Fintechs and digital banks benefit greatly from open banking APIs, which enable faster onboarding, more personalized offers and scalable growth. However, every new connection in the open banking ecosystem also introduces fresh opportunities for fraudsters to exploit gaps in KYC, AML and ongoing registration monitoring.

By understanding how open banking fraud works and how to combine real‑time data, device intelligence and AI-assisted investigations, fraud and risk teams can protect growth while keeping regulators and customers on their side.

Key Takeaways

- Open banking expands access to financial services but also widens the attack surface, from account takeover to synthetic identities created at registration.

- Weak or one‑off KYC checks are no longer enough; continuous registration and lifecycle monitoring are essential to stop bad actors before they transact at scale.

- Fraud teams can safely leverage AI for faster investigations and better decision support, as long as they sit on top of clean, well‑structured risk data.

- SEON helps fintechs and digital banks reduce open banking fraud by enriching identities at sign‑up, monitoring risky patterns in real time and feeding accurate signals into both rules and AI models.

What Are the Uses of Open Banking?

Open banking is designed to create a secure bridge between people’s financial data and third‑party services, breaking the historic monopoly banks held over customer information. It allows licensed fintechs, digital banks and other regulated providers to access account data via APIs, with the customer’s consent, to deliver more tailored and transparent financial products.

In Europe, open banking started with PSD2 but is now evolving towards PSD3, a new Payment Services Regulation, and the wider Financial Data Access (FiDA) framework, which will extend data sharing beyond payments into areas such as savings, investments, pensions, and insurance. The UK remains one of the most mature markets, but EMEA adoption is uneven, with some countries leading the way in standardization and others still catching up on infrastructure and supervision.

Globally, at least 60–70 countries now have live or in-progress open banking or open finance frameworks, with particularly rapid growth in regions such as Brazil, Mexico, and the Gulf. In the US, regulators are reworking the Section 1033 “open banking” rule, so data access is currently driven by market standards and industry initiatives rather than a single unified regime.

Examples of Open Banking

Digital Identity

Open banking powers digital identity networks and hubs that help banks, fintechs and merchants verify that a person really owns the account and data they are sharing. These services build on existing Know Your Customer and Customer Due Diligence checks, and increasingly aim to separate core identity data from sensitive financial details so that each can be secured and governed appropriately.

Finance Management

Personal finance management apps and account aggregators use open banking APIs to pull balances, transactions and recurring payments from multiple institutions into a single dashboard. This helps consumers and small businesses get a real‑time view of cash flow, track subscriptions and optimize spending without logging into several banking portals.

Product Matching

Lenders, insurers and wealth providers tap open banking data to assess affordability, income stability and risk more accurately, then surface tailored products such as mortgages, BNPL limits, overdrafts, or investment portfolios. By using consented transaction data instead of static documents alone, they can approve more good customers, price risk dynamically, and reduce friction at application and registration.

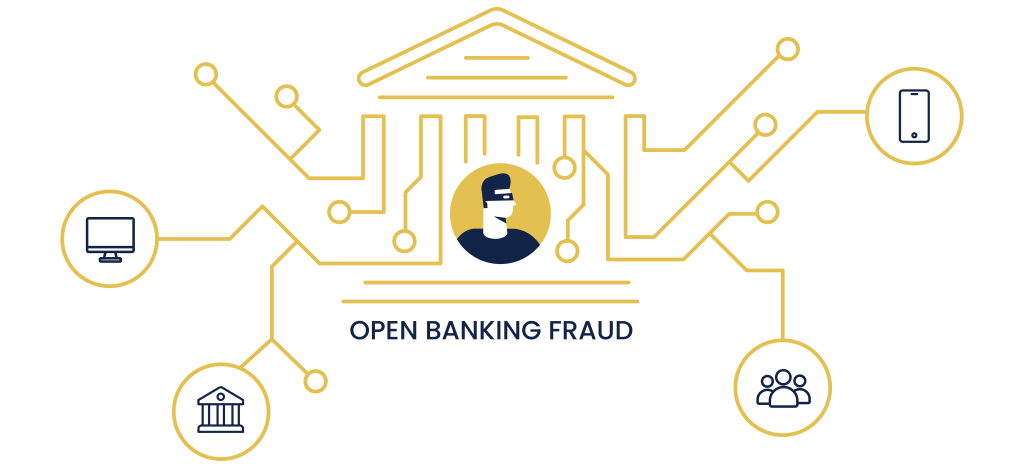

What Is Open Banking Fraud?

Open banking fraud occurs when criminals abuse open banking connections and shared data to access accounts, move money, or open new products in someone else’s name. It typically involves exploiting weak points in APIs, KYC, or consent flows to turn the ecosystem against banks, fintechs, and customers.

Fraudsters use phishing, malware, SIM swapping, and social engineering to steal login credentials or intercept authentication codes. They then use open banking access to view balances, initiate payments, or link additional third-party apps. They may also use stolen or synthetic identity data to pass basic registration checks, creating mule accounts or credit lines that look legitimate until they are used for fraud or money laundering.

Because open banking connects many institutions through shared infrastructure, a single compromised account or API integration can expose multiple accounts and services at once. This multiplies the damage from account takeover and increases the risk that fraud spreads across providers before traditional monitoring detects it.

