Financial institutions and businesses face growing pressure to prevent criminal exploitation of their services. In the first half of 2024, global regulators issued 80 AML fines totaling $263 million—a 31% increase from 2023. The Asia-Pacific region saw a dramatic 266% rise, with penalties exceeding $46 million.

This surge reflects stricter regulatory enforcement, including a $65 million fine against a U.S. subsidiary of a Canadian bank for compliance failures. Fines for transaction monitoring violations also jumped to $30.5 million, up from $6 million last year.

To combat increasingly sophisticated financial crimes, organizations must adopt strong AML strategies to detect illicit funds, avoid hefty fines, and safeguard their reputation.

What Is AML Fraud?

AML fraud happens when money is illegally laundered (layered) through your products or services. Regardless of whether you are in banking, real estate, or even ecommerce, criminals will use any opportunity to launder money illegally acquired.

While all money laundering is illegal, the fraud part happens if you have anti-money laundering controls in place, and criminals bypass them to reach their goals: layering the illegal funds, either themselves or using a money mule.

How Do Criminals Fool AML Identity Checks?

Whether you’re a traditional financial institution, neobank or crypto exchange, the onboarding process is where you’ll need to be smart about checking data. And it’s also your duty to go above and beyond the obligatory KYC regulations.

With Fake and Stolen IDs

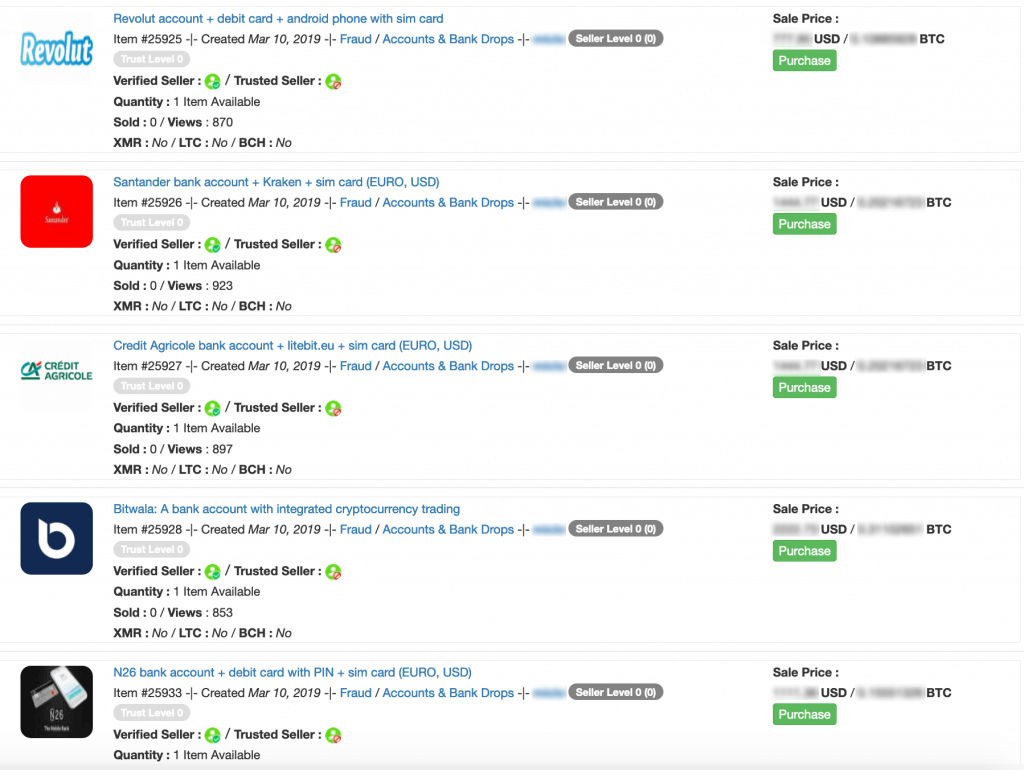

Stolen IDs that come from data breaches are often bought in bulk on the darknet, as well as information to create fake IDs, sometimes candidly advertised as full packages designed to enable you to open online bank accounts. Fraudsters also go to great lengths to acquire personal data via phishing, fake job openings, or plain old hacking.

If you want a drop account, you also have the option to purchase pre-created neobank accounts for your fraudulent needs. Just find one on the darknet and buy the login details from a seller.

With Synthetic IDs

Synthetic IDs, meanwhile, combine real and fake personal data. For instance, fraudsters often use stolen ID details from children with clean credit records and use them for loan fraud.

With real credit information, it’s extremely easy to create fake IDs using templates designed to fool modern credit scoring. You can even find online services that specialize in Photoshop editing for ID fakes and 2FA verification.

