Financial criminals constantly evolve, employing advanced technologies and increasingly complex tactics to evade detection. Fraud insights gathered across onboarding, logins, monitoring and transactions hold immense value by revealing user intent. When siloed, however, these insights remain confined within fraud teams, missing the opportunity to enhance AML efforts. Key indicators – like understanding IP addresses from high-risk jurisdictions, device anomalies or atypical customer behaviors – often go unshared, limiting the potential to accelerate AML investigations and support regulatory reporting.

Fraud and money laundering are closely interlinked, with fraud serving as the precursor to laundering schemes. Yet, teams that address these issues traditionally operate in isolation with minimal knowledge or data-sharing. Integrating fraud data signals into AML workflows can grant teams a more comprehensive view of customer behavior, streamlining investigations, accelerating alert resolutions and strengthening compliance efforts. This united approach can equip organizations to address financial crime with greater efficiency, precision and cost-effectiveness.

A Unified Approach to Fraud and AML Investigations

To counter criminal networks, organizations must unify fraud detection with AML processes in a seamless, collaborative framework. Bridging silos offers three key advantages:

- Enhanced Risk Detection and Contextual Awareness: Integrating fraud insights into AML processes enriches investigations with contextual clues not visible from AML data alone. By connecting fraud indicators (e.g., IP anomalies or shared devices across accounts) with AML data, teams gain a clearer picture of user intent and suspicious patterns, improving accuracy and reducing false positives.

- Improved Collaboration and Transparency: When fraud and AML teams share a unified solution, collaboration becomes more intuitive. Both teams gain access to relevant data, streamlining the tracking of suspicious activities and facilitating communication on complex cases. This integration reduces blind spots, revealing hidden networks and risk factors that a fragmented system might overlook.

- Increased Efficiency and Cost Savings: Consolidating efforts within a single solution eliminates the need to switch between different systems, reducing the duplication of effort and data transfer issues. Visibility across fraud and AML data signals provides missing context for teams to identify and address risk faster, reducing investigation time and lowering compliance costs through increased productivity.

