In May 2022, UKGC CEO Andrew Rhodes emphasized the importance of changing how the industry approaches affordability. Since then, the Gambling Commission has introduced new measures to better protect vulnerable players.

Affordability remains a hot topic, with responsibility increasingly shifting from the consumer to the operator. Key areas of focus in this discussion include:

- How much customers spend

- Spending patterns

- Time spent gambling

- Behavioral indicators

- Customer-initiated contact

- Use of gambling management tools

- Account activity indicators

What Does Player Affordability Mean in iGaming?

For iGaming operators, player affordability is the idea of understanding what a customer can and cannot afford when looking at their gambling habits and uncovering any potential harms.

The National Strategic Assessment 2020 describes customer affordability as:

“Individuals spending more than they can afford to lose is one of the harms most associated with gambling. Harm can be signifcant even at low spending levels as the level of spend at which harms begin to occur depends on the consumer’s discretionary income.”

Operators face constant regulatory pressure to identify at-risk customers, but relying solely on static measures like deposit or loss thresholds can have serious consequences. The issue of affordability remains complex, as many individuals attempt to hide or deny problematic gambling behaviors.

What Is Customer Due Diligence in iGaming?

Customer due diligence (CDD) is the process of verifying and understanding the legitimacy and background of potential customers. In iGaming, CDD requirements are typically set by licensing authorities or local regulations, though some operators may go further to gain deeper insights.

The goal is to identify potential risks tied to a customer, using methods such as:

- Liveness or video checks

- Document verification

- Digital footprint analysis

- Screening against sanctions lists

- Reviewing public and private data

These measures help protect businesses from regulatory penalties and guard against issues like identity fraud, impersonation, and money laundering. It’s crucial for companies to securely collect and store personally identifiable information (PII) and remain compliant with regulations if this data needs to be shared.

How Does CDD Tie In With Player Affordability?

Player affordability and customer due diligence (CDD) are closely tied to the concept of Know Your Customer (KYC). In industries like iGaming, with multiple customer interactions, KYC is an ongoing process rather than a one-time requirement. Operators must assess high-value customers thoroughly and ensure players are not spending beyond their means.

Changes in spending patterns, increased betting frequency, or large one-off bets can create significant uncertainty and risk for operators. While source of funds checks are a key part of affordability measures, implementing them too early can disrupt the user experience, leading to churn as players seek less intrusive platforms. To balance this, automated affordability checks and continuous analysis of gameplay and deposits can effectively mitigate risks without adding unnecessary friction.

iGaming and Affordability: What the Experts Say

According to AGA, the sector generated $4.99 billion in April 2022 in the US alone, up by 12.4% compared to the same time last year. Given the boom of iGaming across the globe, it could be argued that affordability checks should be set and implemented industry-wide.

Solution providers will need to support operators in this shift in mentality as player protection becomes a more important topic of discussion.

We reached out to three industry figures to ask two key questions about player safety, risk management, and the growing importance of identifying problem gambling.

Christina Thakor-Rankin, Principal Consultant at 1710 Gaming

Christina has almost 30 years of experience working in the betting and gaming industry across all aspects of gaming operations, including compliance and MLRO.

She’s held senior roles at some of the biggest brands in the world and continues to work with multiple leading operators to help establish and fine-tune operational strategies.

Tom Webster, Head of Risk and Player Safety at Mobile Incorporated Limited

Tom is an iGaming compliance professional with a variety of experience within the industry. He worked his way through the ranks from compliance assistant to head of risk and player safety within two years.

Accomplished in both the UK and international markets, Tom’s areas of expertise include social responsibility, player protection, and AML/CFT investigations and processes.

Josie Preston, Group MLRO/Nominated Officer at Aspers Casino Group

Josie is a vastly experienced and passionate Casino & iGaming AML professional with time spent at some of the biggest online and offline casinos including the Rank Group, the Ritz Club and Ritz Club Online, Caesars Entertainment, and the Aspers Group.

She is also a Mentor and Key Content Advisor for global fincrime organization ACAMS, and plays an active role in the improvement of AML, CTF and AFC knowledge and expertise across the iGaming industry.

What is the most vital component when balancing player safety, revenue, and risk?

Christina Thakor-Rankin

For me, the most vital component when balancing player safety, revenue, and risk all comes down to good customer profiling.

Not just basic KYC but proper customer due diligence in all its forms based on as much information as possible that allows you to start to build a picture and understand as early as possible the customer’s personal and financial circumstances and their motivations for gambling.

Once you have this you can see fairly quickly where their money comes from, how much they can afford to lose (based on discretionary rather than disposable income), how their gambling fits into other aspects of their life, and if gambling is simply just a leisure activity or something else by looking at their play activity – how, when and why.

This also allows you to establish a baseline for what “normal” looks like for them, making it easier to spot when activity changes.

Also, we should be thinking about ongoing due diligence and regular spot checks throughout the lifetime of the relationship, not just when their activity changes or deviates from their normal behavior.

Tom Webster

Blanket policies and thresholds for managing player safety and regulatory risk are fast becoming outdated and are heavily restrictive on revenue.

A risk-based approach means early and comprehensive customer profiling; CDD, EDD, safer gambling, and affordability. Some key questions to consider are:

- Who is this customer?

- What do we know about them?

- Are there any safer gambling concerns?

- Where does their money come from and how much of it can they safely afford to lose?

- What are the risks to this customer’s safety?

- What are the risks to us as an operator?

Building a customer profile and answering these questions early in a customer’s lifetime, in turn, leads to the creation of a risk profile.

Once you understand who your customer is and what are the risks associated with them, this enables you to almost micromanage your customer base. You are able to differentiate between the high-risk players, the lower-risk players, and all the players in between.

At this point, managing player safety and risk becomes an ongoing monitoring job and revenue is able to grow.

Josie Preston

A robust risk assessment methodology, encompassing all risks specific to the size, nature, and complexity of business operations, is essential to the development of policies, procedures, systems, and a risk control framework in line with a risk-based approach.

However, to inform risk controls, and balance regulatory and compliance obligations with commercial imperative, the critical underlying component of a risk framework is a comprehensive risk appetite or risk tolerance statement issued by the board.

Having a clear risk appetite statement sets the tone for the operator’s approach to driving revenue, within the parameters of their legal obligations and commitment to the regulatory licensing objectives of conducting themselves in a fair and open way, protecting players from harm, and keeping gambling free from crime.

A clearly communicated risk appetite and embedded compliance culture allows the business to adjust risk controls to increase revenue, whilst remaining within the limitations of the degree of risk the operator is willing to tolerate.

Webinar: Affordability in Focus

This SEON webinar dives into the affordability options available for operators, in collaboration with W2, William Hill, and Wiggins.

What types of tools are effective to help manage player risk and affordability?

Christina Thakor-Rankin

Social media can be helpful in seeing if someone’s situation has changed or if their motivation for gambling has changed – e.g. have they suffered a bereavement, are they engaging with a new crowd that is influencing their gambling, etc.

Checks should also be considered where a customer’s stakes start to decrease too. It could mean that there has been a change in their circumstances. For example, loss of job, increase in living expenses compared and the customer profile adjusted based on refreshed due diligence.

In the end, this is just humans trying to understand other humans.

You can have the best tools and solutions in the market but if they haven’t been configured based on your particular business model and customer demographic, or your analysts don’t know how to use them or analyze the data generated from them, then the tools are not going to be half as effective as you think.

Of course, some tools are better than others. There has been a lot of noise about affordability tools that use government data based on geolocation and average salary.

Anyone who lives in London or any other big city will tell you that you can have social housing and lower-income groups happily cohabiting with million-pound houses and high earners in the same street, and open banking is a great step in the right direction but requires customer consent.

The best tools allow you to pull together data from a multitude of sources, map it against a set of sensible rules (financial and behavioral triggers) that reflect your business and product portfolio in an easy-to-use format, and automatically include it in the risk score assigned to the customer.

Tom Webster

Effectively managing player safety and regulatory risk will become more and more of a powerful commercial tool.

Player acquisition through reputation, player retention, and better player experiences are just some of the ways I can see good compliance driving revenue.

There are many useful and effective tools on the market at the moment such as:

- safer gambling reporting (behavioral and financial triggers)

- open-source data

- credit reporting services

- open banking

That’s just to name a few. However, I don’t think that any of them alone offer the complete solution.

It’s necessary to use a combination of all these to effectively build a customer profile and identify and manage safer gambling. Of course, well-trained and skilled analysts are ultimately needed to pull this all together.

Josie Preston

Risk-sensitive, technology-enabled solutions for real-time transaction monitoring and alert systems are certainly one of the most effective tools for proactively detecting patterns of spend and duration of play indicative of potential gambling harm.

However, operators should conduct modeling upon the customer demographic in order to adopt a pragmatic approach to the sensitivity of such controls, ensuring the monitoring processes accurately capture potential problematic gambling behavior whilst equally ensuring that monitoring and alert outcomes requiring action or intervention are operationally manageable to execute.

Detection of potential problem gambling behavior is heavily reliant on the manual observation skills of operational employees to identify potentially problematic gambling behavior and markers of harm.

Apply training and experience to initiate interactions and evaluate the impact of those interventions on a customer’s subsequent behavior in accordance with the Gambling Commission’s Safer Gambling guidance.

Although a lack of automated solutions may be perceived as a disadvantage in the identification of gambling harm in the non-remote sector, the value of face-to-face detection and intervention with a customer displaying signs of problem gambling cannot be underestimated.

The level of support, guidance and attention provided by human contact to manage the relationship with a customer expressing gambling difficulties is not an aspect of harm prevention that can be achieved with technology.

Webinar: iGaming Risk Management

Watch below our iGaming Risk Management webinar with industry fraud expert Ozric Vondervelden, Co-Founder at Greco.

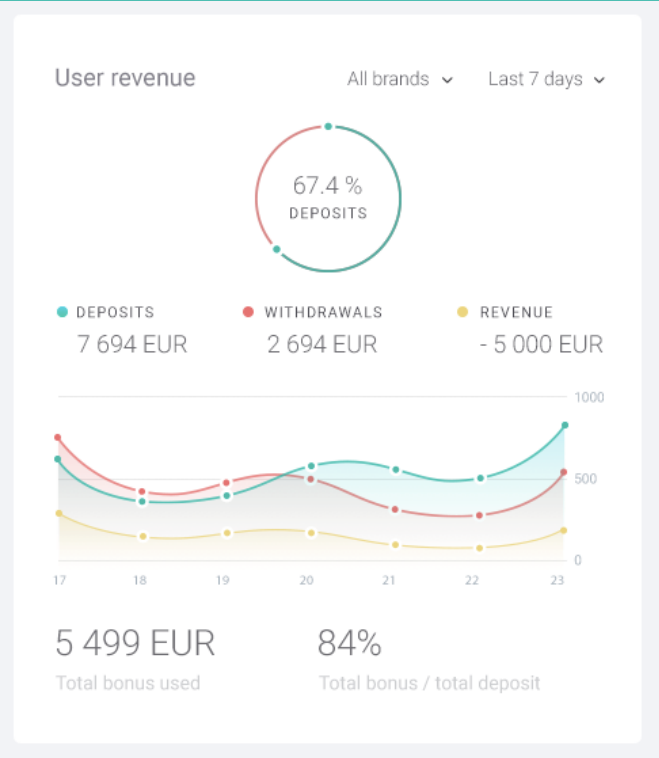

How Can SEON Support iGaming Affordability Checks?

SEON has introduced solutions such as our revenue widget, which lets you see a snapshot of any given user’s deposit and withdrawal levels within a certain period, to better enable the human touch that Josie highlights above.

While this is typically used to spot bonus abuse, some risk managers in the space use this tool for extra due diligence on potential gambling harm as it enables you to see a customer and their financial interactions from a single viewpoint.

A strong, flexible fraud prevention platform should allow you to create custom rules to highlight risky behaviors in real-time to help with affordability analysis including customer spend rate, time-to-bet speed, and unusual or larger spending amounts.

Furthermore, our digital lookup tools enable compliance and risk managers to uncover more about their customers via their online and social media presence.

Examples include:

- Through data enrichment using our OSINT tool, you can easily find someone’s LinkedIn profile with just their email address and view any potential job changes.

- See their digital footprint history (300+ digital and social checks) at a glance, giving you a more complete picture when assessing affordability by considering data points such as e.g. their Airbnb stay history, if they’ve made it public.

- You can pull assumptions and support cases from certain scenarios such as if a person is paying for multiple streaming service subscriptions or is present on more niche, higher cost-based platforms such as GitHub.

Partner with SEON to reduce fraud rates in your business with real time data enrichment that only lets good users through to KYC and CDD.

Ask an Expert

Sources

- iGaming Business: Gambling Commission CEO Rhodes calls for new mindset on affordability

- UK Gambling Commission: National Strategic Assessment 2020