With the signs of a prolonged recession clearly on the horizon, we are likely set to see a shift in the fraud landscape, including a rise in business-to-business fraud.

The past decade saw ecommerce blossom, as well as the development of a vast cybercrime ecosystem that could be dubbed B2C, as it focused on using the stolen identities of consumers to defraud merchants.

Yet, this decade also saw B2B commerce digitalize to an unprecedented degree, allowing organizations to provide more convenience to consumers, automate operations, and do business with as little friction as possible. The great fintech revolution has made it easier for almost anyone around the globe to start a business that operates online.

But the same goes for fraudsters, fraudulent schemes and businesses. Now, B2B fraud is expected to become one of the biggest fraud trends of 2023.

What Is B2B Fraud?

Business to business fraud is defined as any fraudulent activity targeting an organization that is undertaken by someone who represents, or claims to represent, a business – or is enabled by it.

According to Capital One, up to 19% of new B2B inquiries conducted online are linked to attempted fraud, though this includes very obviously fraudulent communications such as scam emails. From there, the fraudster or fraud ring will attempt to defraud the targeted organization of money or sensitive, valuable information.

In reality, B2B scams and fraud take so many guises that it is impossible to provide an exhaustive list. One day, danger could be waiting at a fake online shop, or a new supplier could have set up a triangulation scheme. The next day, maybe fraudsters have created a fake charity appealing to businesses for donations, or a company abusing credit lines.

A much-publicized iteration of this seen over the last few years were pandemic scams, where fake, non-existent, or non-eligible businesses claimed support grants provided by various government organizations. In fact, as recently as August 2022, the US Secret Service had recovered $286 million in funds lost to “illegally obtained coronavirus relief funds” – which demonstrates just how ready fraudsters are to take advantage of new developments.

Why Is B2B Fraud on the Rise?

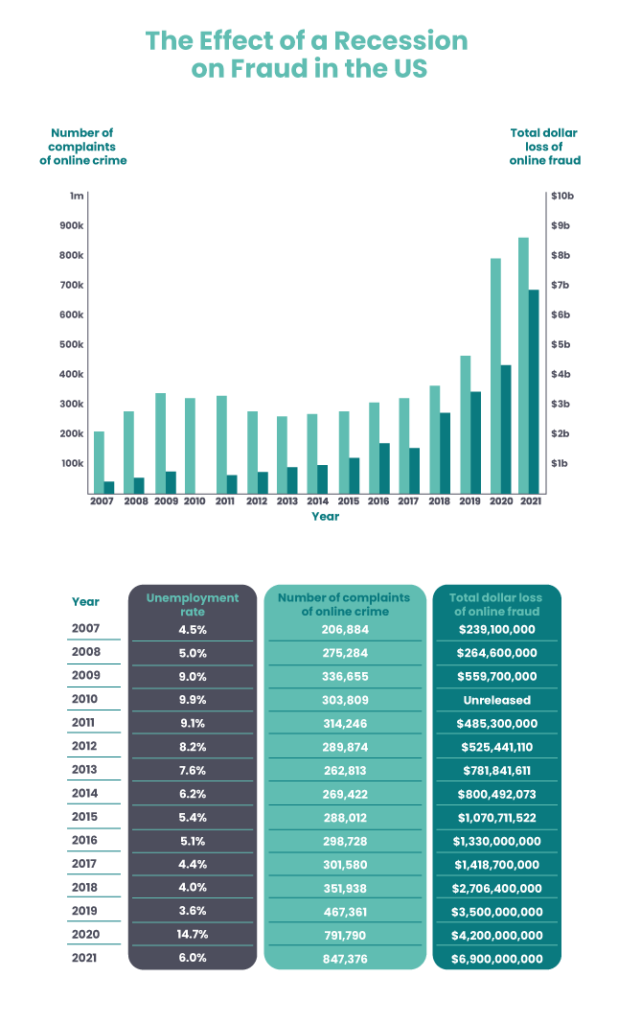

As we saw in our Recession Fraud Report, times of economic hardship are likely to bring about a rise in scam businesses that pose as legitimate merchants in order to rob or entrap consumers in one way or another. These are easy to set up and scale, and there is an ample supply of unsavory characters looking for a quick buck.

However, we are also due an increase in B2B fraud. Fraudsters set up firms that seem legitimate at the onset, relying on suppliers and business loans to ramp up their credit, operating as dream clients in times of economic hardship – until they don’t, and the fraud is revealed, harming their creditors and investors. We are going to start seeing more and more of this.