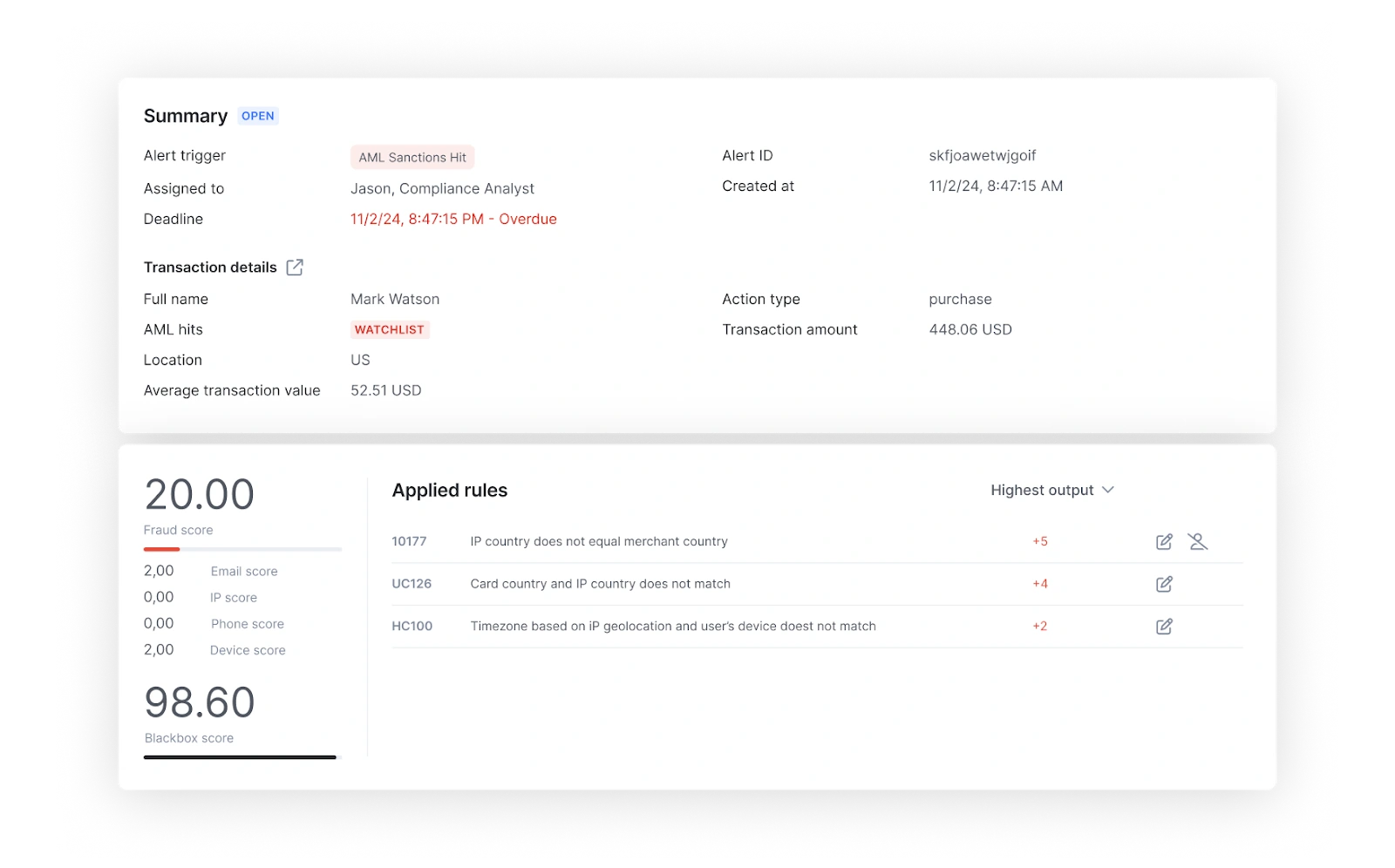

Filtering Out Fraudsters Before AML Screening: A Cost-Effective First Line of Defense

Before AML teams initiate screening, organizations should focus on blocking fraudsters from onboarding processes. Fraud detection tools that analyze digital footprints and device signals can spot suspicious users right from the start. Indicators such as the absence of a verifiable online presence, use of anonymizing browsers, email age, data breach exposure and suspect device configurations offer valuable insights into potential fraudsters.

By intercepting high-risk users early, businesses can avoid the costs associated with AML/KYC checks, preserving resources and maintaining customer base integrity. This proactive approach reduces the financial burden of managing high-risk users in AML workflows, allowing teams to focus on legitimate customers with reduced risk of costly remediation.

Key Fraud Insights for AML Teams

Fraud insights supply value across the entire compliance operations process – not just onboarding – enhancing AML efforts by delivering essential context for investigations. Here’s how specific fraud data signals support different stages of compliance:

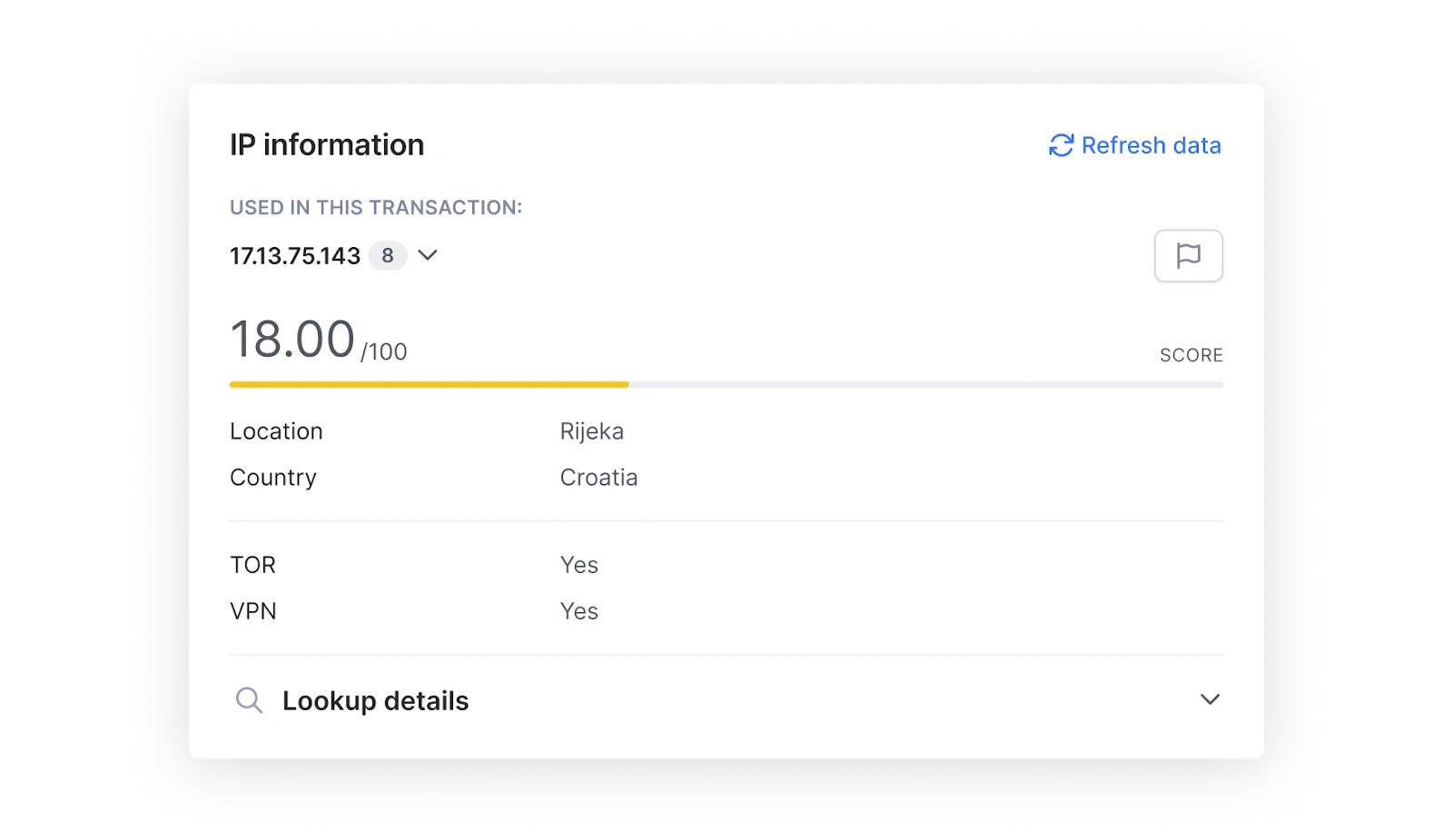

- IP Addresses

- Use Case: Onboarding, Payment Screening and Transaction Monitoring

Analyzing IP addresses helps identify users from restricted or high-risk jurisdictions. During onboarding, IP analysis prevents high-risk individuals from entering the system, while in payment screening and transaction monitoring, it flags unauthorized access and suspicious payment destinations, assisting in identifying potential money laundering routes.

- Use Case: Onboarding, Payment Screening and Transaction Monitoring

- Email Addresses & Phone Numbers

- Use Case: Onboarding

Email and phone number analysis can reveal synthetic identities or disposable contacts often used by fraudsters. Users with limited online presence linked to their contact details may be flagged as high-risk, as legitimate users typically have an established digital footprint.

- Use Case: Onboarding

- Email Age

- Use Case: Onboarding

Evaluating the age of an email account – through data breach records – provides a view into authenticity. Established emails with longer histories are generally considered more trustworthy, while newly created emails may indicate higher fraud risk, allowing teams to filter at the onboarding stage before users make it to AML screening.

- Use Case: Onboarding

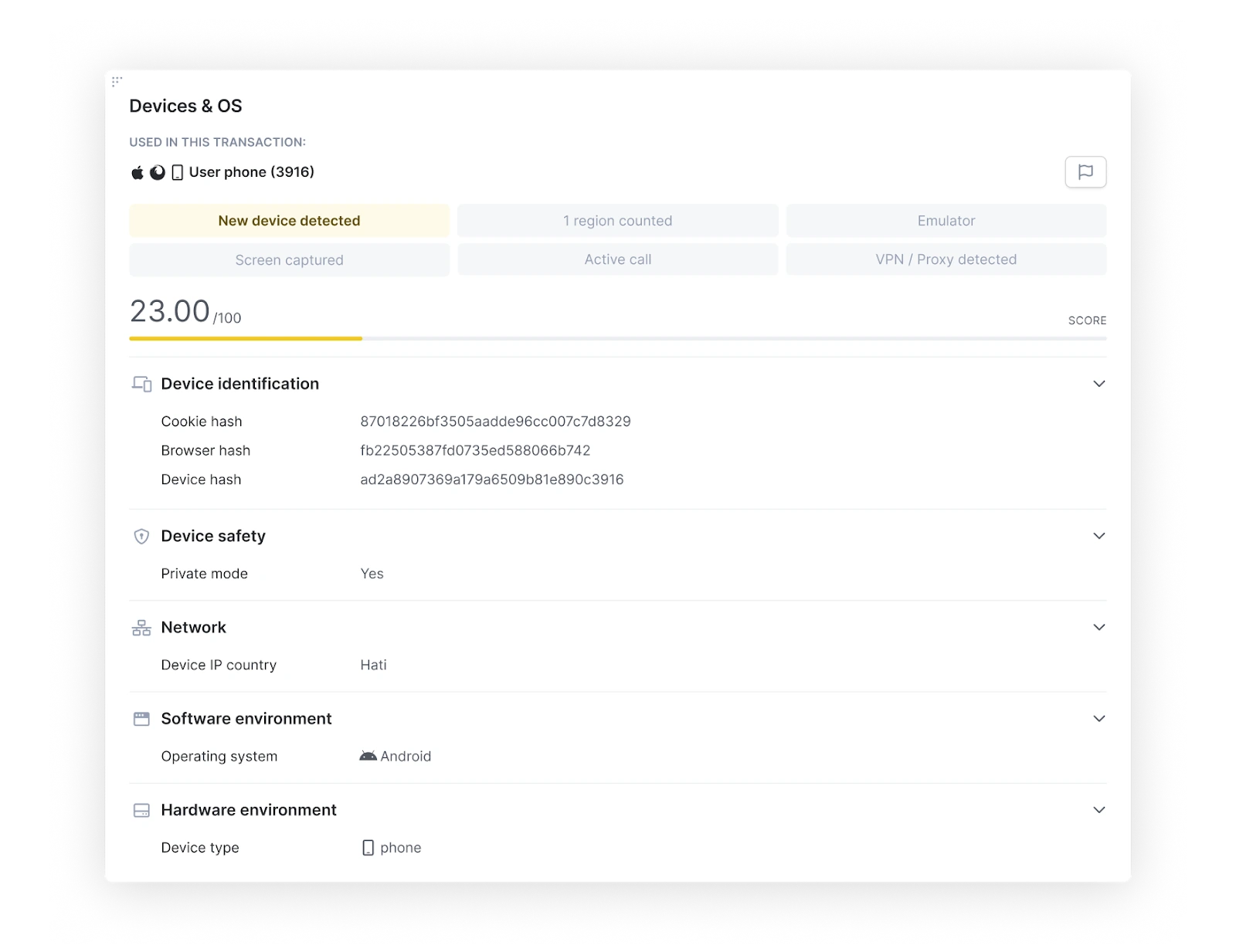

- Device Fingerprinting

- Use Case: Onboarding, Continuous Monitoring and Transaction Monitoring

Device fingerprinting detects suspicious configurations frequently associated with fraudulent behavior. During onboarding, this helps block fraudsters early. In continuous monitoring, it can flag repeated login attempts from unusual devices, signaling account takeovers, and during transaction monitoring, it aids in spotting anomalies in user behavior.

- Use Case: Onboarding, Continuous Monitoring and Transaction Monitoring

- Linked Accounts

- Use Case: Onboarding, Transaction Monitoring

Identifying shared devices and IPs across multiple accounts can uncover clusters of accounts involved in fraud or money laundering. This insight blocks high-risk networks at onboarding and flags interconnected accounts during transaction monitoring.

- Use Case: Onboarding, Transaction Monitoring

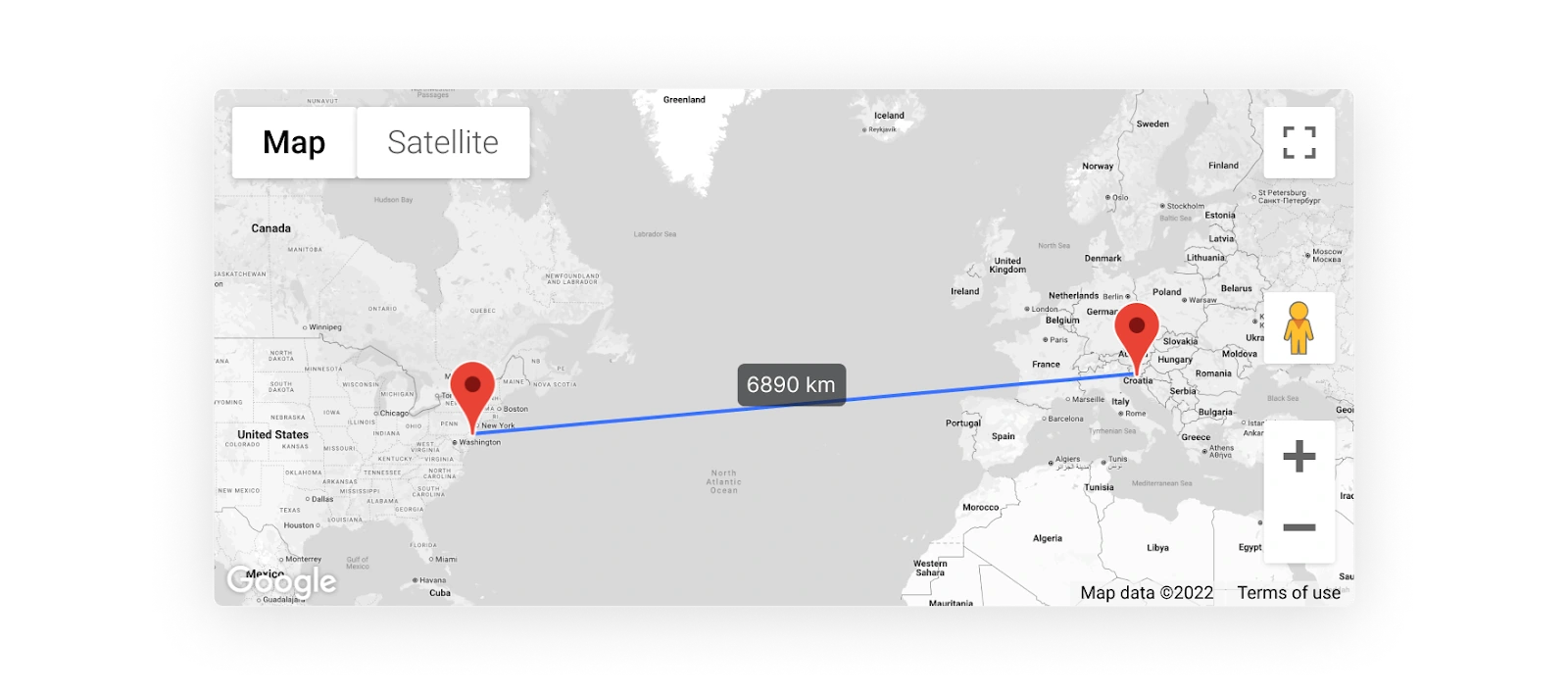

- Geographic Discrepancies

- Use Case: Payment Screening, Transaction Monitoring

Monitoring transaction locations for unexpected regions or high-risk geographies provides valuable information. Geographic discrepancies are red flags for unauthorized access or suspicious transfers, adding valuable context to payment screening and transaction monitoring efforts.

- Use Case: Payment Screening, Transaction Monitoring

- Credit Card Activity

- Use Case: Payment Screening, Transaction Monitoring

Changes in credit card usage patterns, such as switching cards after a decline, can indicate attempts to launder money. This is useful in payment screening to flag suspicious behaviors, and in transaction monitoring to track laundering tactics.

