An AML toolkit serves a two-pronged purpose, functioning as a compliance training tool and as a framework to ensure your company does not have to pay regulatory fines.

But what does it look like in practice, and how can you build your own?

Since AML fines surged by 53% in 2022 reaching a record $5 billion, it is more important than ever for businesses of all sizes to answer these questions.

What Is an AML Toolkit?

An AML toolkit includes all the tools, software and features necessary for your company to ensure anti-money laundering compliance. It will typically include transaction monitoring systems as well as screening tools to check PEP, sanctions, and crime watchlists, among other considerations.

Because anti-money laundering compliance varies from country to country and governments incentivize a risk-based approach, there is no global, standardized way to select what goes into your AML toolkit.

However, general guidelines can be found by consulting the Financial Action Task Force (FATF).

A recurring theme with these guidelines is to establish a risk-based money laundering prevention strategy, which includes writing policies, employee training, deploying procedures, and often integrating adequate AML software.

Note that some companies also sell anti-money laundering toolkits in the form of educational content based on the latest legislative and regulatory changes. The content may be delivered via online books or video courses, among others.

Partner with SEON’s AML solution to boost your AML compliance without friction and stop all kinds of fraud with real-time data enrichment and advanced APIs.

Ask an Expert

How to Build Your AML Toolkit

Here is a series of steps you should follow to build your own AML toolkit. While there are overlaps with our AML checklist, this is an abridged version that focuses on learning more about the latest laws and regulations:

- Assess the risk to your company: Before diving into AML regulations, you must know which ones are relevant to your business. While, historically, only financial institutions were required to meet anti-money laundering mandates, these days, any business with the potential to be used for money laundering can be considered high-risk and mandated to follow AML legislation. That can include estate agents, hedge funds, forex trading, high-end retailers, and even BNPL companies, depending on the jurisdiction.

- Set up your system and controls: Whether you deploy a built-in solution or cloud-based software, you must first prepare for what would happen if you do suspect money is laundered by your customers. This will involve creating a workflow for data logging and reporting the suspects to the authorities using the right templates (for instance, with a Suspicious Activity Report).

- Deploy name/entity screening workflows: You want to be able to quickly and automatically check for customer names against government databases. That means performing PEP screening, RCA checks, and looking at crime and sanctions lists as well. At this stage, it is wise to enable continuous AML monitoring where available or conduct this yourself manually at regular intervals. A customer’s name may suddenly appear on AML lists – for instance, after they’ve had a job promotion.

- Monitor suspicious activity: AML suspicious activity monitoring is essential for industries subject to regulatory oversight. This involves monitoring transactions—such as deposits exceeding a certain threshold—and identifying patterns of regular or irregular payments that could indicate criminal behavior.

- Combine AML with other forms of due diligence: Because AML compliance forces you to check customers’ names, you might as well use the opportunity to combine these checks with other CDD tools, such as identity verification (IDV) software. Most organizations face a challenge when they need to meet two sets of compliance requirements. Combining them into one offers a potential, cost-effective solution.

- Stay on top of the latest AML laws and regulations: Another common challenge companies face is a lack of resources dedicated to staying up to date with the latest regulations. While a dedicated compliance or legal team should be able to provide guidance, smaller businesses have no substitute for simply regularly reading about regulations.

Speaking of laws and regulations, we’ve compiled a handful you should know about, regardless of whether they target your region.

