What Is a Money Mule?

A money mule is a person who moves funds on behalf of someone else in order to disguise where the money really came from. The role is often simple on the surface — receiving money and sending it onward — but the purpose behind it is to make criminal proceeds harder to trace. Taking part in this, even unintentionally, is considered a criminal offense in most jurisdictions.

People use different expressions to describe money muling depending on the context. In some regions it is casually referred to as squaring, while in financial crime investigations it’s more closely associated with practices like layering in AML or smurfing.

Although many mules know they’re helping someone hide money, others get pulled in without realizing it, often through online job ads, “quick cash” opportunities, or social engineering.

How Does Money Muling Work?

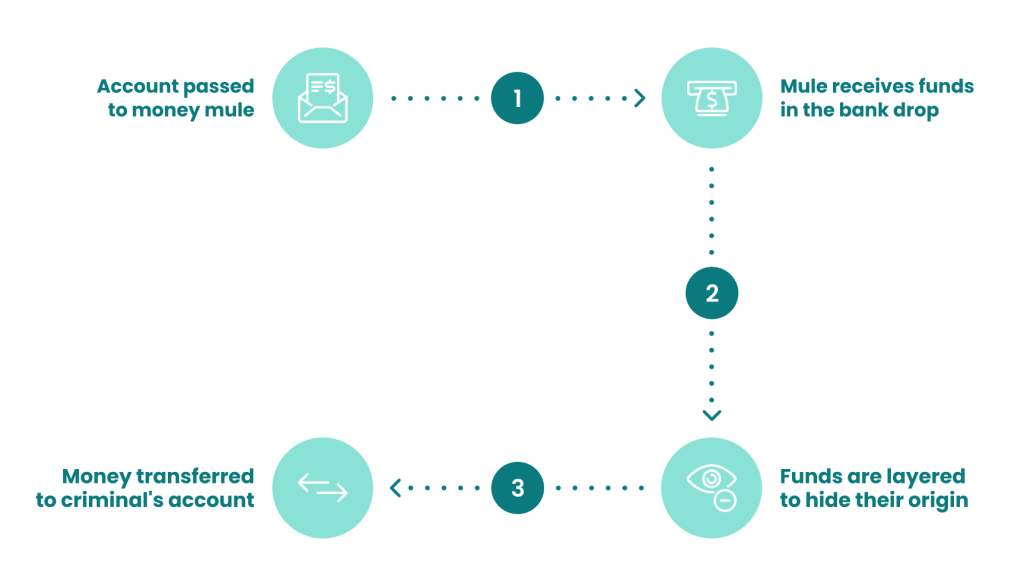

Money muling generally follows a predictable pattern:

- A criminal obtains illicit funds through activities such as phishing, ecommerce fraud, or illegal sales.

- The criminal recruits a money mule, knowingly or unknowingly.

- The mule receives the funds in their bank account or digital wallet.

- The mule transfers, withdraws, or converts the funds to obscure their origin.

- The cleaned funds are passed back to the criminal or a related party.

Common laundering actions include:

- splitting funds into smaller payments (“smurfing”),

- routing money through additional accounts, or

- converting funds to cryptocurrency before forwarding them.

The process mirrors the three stages of money laundering defined by the United Nations:

Placement (the money enters the system), Layering (the mule obscures its trail), and Integration (the criminal receives “cleaned” funds). Europol reports that over 90% of mule transactions are linked to cybercrime, with additional ties to drug trafficking, the arms trade, and terrorism financing.

What Are the Types of Money Mules?

Money mules are often grouped by intent:

Unwitting money mules

These individuals do not realize they are taking part in a crime. They may be manipulated through romance scams, fake job offers, or social engineering.

Witting money mules

These participants suspect that the activity is illegal but ignore the warning signs. They may be asked to open new accounts, move large payments, or “help” someone they met online.

Complicit money mules

These individuals knowingly take part in laundering activity. Some manage networks of mules, run funnel accounts, and receive higher profits for coordinating the operation. to their active participation and awareness of the illegal nature of the activities.

What Businesses Do Money Mules Target?

Any and all companies that are subject to anti-money laundering regulations are legally obliged to take sIndustries that handle, transfer, or store customer funds face the highest risk. Examples include:

- banks and building societies

- fintech and investment platforms

- cryptocurrency exchanges and brokers

- real-estate businesses

- iGaming and gambling operators

Local law determines which organizations fall under AML (anti-money laundering) requirements, but most high-risk sectors must perform due diligence, monitor transactions, and report suspicious behavior.

Supervisory bodies vary by region, such as the OCC in the United States, FSA in Japan, EBA in the European Union, and FCA in the United Kingdom. Globally, the Financial Action Task Force (FATF) provides the main framework used by more than 200 jurisdictions.

Failure to meet AML obligations can result in fines, operational restrictions, and criminal liability.

The Scale of Money Muling Today

Money muling remains a major component of global money laundering activity. It has continued to expand in line with the growth of online fraud, instant payments, digital wallets, and cross-border financial platforms, all of which give criminal networks more ways to move funds quickly and with limited friction.

Recent assessments from the United Nations Office on Drugs and Crime (UNODC) estimate that 2% to 5% of the world’s GDP is still laundered each year. With the global economy now larger than ever, this places the value of illicit funds circulating through the financial system well above $1 trillion, and potentially into several trillion dollars annually.

Operational data from law-enforcement agencies reflects the same trend. Europol’s most recent “European Money Mule Action” operations continue to identify thousands of mule accounts and cross-border transactions each year. These investigations frequently uncover organized recruitment networks, large-scale fraud schemes, and a growing reliance on digital payment methods to obscure transaction trails.

Younger demographics are still heavily targeted, particularly through social media, online job boards, and messaging platforms that make it easier for criminals to approach potential recruits anonymously. Financial institutions and fintech companies continue to report increases in suspicious mule-related activity, especially where payments are fast, reversible, or have limited onboarding friction.

The Warning Signs of Money Muling for Businesses

Activity that would be unreasonable or unlikely under normal standards for one’s average customer can be a warning sign of money muling. For example:

- Customer unwilling to pass KYC verification checks

- Money deposited/withdrawn unusually quickly

- User keeps logging in from different, remote geolocations

- Large spontaneous transactions

- Hundreds/thousands of small sums paid in and withdrawn in bulk

For crime-fighting authorities, “fighting money laundering goes hand in hand with investigating the crimes it is linked to”, as Interpol notes. Their efforts are big picture and mostly focused on using lower-tier money mule activity to investigate and catch criminal masterminds higher up.

However, for companies who want to ensure their users do not participate in – and they themselves are not implicated in – illegal money mule activity, there are available solutions in the form of AML fraud detection technology.

Depending on each organization’s circumstances, customizable passive monitoring of user activity can alert risk analysts about any red flags, fine-tuning and adjusting as needed. Such tools can scale up or down, while there are various niche and custom-built solutions as well.

Money mules are just one of the ways fraudsters will avoid detection when they attempt to launder money.

Read more

Sources

- Interpol: Money laundering

- Europol: 422 arrested and 4,031 money mules identified in global crackdown on money laundering

- Europol: Money Muling Guide

- UK Finance: Money mule recruiters use fake online job adverts to target ‘Generation Covid’

- FBI.gov: Don’t Be a Mule: Awareness Can Prevent Crime

- UN Office on Drugs and Crime: Money Laundering

- FATF: Topic: FATF Recommendations