The Risks of Open Banking Fraud

Sometimes open banking risks can overshadow its benefits. The same APIs that make onboarding effortless also give fraudsters more ways to sneak through weak KYC, exploit gaps between partners, and hide in plain sight without strong registration monitoring.

More Connections Mean More Weak Links

Because open banking ecosystems connect data providers, third-party providers, banks, fintechs, regulators, and government agencies, there are many potential points of failure that sophisticated fraudsters can probe for weak links.

When they succeed, they can mine infiltrated accounts for personal information, currency, reward points, or crypto, and use linked accounts to multiply the damage from a single account takeover.

One Weak KYC Decision can Ripple Across the Network

If all of these services trust the same initial KYC, a single bad onboarding decision can ripple through the entire network. A fraudster who passes one weak check can use that “clean” identity to open bank accounts, apply for loans, or secure credit across multiple partners, while missed risk signals can later translate into painful AML questions and potential financial crime fines.

Shared APIs can Become Single Points of Attack

Shared APIs and common integrations can create attractive single points of technical attack, where one compromised connection exposes several institutions at once and increases the potential reward for organized fraud groups.

“Someone Else Checked” Is a Dangerous Assumption

Open banking can also create a false sense of security. When providers assume someone else in the chain has already done the hard work on KYC and fraud checks, they are less likely to apply their own device, behavioral, and digital footprint analysis at registration.

Weak Onboarding Becomes a Backdoor for Fraud

Fraudsters exploit this information and security asymmetry by targeting the weakest KYC flows with just enough data to pass a basic review, then sitting inside the ecosystem as sleepers, mules, or repeat abusers.

Without strong verification and continuous registration-stage monitoring, these risky profiles can turn into a backdoor for criminals, allowing open banking fraud to spread across products, partners, and regions before anyone notices.

Learn how real-time registration monitoring, digital footprint analysis, and risk-based friction help fintechs stop open banking fraud before accounts are connected.

Read more

How to Prevent Open Banking Risks

Open banking risk can be anticipated and reduced by combining strong controls at registration, smarter ongoing monitoring and closer collaboration across your ecosystem. The goal is to make it easy for good customers to connect accounts, while making it extremely difficult for fraudsters, mules or compromised users to slip through unnoticed.

Secure your data

The more data gets shared, the more potential points of failure are introduced, so it is critical to secure APIs, encryption, access tokens and webhooks end to end, not just your core banking stack. Go beyond minimum regulatory requirements by hardening third‑party integrations, enforcing least‑privilege access and regularly testing open banking connections for misconfigurations that attackers could exploit.

Verify identities in more than one way

ID proofing and identity verification have become the battleground where companies win or lose the fight against open banking fraud, so you should layer document checks with device intelligence, behavioral signals, and digital footprint analysis instead of relying on a single control. Combining biometrics, strong customer authentication and signals such as email, phone and IP reputation helps you spot synthetic identities and risky profiles before they connect bank data or move money.

Monitor logins and activity continuously

Because account takeover and session hijacking are major risks in open banking, it is important to track logins, device changes, geolocation anomalies and high‑risk actions in real time, and alert or step‑up when behavior looks unusual. Dedicated login and activity monitoring lets you detect compromised accounts even when the original KYC was valid, reducing the time fraudsters can use open banking connections to explore balances, create new links or initiate payments.

Vet the companies your customers rely on

If customers are regularly connecting BNPL apps, fast‑loan providers, wallets or investing platforms, you should perform due diligence on those third parties, including how they handle KYC, fraud checks and API security. Building a clearer view of which partners send you the riskiest users allows you to adjust your onboarding thresholds, apply higher friction where needed, and avoid inheriting other companies’ fraud and AML problems.

How SEON Helps Fight Open Bank Fraud

SEON helps fintechs and digital banks stop open banking fraud by turning onboarding and registration into a real‑time risk control, not just a compliance checkbox. By enriching identities from the first interaction with 900+ first‑party data signals, SEON lets you spot synthetic identities, mule accounts and high‑risk profiles before they connect bank data, rather than waiting for suspicious transactions to appear.

At registration and login, SEON combines digital footprint analysis, device intelligence, behavioral signals, and rules or AI‑based scoring to flag risky users, unusual devices, and suspicious patterns across your entire customer base. This lets fraud teams automatically step up authentication, block connections, or route cases for review when open banking access requests look abnormal, all while keeping the experience frictionless for trusted customers.

Because SEON acts as a centralized command center for fraud prevention and AML, you can monitor activity across products and partners, not just within a single channel. Risk teams get a unified view of people, accounts and devices, complete with explainable risk scores and audit‑ready decisioning, so they can quickly investigate alerts, meet regulatory expectations around KYC and AML, and shut down open banking fraud before it spreads across multiple institutions.

Open Banking Fraud FAQ

What are the risks of open banking?

Open banking adds more points of failure where customer data can be stolen. The more data is shared between third-party companies and financial institutions, the more risk there is that the data could fall into the wrong hands.

Is open banking disruptive?

Yes. Historically, financial institutions guarded their customers’ information closely. But thanks to open banking, these large companies are forced to share information with smaller, more agile third-party companies providing financial services and products.