AML Laws and Regulations You Should Know About

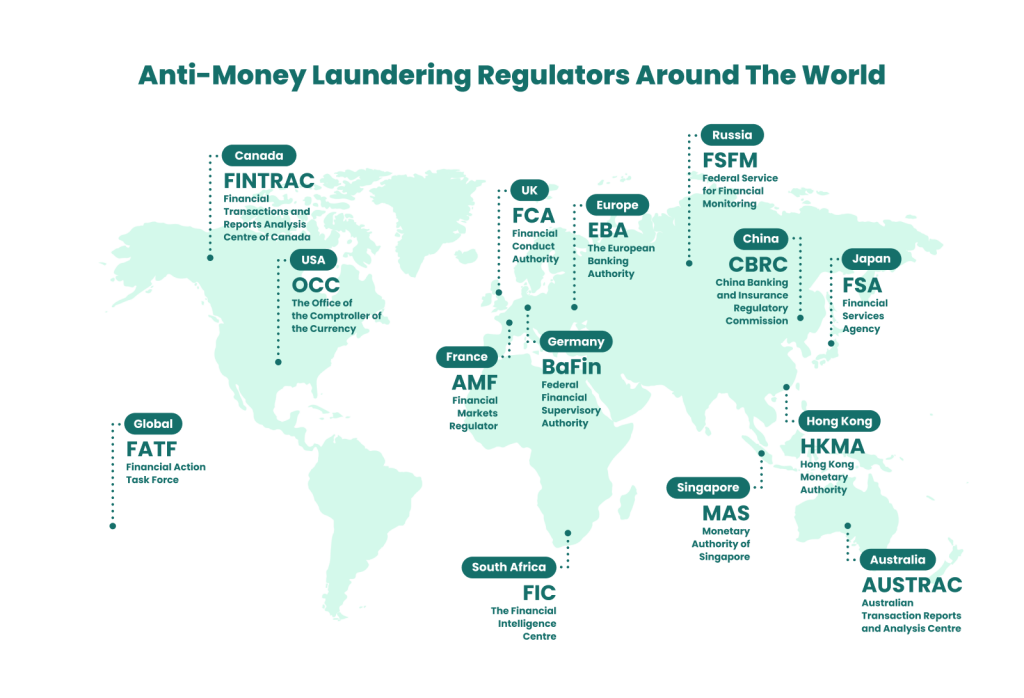

AML regulations vary from one country to the next. However, some noteworthy regulations may influence how anti-money laundering policies are implemented worldwide. The Financial Action Task Force (FATF) lists recommendations that are more or less endorsed globally.

With that said, here are some AML laws and regulations found around the world:

The Bank Secrecy Act (US)

The Bank Secrecy Act – also known as BSA or the Currency and Foreign Transaction Reporting Act – was passed in 1970 by the United States Congress.

It requires US financial institutions to collaborate with the government, namely by:

- reporting cash transactions above $10,000

- verifying the identity of customers

- keeping records of the above

It is an evolving piece of legislation, which FinCEN, the US Financial Crimes Enforcement Network, regulates.

6AMLD (EU)

6AMLD is the 6th Anti-Money Laundering Directive. It covers companies with financial activity in the EU and was issued on October 23, 2018.

The regulation includes updated definitions of AML in the region, notably also covering cryptocurrencies and digital tokens. It paved the way for better coordination between cooperation between the European Union’s member states when combating money laundering, issuing fines, and escalating legal procedures against guilty parties.

The Money Laundering and Terrorist Financing Regulations (UK)

Amended in 2022, the Money Laundering and Terrorist Financing Regulations offer guidance on AML compliance in the UK.

It originally came into force on January 10, 2020, and covers the scope of the mandates, requirements for reporting, and obligations in terms of policies, controls, and procedures.

Corruption, Drug Trafficking and Other Serious Crimes Act (Singapore)

Singapore’s AML legislation was passed along with the Payment Services Act (PSA), which designated the responsible authority as the Monetary Authority of Singapore (MAS).

The agency published a report of its activities every 18 months and is known to scrutinize shell companies in the region.

The Prevention of Money Laundering Act, 2002 (India)

While India only became a nation member of the Financial Action Task Force in 2010, its Prevention of Money Laundering Bill goes as far back as 1998. It has been amended several times and claims three objectives:

- to prevent and control money laundering

- to confiscate and seize the property acquired from the laundered money

- to deal with any other issue in relation to money laundering in India

It also established the Financial Intelligence Unit of India, formed in 2004 to coordinate the country’s AML efforts.

Anti-Money Laundering and Counter-Terrorism Financing Act (Australia)

Last updated in 2021, Australia’s AML and CFT laws are administered by Home Affairs and cover a number of points for reporting, disclosure of personal information, and identity verification practices. Designated services are also listed and include financial services, goods suppliers, building societies, credit unions, and more.

Partner with SEON to reduce fraud rates in your business with real-time data enrichment, whitebox machine learning, and advanced APIs.

Ask an Expert

How SEON Can Help With Your AML Toolkit

SEON is designed to tick two compliance boxes off at once in the form of KYC and AML. It’s also a powerful fraud prevention solution, which lets you monitor transactions to get better insights into your customers’ funds.

For the AML part, we let you screen customer names via API to check PEP, RCA, sanctions, and crime watchlists, among others. It is all available via an intuitive UI, which makes it easy to manage risk, flag suspicious users, and even monitor unusual behavior.

Thanks to flexible, pay-per-API call pricing, it’s also a cost-effective way to reduce fraud, improve compliance, and protect your legitimate users – as well as your business.

Frequently Asked Question

The anti-money laundering clause is set out by the UK’s Proceeds of Crime Act 2002. It is designed to align the implementation of anti-money laundering requirements to meet the EU’s Money Laundering Directive.

Identifying money laundering begins by checking for names on databases created by the government and criminal agencies. You also want to look at complex ownership structures, corporate funds used for private spending, and suspicious transactions.

AML defenses can be organized into three blocks that include KYC for identity verification, AML screening to ensure you’re not dealing with high-risk individuals, and transaction monitoring to look at the movement of funds.

Sources

- City A.M.: Financial crime: Anti-money laundering and crypto fines surge to £4bn in regulatory crackdown

- Fincen: The Bank Secrecy Act

- Legislation.gov.uk: The Money Laundering and Terrorist Financing (Amendment) Regulations 2022

- Federal Register of Legislation: Anti-Money Laundering and Counter-Terrorism Financing Act 2006