It’s important to note that this phenomenon isn’t just led by career criminals – many honest businesses might turn into fraudulent operations in hopes of surviving the rough times by illegal practices. But B2B fraud goes beyond this common example.

Types of B2B Fraud and B2B scams

As it merely describes the instigator and target rather than specific methodology, business to business fraud can look like many different things. We tend to categorize these attacks by the type of business they claim to be, and the duration of the scheme.

Bust-out fraud

The fraudster sets up an ostensibly legitimate merchant account with a bank or even a marketplace, attempts as many scam or fraudulent transactions as they can, and then simply abandons it when found out. This type of fraud overlaps with short firm fraud or long firm fraud, as it also relies on supplier credit and fraudsters vanish when discovered. Criminals may make use of fraudulent IDs to perform synthetic identity fraud and to set these accounts up.

Merchant fraud

Scam merchants can target businesses or consumers. Practically, merchant fraud involves someone setting up shop as a merchant and then defrauding their target. They may obtain merchant accounts in online marketplaces or register with payment processors/PSPs. The idea is that they want to become able to process payments in a seemingly legitimate manner but sell rip-off products or simply never deliver – making as much dough as possible before they are shut down. Merchant fraud is a particular concern for acquiring banks, payment processors and other fintechs.

Triangulation fraud

A special type of merchant fraud, this scheme sees the fraudster masquerade as a legitimate shop owner, selling an item they do not actually have. They then order the item from a legitimate shop, using a stolen card, and have it shipped to the original buyer. As a result, the fraudster has obtained some clean money and the legitimate shop often faces chargebacks when the owner of the stolen card notices the unauthorized purchase. Such a scheme can, of course, defraud organizations as well as consumers.

Short firm fraud

The term short firm fraud refers to all business fraud that takes place in the short term – in other words, a quick-to-instigate scheme that may see the fraudster disappear with the stolen funds within a few weeks.

Long firm fraud

Long-term firm fraud relies on supplier credit. The fraudulent business builds up trust over months or even years, in order to be able to defraud the target of more funds in the long term. As part of this, they may generate fake sales, do “carding” with stolen credit cards, or deliberately fulfill several legitimate orders, to enable larger-scale schemes in the long run.

How to Stop B2B Fraud

Protecting your business from becoming the target of a fraudulent business is a multi-pronged approach that involves specialist tools, employee awareness training and clear procedures put in place.

Monitor your business partners and suppliers. When the times are good, as they were, there is less scrutiny because you don’t expect these relationships to turn sour but in a downturn, anything goes.

Obviously, massive B2B companies such as PSPs are affected more than your run-of-the-mill merchant, but the latter has a lot to lose as well. Hence the need to vet and monitor your partnerships closely.

- It all starts with raising awareness among business leaders. The always-online financial landscape offers an abundance of opportunities for fraudsters. Until those in charge of the firm recognize that no company is safe from B2B fraud, especially in difficult economic times, your business is a sitting duck.

- From there, risk management and risk monitoring procedures need to be expanded to also address this type of risk. Your stack should include solutions that provide intel into clients, suppliers and associates – not just customers.

- Part of this intel is a know your business (KYB) solution, which seeks to verify businesses. This can be automated or manual. Verification and background checks on business contacts are also useful.

- Certain workflows can make use of the more adaptable types of traditional fraud prevention tools, as B2B fraud techniques and indicators often overlap with more traditional flavors of fraud – for instance, the use of stolen credit card numbers.

- Make sure you stay abreast of sector-specific trends and adapt your fraud prevention strategy accordingly. An ecommerce marketplace operator may be targeted by different types of fraud than a logistics company, for instance.

Fraudulent Businesses, Targeting Businesses

The ease of setting up shop – or pretending to set up shop – and near-anonymous online communication have helped B2B fraud rise. The pandemic has demonstrated to criminals the endless possibilities. The fintech revolution has helped as well.

Early signs show that 2023 could be the year of B2B fraud.

The question is whether the B2B landscape, anti-fraud measures, and regulations are equipped well enough to deal with these – or will we face a similar meltdown to what we are seeing in the crypto landscape?

Sources

- Capital One: Three Ways to Prevent B2B Fraud

- Action Fraud: Short and Long Firm Fraud

- FinExtra: Three Types of Merchant Fraud: A Guide for Merchant Acquirers.

- United States Secret Service: U.S. Secret Service Returns $286M in Fraudulently Obtained Funds to the Small Business Administration