- Use Case: Payment Screening, Transaction Monitoring

- Behavioral Patterns

- Use Case: Continuous Monitoring, Transaction Monitoring

Monitoring behaviors, like repeated login attempts or device usage shifts, helps detect anomalies. Continuous monitoring identifies account takeovers, while transaction monitoring flags deviations that may signal fraud.

- Use Case: Continuous Monitoring, Transaction Monitoring

- Dynamic Risk Scoring

- Use Case: Continuous Monitoring, Transaction Monitoring

Real-time dynamic risk scoring assesses ongoing activities against historical data and user behavior to identify unusual patterns. This capability allows AML teams to respond swiftly to emerging threats.

- Use Case: Continuous Monitoring, Transaction Monitoring

Putting Fraud Insights into Action with Velocity Rules

To transform fraud insights into actionable monitoring, AML teams can implement velocity rules that track behavioral patterns over time. With the flexibility to specify up to two aggregates for comparison, velocity rules enable teams to monitor evolving patterns and respond quickly to shifting threats. This adaptable layer of security enables AML teams to stay proactive as risks evolve. Here are some example velocity rules that can help identify suspicious activities and enhance AML investigations:

- IP Addresses and Device Usage

- Example Velocity Rule: Set thresholds to monitor the frequency of IP address changes or device shifts within a defined timeframe. A velocity rule could flag accounts that change IP addresses multiple times in a single session or repeatedly switch devices. This configuration enables AML teams to detect patterns suggesting unauthorized access attempts or compromised accounts.

- Credit Card Changes

- Example Velocity Rule: Track the number of credit card changes within a specific period. If an account frequently switches cards after declines, it may indicate an attempt to evade detection or cycle funds. Velocity rules can flag such patterns in real time, allowing for swift investigation into potentially suspicious behavior.

- Behavioral Patterns

- Example Velocity Rule: Define thresholds for repeated login attempts, unexpected device changes or shifts in communication channels. By setting comparative thresholds with historical or peer group norms, AML teams can quickly identify unusual behaviors that signal account takeovers or fraudulent intent, enhancing the timeliness and relevance of alerts.

Each of these example velocity rules can be fine-tuned to suit specific compliance requirements and organizational risk tolerance. By applying dynamic thresholds, AML teams can move beyond static detection and achieve real-time, adaptive monitoring that proactively mitigates financial crime risks.

Resolve fraud and AML cases faster with SEON Case Management — automate workflows, collaborate easily, and streamline reporting with AI and filing tools.

Explore AML Case Management

Fraud Data for Faster, Accurate AML Investigations

Incorporating fraud insights into AML investigations supplies contextual data that can enhance decision-making and lead to faster and more efficient case resolution. Integrated data streamline compliance processes and control costs through:

- Automation: Automating the sharing of fraud knowledge with AML tools minimizes manual tasks, allowing teams to concentrate on high-risk cases requiring human oversight and discernment.

- Reduced False Positives: Cross-functional data sharing enriches AML investigations, lowering false positives and reducing unnecessary escalations.

- Comprehensive Audit Trails: A unified system provides traceable case documentation, supporting regulatory compliance and mitigating fines.

How SEON Enhances AML Investigations

SEON’s fraud and money laundering prevention solutions are designed for seamless integration with AML workflows, providing comprehensive view across onboarding to transaction monitoring.

- Early Fraud Detection: Identify risky behaviors during onboarding, blocking high-risk users from advancing to AML and KYC stages.

- Unified Fraud & AML Solution: Enables cross-team collaboration, using context-rich insights to improve efficiency and stay ahead of risks.

- Tailored Risk Strategies: Customizable rules, adjustable risk thresholds and adaptable data signals across geographies ensure compliance processes align with business needs.

- Simplified Reporting: AI-powered reporting simplifies regulatory submissions while providing secure recordkeeping and a full audit trail, reducing errors and saving time.

Building a Unified Defense

Bringing fraud insights into AML investigations and workflows equips teams to make faster, more informed risk decisions, streamline compliance and improve regulatory reporting. SEON’s solutions offer AML teams a comprehensive, data-driven approach to managing risks throughout the customer lifecycle.

Explore how our integrated fraud and AML solutions can enhance your compliance capabilities and support regulatory standards.

Speak with an Expert