Why Is AML Fraud Detection Important?

Of course, companies implement AML software & tools in order to fight AML fraud and improve AML detection, but a big plus is that it increases efficiency when handling a higher volume of transactions. With machine learning and velocity rules, a business can easily automate transactions with no human input by scanning multiple data sources to lower the need for manual reviews.

As society has only further headed towards the digital age, money laundering activities continue to increase and diversify – as does fraud – and staying on top of this is key.

Furthermore, AML software can remove compliance risks. Whether you are a crypto exchange, a neobank, or a traditional financial institution, it’s your duty to be aware of and follow AML regulations. While there are different levels depending on your vertical, the core rules to follow include:

- AML holding period: A recommendation that funds deposited in an account must be held for a minimum of five trading days.

- Reporting suspicious activity: Businesses must monitor customer deposits and transactions. Large sums, especially those exceeding $10,000, must be given extra attention by verifying their origin.

- AML education: The responsibility of letting customers know about AML laws falls on the shoulders of the business.

- Logging financial information: Businesses must keep extensive records that can be used to investigate suspicious financial transactions.

- Customer due diligence (CDD): Knowing who your customers are through extensive KYC verification checks is also the business’s responsibility.

Are you in a sector mandated by law to be AML compliant? Discover our impartial reviews of efficient and useful software here.

Read more

The Basics of Money Laundering

Criminals who acquire money through illegal means want to ensure the funds cannot be traced back to them. The process, known as money laundering, usually involves running the money through a legitimate business. This can be a cash-based brick-and-mortar shop or an online operation.

There are three steps involved in money laundering:

- Placement: The dirty money is placed into the legitimate financial system.

- Layering: The money is concealed through transactions and bookkeeping tricks.

- Integration: The money is now laundered and withdrawn from a legitimate account by criminals.

The Challenges of AML Detection Solutions

The biggest controversy surrounding AML is whether it’s effective at all. While heavy fines are so large that they can destroy a business, there is little evidence that the current approach helps to catch terrorists, criminals or insiders who abuse the financial system. This has been highlighted in several reports as well as opinion pieces in recent years, including in The Economist and on Reuters.

And still, financial institutions must employ sizable teams of staff and consultants to help with transaction monitoring, even when it’s automated.

This is in part because of the ever-growing complexity of payment streams (ecommerce, increase of online volume, virtual currencies, prepaid cards), which, coupled with an increase in more sophisticated attacks, is causing a real headache for larger businesses to stay ahead of fraudsters.

The main challenge, however, isn’t necessarily in deploying the right team of resources to prevent money laundering. It’s about the friction that these checks create for customers.

This is particularly damaging for neobanks, whose entire business model relies on quick and painless onboarding via mobile or desktop. Throw in too many ID verifications and questions, and your potential customers might just turn elsewhere.

It doesn’t matter if you use in-house tools or third-party companies like Onfido (as does Revolut); the AML solution is stacked on top of already heavy regulations regarding customers’ identity in the form of KYC or PEP and Sanctions checks.

How Does AML Fraud Work?

Money laundering in its essence focuses on allowing a criminal to sign up for an account with a fake identity and laundering money through a business.

So, can you trust your AML solution for AML detection?

What if you are diligent in your AML checks but accidentally miss some falsified information? Many developing countries don’t have bureaus for ID information to reliably perform checks with.

Real criminals, moreover, have every incentive to hide their IDs from you. And there is no shortage of options for them to build fake profiles.

1. Criminals acquire stolen ID scans from the deep web.

2. They open bank or neobank accounts as “drops”.

3. They deposit money in these accounts and withdraw to P2P money transfer apps or crypto exchanges.

4. The funds are “tumbled”, i.e. moved across multiple accounts so they become untraceable.

Understanding these steps helps to highlight where the challenge lies for financial institutions. The onboarding stage, where you collect all your customer information, is the stage where money launderers will work the hardest to fool you.

This brings us to the topic of tools you can put in place within your organization.

What Connects AML and Fraud Detection?

Essentially, AML compliance and fraud detection efforts require similar checks. You must ensure you can confirm your user’s identity, and flag any suspicious activity, both at the onboarding and transaction stage (deposits and withdrawals).

This is why a continuous detection solution like SEON’s can help simultaneously with anti-fraud and anti-money laundering. Not just an AML and fraud prevention provider, SEON also allows you to keep granular logs of your AML screening and perform it at regular intervals, helping you towards your AML programs.

What Features to Look for in AML Software

If you’re an organization operating online and offering some form of payout, it’s vital to utilize real-time fraud detection software. However, the importance of specific features will vary depending on the requirements of your business and industry.

