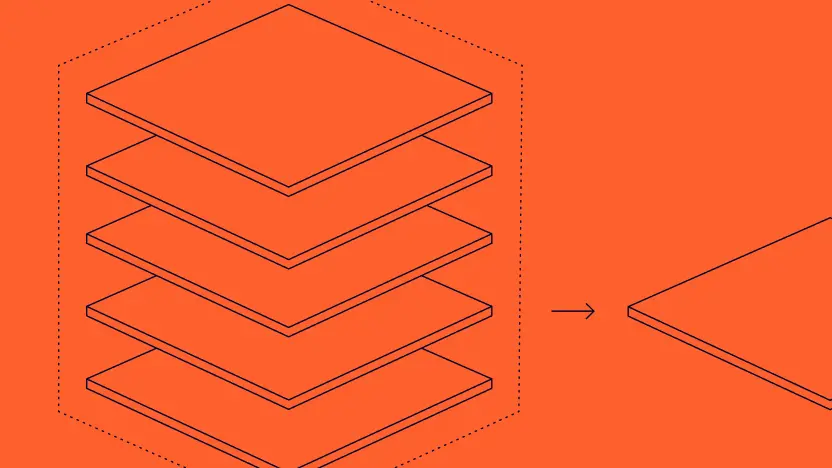

Platform First, Point Solutions Only When Indispensable

By the end of 2026, the default fintech buying motion will be platform‑first. Buyers will look for partners that sit on top of meaningful data, connect multiple critical workflows under a single governance layer and still make economic sense in a tighter capital environment.

Point solutions will not disappear entirely, but the test they must pass has become unforgiving. If a specialist tool doesn’t offer something clearly indispensable, it will be bundled into a broader suite, sunsetted or quietly swapped out at renewal. For fintech operators, that makes the 2026 vendor review less about shaving line items and more about closing risk gaps. A disconnected stack drains budget and blurs where risk truly moves through the business, and blind spots have a habit of emerging at the worst possible moment, whether in the middle of an incident or under direct regulatory scrutiny. The reckoning, long deferred, is here.

Consolidating tools or rethinking fraud and compliance? Talk to SEON’s experts to see how you can cut complexity, keep coverage and move faster with a smarter, unified stack.

Speak with an Expert