Financial institutions are under constant pressure to prevent illicit transactions, and one of their most important defenses is PEP screening. Designed to flag individuals with elevated financial-crime risk due to political exposure, PEP checks are a core requirement of AML compliance.

The stakes continue to rise. In October 2024, TD Bank became the largest U.S. bank in history to plead guilty to federal AML violations, paying a record $3.1 billion in penalties. Cases like this show why strong due diligence and reliable PEP screening software are essential.

This guide explains how PEP screening works, the key compliance obligations, and best practices for managing high-risk individuals effectively.

What Is a Politically Exposed Person?

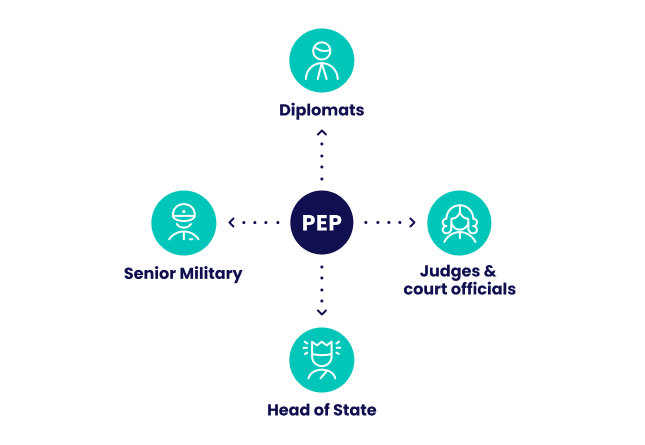

A Politically Exposed Person (PEP) is an individual who currently holds or has previously held a high-ranking public role, such as a government official, senior politician, military leader or judicial authority. This designation also extends to their close associates and family members, due to the potential for influence and access to state resources. Because of their elevated exposure to political power and decision-making, PEPs are inherently considered to carry a higher risk of involvement in illicit financial activities, including bribery, corruption, and money laundering.

What Is PEP Screening?

PEP screening, often referred to as a PEP check, is the process of identifying these individuals within your customer or partner base. It involves referencing structured databases and clearly defined profiles of political exposure to flag elevated risk and ensure your organization complies with anti-money laundering (AML) regulations.

The Importance of PEP Checks for Businesses

Conducting PEP checks is a critical step in safeguarding businesses from becoming conduits for financial crime. By identifying individuals with political influence or close ties to power, companies can proactively detect and mitigate the heightened risks associated with corruption, bribery and money laundering. Beyond regulatory compliance, effective PEP screening also protects a business’s reputation, strengthens customer due diligence and builds long-term trust with stakeholders and financial partners.

While PEP screening was once a requirement mainly for banks and large financial institutions, its importance has expanded significantly across various industries. Today, depending on the jurisdiction, many sectors are expected or even legally required to incorporate PEP checks as part of their anti-money laundering (AML) and Know Your Customer (KYC) protocols. Industries where PEP checks are especially relevant include:

- iGaming: Online gaming platforms handling high-value transactions must address the risks of anonymous gambling and fraud.

- Fintech: Companies offering digital wallets, lending services or peer-to-peer payments face regulatory scrutiny due to the volume and velocity of financial activity.

- Financial Services: Hedge funds, investment firms and accountancy practices manage large sums of money, making them attractive targets for illicit activity.

- Payments: Payment service providers and gateways that process international transactions need to prevent their networks from being exploited for money laundering.

- eCommerce: Online retailers, particularly those dealing in luxury or high-ticket items, must remain vigilant against fraudulent behavior and criminal money flows.

Given that AML requirements vary widely between regions, it’s essential for businesses to consult their local regulatory authorities to determine the specific obligations around PEP screening for their industry and jurisdiction.

Consequences of Failing to Perform PEP Checks

Conducting PEP (Politically Exposed Persons) checks is a legal obligation in many jurisdictions, and failing to do so can lead to serious repercussions:

- Substantial fines: Regulatory bodies are increasingly strict. In November 2024, the Financial Conduct Authority fined Starling Bank £28.96 million (approximately $36 million) for inadequate PEP and sanctions screenings.

- Reputational damage: Non-compliance can erode trust among shareholders and customers, leading to long-lasting harm to a company’s brand.

- Decline in stock value: Research from Fenergo indicates that regulatory penalties significantly disrupt investor confidence, negatively impacting share prices. In 2024, financial institutions faced an average stock drop of 6.5% on the day a fine was announced, with losses persisting for months afterward.

For smaller businesses, the impact can be even more severe, as legal battles and fines may disrupt operations and hinder growth. In summary, rigorous PEP checks are essential not only for regulatory compliance but also for protecting against financial penalties and reputational damage.

Compare sanction screening tools to protect your business and choose the best fit.

Explore this list

Who Audits the PEP Screening?

PEP screening is mandated in many jurisdictions, but oversight varies by country. Most nations follow the definitions and guidance provided by the Financial Action Task Force (FATF), which sets global AML standards and outlines how politically exposed persons should be identified and monitored.

In the European Union, requirements stem from the 6th Anti-Money Laundering Directive (6AMLD), which defines different PEP categories and mandates enhanced due diligence.