On top of any compliance/regulatory demands, some specific features that you might want to look out for include:

- Digital footprinting capabilities: Create a basic user profile that details information from external sources on a single data point – for example, checking an email address to see if it’s deliverable and what domain type can reveal a level of risk.

- Customizable rules and risk scoring: To help businesses streamline processing times and boost accuracy, a customizable ruleset will approve or reject any given action in real time without impacting the user’s journey. This is best calculated via an overall risk score.

- Social media lookup: Building on digital footprinting, some software providers offer a social media tracking API that offers more insights about the user, essentially acting as an online passport.

- PEP screening and checks: Transactions involving a politically exposed person (PEP) or their family (RCA)– i.e., a president, politician, mayor, etc. – are considered high-risk due to the nature of the person’s position and authority. Applying enhanced customer due diligence with these individuals helps prevent potential money laundering.

- Sanctions lists checks: Sanctions lists that apply to your locale also need to be checked for any potential matches.

- Crime and fugitive watchlists and other blacklists: AML screening also involves ensuring that the customer’s name is not on any law enforcement lists.

- Pricing: For smaller businesses, paying per API call offers the most flexibility as your business grows. Businesses using the option of paying per individual check can complete operations in-house instead of outsourcing any transactions, which is often more costly.

How to Integrate AML Detection or Tools into Your Business

For ease, some businesses simply work with the AML software provided by their chosen payment gateway/processor. For example, Stripe has its own Radar tool, which uses historical payments and card data gathered through its platform to identify potential risks. SEON also provides a convenient AML screening tool.

Some companies choose to employ their own in-house fraud prevention teams, as this provides more flexibility and security when faced with specific fraud challenges. However, to be truly successful, you need champions who are highly knowledgeable in the space and make the right hires when scaling. Otherwise, this can become an expensive endeavor.

Alternatively, for most companies, we would recommend looking at cloud-based solutions from third-party providers that enable you to integrate APIs to create a multi-layered defense that is developed solely around the needs of your business.

With fraud detection solution, maintenance and upgrades happen when needed – but the multi-layered approach gives you complete control and flexibility over your prevention arsenal without any heavy fees or commitments.

Discover scalable AML solutions tailored to your needs. From payment gateway tools to API-driven systems, our insights help you achieve cost-efficient, robust fraud prevention with flexible, multi-layered protection.

See How It Works

How to Screen for Bad IDs

We’ve already extensively covered how SEON’s tools, like digital footprint analysis and dynamic friction, can help, especially in the context of onboarding users with zero friction.

But it’s worth noting here that a key element of improving your AML compliance checks is to look at user behavior. This is something an experienced risk team can do, but it’s also possible to automate the process with certain risk management rules.

Put simply, a fraud management engine will be monitoring and logging all user activity on your platform. And it’s up to you to feed that data through certain rules to see if the activity looks suspicious or not.

How to Use SEON to Help Your AML Compliance

SEON offers a robust solution designed to enhance your compliance efforts. Our AML offering enables both manual and automated screenings against crucial watchlists, including sanctions and Politically Exposed Persons (PEP) lists, allowing you to customise the frequency of these checks based on your specific needs. Our platform also supports effective transaction monitoring through tailored rules that can quickly adapt to regulatory changes.

In addition, SEON’s fraud prevention tools identify risks such as multi-accounting and synthetic identity fraud, helping to minimize money laundering opportunities. The platform maintains detailed records of compliance checks, simplifying the filing of necessary reports like Suspicious Activity Reports (SARs) and demonstrating your adherence to regulations.

SEON also provides alternative data sources that enhance manual reviews and serve as a pre-KYC step so can effectively identify fraudulent customers before they reach KYC and strengthen your AML compliance across your operations.

FAQ

This depends entirely on your requirements. An all-in-one suite might cost more/involve a longer commitment but will quickly lift the majority of work from your business, whereas developing a multi-layered defense might mean taking time to identify the right tools but will be much more affordable in the long run.

Not at all! AML stands for anti-money laundering, which is legislation put in place to combat money laundering, which is a type of fraud. Certain organizations, such as banks, are mandated by law to follow AML risk assessment requirements in almost every country.

A good fraud prevention tool will automate as much risk management as possible by calculating risk before declining, accepting, or sending for manual review accordingly. With key features such as machine learning, digital footprinting and device fingerprinting, you can create a clearer picture of the person trying to operate on your site.

Sources

- Finextra: Bank AML fine values in 2020 already outstripping 2019

- Guardian: Is money laundering scandal at Danske Bank the largest in history?

- Reuters: Anti-money laundering controls failing to detect terrorists, cartels, and sanctioned states

- The Economist: The war against money laundering is being lost

- Fenergo: Global Financial Institution Penalties on the Decline in 2021

You might be interested in: