The UK government is about to pull a very real lever on every UK‑licensed remote gambling operator: from 1 April 2026, the Remote Gaming Duty is moving from 21% to 40%.

This is a 100% increase in the tax rate on gross gaming yield — in other words, not a minor adjustment in a budget footnote. It is the industry’s biggest single cost shock in more than a decade, landing in a market where fraud had already been eroding margins.

In SEON’s 2026 Fraud & AML Leaders Survey of 1,000+ fraud, risk and compliance professionals, 57% of betting and gaming respondents said fraud losses were already outpacing revenue before the tax change was announced. On the surface, brands have been reporting strong top‑line growth. Underneath, fraud and financial crime have been quietly catching up.

Here are the top considerations for operators who need to adapt to this change.

Growth is Soaring, Which Means Fraud Rates Do Too

The growth engine is still running hot. According to the same research, 99% of betting and gaming operators plan to launch a new product or enter a new market in 2026, and nearly half saw revenue climb by more than 26% over the past year. New brands, game formats and jurisdictions, backed by aggressive promotions, remain the standard way to defend market share.

That same playbook is also what today’s fraud problem feeds on.

Three categories dominate the loss profile: bonus abuse, loyalty fraud and account takeover. Together, they account for 68% of reported fraud in betting and gaming. Each one is tightly connected to how operators drive both acquisition and retention.

On the acquisition side, generous welcome and reload offers invite synthetic identities and multi‑accounting. If you are rewarding every “new” player aggressively, you are also rewarding the fraudsters who are best at looking new on repeat. On the retention side, rich loyalty and VIP schemes make existing accounts more valuable targets. In addition to creating new profiles, fraudsters also look for ways into trusted, aging accounts so they can harvest bonuses and rewards that the operator has already earmarked for genuine players.

The more operators do to accelerate growth and deepen retention, the more surface area they expose to this kind of abuse. The same levers used to push revenue up are also expanding the attack surface fraud teams must defend.

Inefficiencies Such as Fragmented Stacks and Manual Fixes Don’t Scale

Underneath the loss figures sits a foundational problem in how systems are wired together. Betting and gaming operators are almost four times more likely than peers in other industries to describe creating a unified customer view as “extremely challenging.”

Data silos run well above the cross‑vertical baseline, and identity workflows are often split between multiple providers with incompatible data models. Fraud prevention, AML monitoring and IDV are often handled under separate contracts and integrations, each with its own events, rules and reporting.

Given this architecture, what happens when pressure hits is rarely a surprise. Instead of fixing the foundation, many operators simply add more people around the edges. The Fraud Survey shows that betting and gaming operators invest significantly more budget in analyst headcount and significantly less in AI and automation than other verticals — making it the only sector where spending on people surpasses spending on automation.

When fraud spikes or a new product launches, the first move is to expand manual review teams and plug gaps between tools with human effort. The extra headcount creates the sense that the issue is under control, so the organisation leans back into the same growth tactics: more offers, more markets, more volume through the same fragmented stack.

But this approach has a structural limit: human capacity increases one case at a time, whereas fraud grows on a curve that hiring plans cannot keep pace with. High false‑positive rates compound the problem, pushing more legitimate players into already long queues and inflating costs without a corresponding improvement in control.

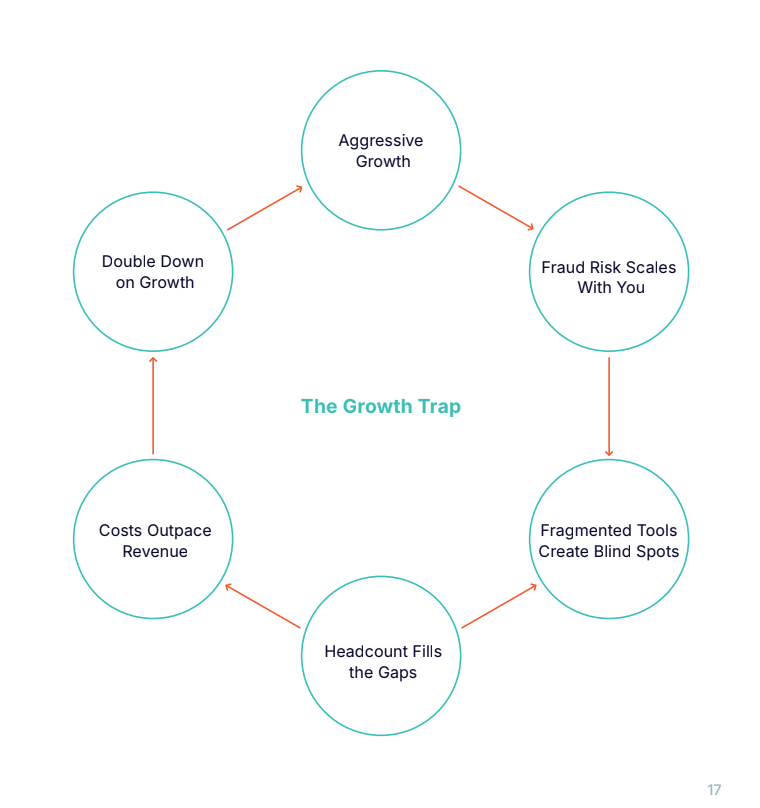

Over time, the pattern gets more entrenched: ambitious growth creates more fraud, fragmented tools miss signals, hiring more people masks the strain just long enough to fuel the next round of growth — and the cycle repeats at a higher cost base each time.

What Leading Operators Are Doing to Adapt

The Remote Gaming Duty increase didn’t start this pattern, but it transforms these challenges from expensive into unsustainable. Under a doubled tax rate, every extra analyst, every redundant vendor contract and every player lost at a broken verification step consumes a larger share of the value generated by each bet.

What once felt like an expensive, slightly messy way of working is now a direct threat to the business model.

This is why the industry’s attention is shifting from individual point solutions to an architecture that connects them. The operators best placed to defend their margins in the coming years will be those who break the cycle by consolidating their risk stack. In practical terms, this means bringing fraud, AML and IDV together in a single platform: one integration, one data pipeline and one view of each player.

When fraud signals feed directly into AML decisions, plus IDV flows are informed by digital footprint data and device intelligence before a document is requested, the economics change. Detection sharpens, and the dead weight of redundant manual work, along with its cost, finally starts to lift.

Timing matters. Multi‑year contracts are being negotiated now as the AML and risk technology market consolidates around a smaller number of platforms. Leveraging a cluster of standalone tools today effectively locks in fragmentation and costs for the duration of those agreements.

Choosing a unified platform instead is a way of building in flexibility: controls can be adjusted centrally, automation can expand as operators gain confidence, and scarce human expertise can be deployed where it genuinely adds value.

What Survives When the Dust Settles

The old pattern of fragmented tools and ever‑larger manual teams is no longer something operators can grow their way out of. SEON is built to offer a different route. Instead of adding another point solution to an already crowded stack, it brings fraud, AML and IDV into a single environment where every signal can inform every decision. The same controls that keep acquisition fast can harden high‑risk journeys, and the same data powering fraud decisions can sharpen AML alerts without adding friction.

In a market where duty has doubled, and fraud was already eroding margins, consolidation stops being a tidy efficiency play and becomes one of the last real levers left to protect profitability.

Turn Tax Pressure Into a Fraud Advantage

SEON’s 2026 Betting & Gaming Fraud & AML Report dives into how operators are reshaping fraud, AML and IDV this year — and where consolidation is already turning rising costs into better margins and stronger controls.