In the United States, the Financial Crimes Enforcement Network (FinCEN) guides financial institutions to apply a risk-based approach to PEPs as part of broader AML obligations.

How The PEP Screening Process Works Step-by-Step

PEP screening involves a structured approach to identifying and managing individuals who pose elevated financial crime risks due to political exposure. Here’s how the process typically unfolds:

1. Data Collection and Identification

The first step involves gathering key personal and business information about a customer, such as full name, date of birth, nationality and identification documents. This data is essential for verifying the individual’s identity and ensuring accurate screening results.

2. Screening Against PEP Databases

Once the data is collected, it is cross-checked against various official and commercial PEP databases. These include lists maintained by regulatory authorities, international bodies and reputable third-party data providers. The goal is to flag any matches with known politically exposed individuals or their associates.

3. Risk Assessment and Categorization

If a match is identified, the individual is assessed to determine the level of financial crime risk they pose. Factors such as the nature of their political role, geographical risk and connection to high-risk sectors help categorize the individual as low, medium or high risk.

4. Enhanced Due Diligence (EDD)

For high-risk individuals, organizations must conduct a more thorough review known as enhanced due diligence (EDD). This includes verifying the source of funds, understanding the purpose of transactions and obtaining senior management approval before onboarding or continuing a business relationship.

5. Decision

Based on the risk assessment and due diligence findings, the organization must make an informed decision on whether to onboard, continue or terminate the relationship with the individual. This step may involve compliance and legal teams, particularly for high-risk cases.

6. Ongoing Monitoring and Alerts

PEP status can change over time: individuals may enter or leave public office, gain new associations or face emerging risks. As such, businesses must implement ongoing monitoring systems and set up alerts to detect changes in status or behavior that could impact risk exposure.

3 Ways to Perform PEP Screening

While regulators must ensure you perform your customer due diligence (CDD) and enhanced due diligence (EDD) checks, there are no strict rules on how to do PEP screening.

Here are three methods that may generally suit your organization, depending on your scale and risk appetite.

Manual PEP Screening

The easiest (and most resource-intensive) way to run a PEP check is simply to manually look at the right lists. Businesses can do this by accessing the information on PEPs available through official government websites, public registers, or commercial databases.

OSINT sources and OSINT tools can also accelerate the process by aggregating information about a person based on their name.

Finally, you could also monitor news reports from reputable sources to monitor the latest political or judiciary appointments.

Manual PEP Checks With an AML Solution

The second option is to manually check for names by inputting them into specialist software. This has pros and cons. The advantage is that it speeds up searches by automatically aggregating results from several PEP lists worldwide. The results are sometimes processed via algorithms to provide the best estimate of whether you are dealing with the right person or not.

However, this can be challenging since names are not unique identifiers. You still need to confirm the information manually to ensure you are verifying the correct identity.

Fully Automated PEP Checks

The most ambitious businesses subjected to AML rules will sometimes deploy fully automated checks.

This involves integrating sophisticated AML software, either on-premise or via API. Automated AML verification also works by aggregating data from several PEP lists around the world and running it through algorithms.

The advantage of fully automated PEP checks is that you can verify the identities of large numbers of new customers in nearly real-time. The challenge is that, once again, people with similar names may be processed as false positives or negatives.

How SEON Does PEP Screening

SEON acts as a unified command center for fraud and AML compliance, bringing together PEP screening, sanctions and watchlist checks, automated monitoring, case management and AI-powered risk scoring into one streamlined platform. What makes it uniquely effective is the way it enriches traditional AML screening with digital footprint analysis and device intelligence, giving compliance teams deeper context behind every customer interaction.

By continuously updating PEP data and combining it with real-time digital, device and behavioral signals, SEON helps identify risk earlier, reduce false positives and support confident decision-making. With built-in workflows, audit-ready reporting, and visibility across the entire customer lifecycle, SEON transforms fragmented compliance processes into one intelligent, proactive system.

Frequently Asked Questions

How do I check if someone is a PEP?

To check if someone is a PEP, you can manually enter their name on politically exposed persons lists found on official websites. You can also look at open-source or commercial databases or even monitor media sources. However, most online businesses rely on AML software to automatically aggregate PEP list data for them.

How do I run a PEP check?

You are allowed to run a PEP check manually by searching for information about a person on official government PEP lists. You can also rely on AML software to automatically scan for that person’s name on dozens of aggregated databases.

How do PEP screening tools work and what features should you look for?

PEP screening tools compare customer data against global PEP databases using advanced algorithms and fuzzy matching to detect potential risks, even with name variations. These tools may be manual, semi-automated, or fully automated, and often include real-time alerts, sanctions list integration, customizable risk scoring, and enhanced due diligence workflows. Leading solutions like SEON also offer AI-powered false positive reduction, digital footprint analysis, and device intelligence to give compliance teams deeper context and improve accuracy.

Sources

- Financial Conduct Authority: FCA fines Gatehouse Bank £1.5m for poor anti-money laundering checks

- Global Trade Review: Share price and reputational damage: banks count cost of AML failings

- PWC: Five forces that will reshape the global landscape of anti-bribery and anti-corruption