What Are False Declines?

False declines are legitimate transactions that get blocked due to suspicions of fraud. They are closely link to the concept of customer insult rate because they frustrate or “insult” good customers by not letting them complete their purchase.

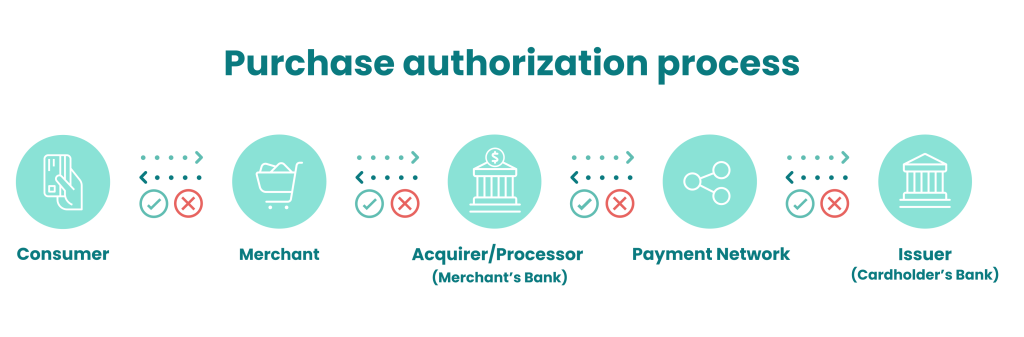

In a false decline, the eshop, payment processor or card issuer is falsely identifying a payment as fraudulent, and thus declining it. This happens at checkout and takes the customer by surprise.

In essence, a false decline accuses a customer of being a criminal, and can even cause them to worry that there is something wrong with their card, or that they will not be able to complete this and/or other transactions with it at all.

By definition, a false decline is always a mistake, because the fact it is “false” means it should not have happened, and the buyer is not a fraudster.

How Common Are False Declines?

False declines are fairly common in ecommerce. A survey published by the Merchant Risk Council found that the average online store has a 2.6% rate of false declines because of suspected fraud. This means that 2.6% of the transactions blocked by the average eshop’s overzealous threat detection tools were, in actual reality, legitimate shoppers trying to make legitimate purchases – and being stopped from doing so.

Another important point to make is that the more expensive the attempted purchase, the more likely the transaction is to be declined. So, for purchases over USD 100, the false decline rate jumps to 3.1% – and so on for even more expensive buys.

Although false declines can, in theory, happen in any type of setting, the vast majority take place in card not present (CNP) transactions, and particularly online.

The online setting also increases the likelihood of customers getting frustrated, as there is no representative nearby to help them through, like there would be in a physical store. On the contrary, a customer at an eshop will have to initiate contact with customer service themselves, if needed.

Are False Declines the Same as False Positives?

False declines are a type of false positive, and specifically one that means an attempted card payment has been declined. All false declines are false positives. However, not all false positives are false declines.

False declines always have to do with payment approvals – usually of credit card payments but also of debit cards, gift cards, as well as digital wallets and payment apps.

If the card purchase authorization is blocked at the approval stage, this is a false decline. If a legitimate buyer is stopped from proceeding at another stage of their customer journey, for instance when attempting to create a new account, that is a false positive, but not a false decline.

Cut through alert fatigue with smarter rules, real-time data, and fewer unnecessary escalations.

Read the how to guide

What Causes False Declines?

False declines are often caused by rigid fraud management software. Fraud fighting platforms set and follow fraud score risk rules, but when these are too stringent or badly calibrated, several legitimate transactions are also blocked. This, in short, is because the software thinks the buyer might be a criminal who is using a stolen card.

Some risk management tools also block medium-risk transactions, when in actual fact these are best manually reviewed.

Common causes of false declines include, among others:

- filters for the location of the shopper

- delivery address not matching the card’s billing address

- shipping speed inconsistencies

- inconsistent order data

- larger than average orders

- multiple shipping addresses

Why Are False Declines Damaging?

The biggest reason is financial. A false decline means that a legitimate customer has been stopped from buying one or more of your products.

From there, they might shop at your competitors, or try your shop again, but they are still likely to feel disappointed with your company. This damages your reputation and can even overwhelm your customer support.

More specifically, false declines can have disastrous consequences for an ecommerce business. In particular, by blocking legitimate customers from finishing their purchase, you:

- Lose sales, which directly impacts your revenue. The sale the customer was attempting has been lost although it was legitimate, and the customer must choose to invest additional time and effort to try again if they still want to buy from you – which is not a given.

- Lose a customer: Blocked payments frustrate and “insult” customers, who are likely to go looking for the same item or products on competitor websites. Even if they don’t do so right away, the false decline can leave a bad impression and discourage them from returning.

- Damage your business reputation: In a world where customers expect online services to work seamlessly and with as little friction as possible, creating obstacles is the surest way to get into users’ bad books. In extreme cases of repetitive false declines, a shopper might even speak ill of you to their friends and family, or even spread the word on social media, which can be catastrophic for an online business.

- Overwhelm the customer support team: It’s often the customer service staff who have to deal with angry customers when they should be helping people with more pressing issues. Consistently high rates of false declines might even lead to a need for additional hires for customer support.

What Is the Customer Insult Rate?

By “customer insult rate” we refer to the rate at which false declines are preventing your legitimate customers from completing their purchase.

Expressed as a percentage, this is an increasingly popular alternative term for false declines, which hits the point home of just how detrimental false declines can be for an online store and just how much they affect customer perceptions of your brand.

5 Ways to Avoid False Declines

The best methods to avoid false declines include improving your anti-fraud protocols and software, optimizing the manual review process, and ensuring you are using the settings and tools that make the most sense for your business and your customers.

More specifically:

- Check your fraud prevention tools: It could be a risk rule that is too general, such as when the IP address doesn’t point to the same location as the shipping address. If a customer is traveling, there are high chances they could be flagged as fraudster – which is a common example of a false decline.

- Test risk rules on your historic fraud analytics data: Balancing risk rules can be a trial-and-error process, so it’s important to check the new configuration with a control set. Use your historic data to verify if the new risk rules actually reduce false declines.

- Improve your manual review process: Medium-risk transactions would ideally be sent for manual review. With the right tools, you should be able to make an informed decision about whether the transaction is fraudulent or not.

- Leverage machine learning: Fraud detection with machine learning can suggest optimal rules after running over previous data where the false declines have been marked as such. Your system may deliver new rule suggestions that reduce the false decline rates.

- Beware of chargeback guarantee tools: Chargeback guarantee tools have a strong incentive to err on the side of caution. This means that they might flag a medium-risk transaction as high-risk, simply to avoid paying the chargeback fees. This works to the tool vendor’s advantage but increases your rate of false declines – and your unhappy customers.

Overall, an advanced, fine-tuned anti-fraud solution will help you keep your false decline rates as low as possible, thus reducing friction and disappointment while keeping your business safe from online payment fraud.

Sources

Merchant Risk Council: MRC Global Fraud Survey