Lenders serving thin-file or underbanked customers face a straightforward problem: traditional credit data doesn’t exist for a significant portion of the global population. Social media scoring is one way to close the gap.

According to the World Bank’s Global Findex 2025 report, 1.3 billion adults worldwide still lack access to formal financial services. For fintech lenders and digital banks expanding into new markets, this represents both a growth opportunity and a data challenge.

Social data, including digital footprint signals from registered profiles, activity patterns and platform presence give risk teams an additional layer of signals where bureau data falls short. That matters more than ever: according to SEON’s 2026 Fraud & AML Leaders Report, the share of leaders who believe fraud losses are outpacing revenue nearly doubled year over year.

What Is Social Media Credit Scoring?

Social media credit scoring uses digital footprint data to assess the creditworthiness of a loan applicant. Rather than relying solely on bureau data, lenders analyze signals from registered social profiles, platform activity and network reputation to build a fuller picture of borrower behavior.

It sits within the broader category of alternative data for credit scoring — data sources that supplement or replace traditional credit signals for populations with thin or no bureau files. Beyond lending, alternative data also appears in digital onboarding, financial product eligibility and affordability assessments.

Social data is not a standalone underwriting input. The most defensible implementations layer it alongside identity verification, device signals and transactional data, using social presence as one corroborating signal rather than a primary risk driver.

See how SEON’s social media profiling helps FairMoney offer 10,000 loans daily, fast and with reduced risk.

Learn How

How Does Social Media Credit Scoring Work?

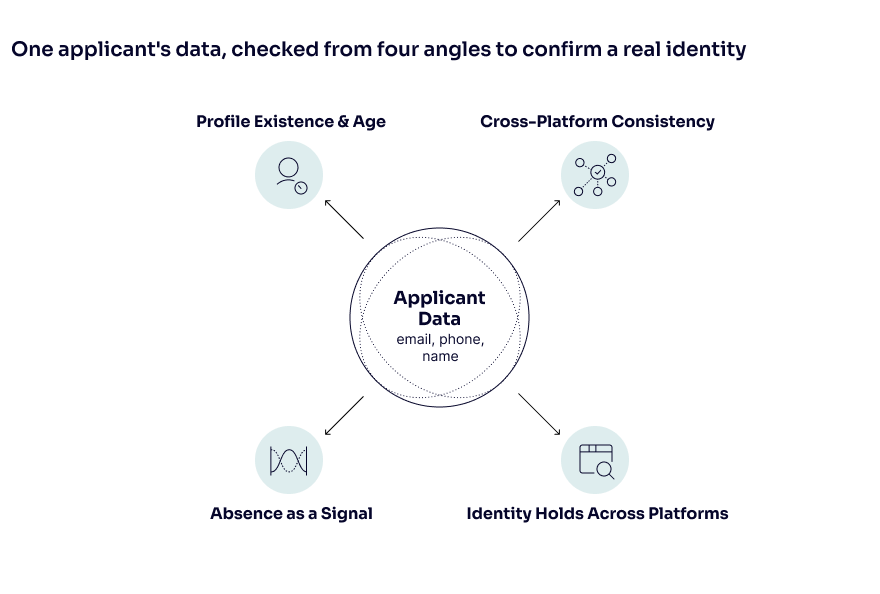

Social media credit scoring works by enriching standard onboarding data like an email address, phone number or name against digital and social platforms to verify that a consistent, organic identity exists behind the application. The goal isn’t to analyse someone’s posts or opinions; it’s to check whether a real, active digital presence corroborates what the applicant declared.

In practice, this involves several interconnected checks:

- Profile existence and account age: Does a profile exist across platforms like LinkedIn, Facebook or Instagram and how long has it been active? Account longevity carries more weight than which platforms someone uses.

- Cross-platform consistency: Does the name, location and employment data across platforms match the application? A LinkedIn profile that conflicts with a stated income bracket or a Facebook account registered in a different country to the applicant’s declared address are both worth flagging. Absence of social presence as a signal: No LinkedIn, no Facebook, no Instagram and no traceable social history is itself a red flag, since fraudulent or synthetic identities rarely carry the kind of platform history real people build up organically.

- Platform choice versus behavioral signals: Weighting someone negatively for using TikTok over LinkedIn carries discriminatory risk. The stronger signal is whether their identity holds up consistently across whichever platforms they do use.

The Pros and Cons of Social Media Credit Scoring

Social media platforms have previously attempted to build their own credit scoring models from user data, and the backlash shaped how the industry thinks about this today. The more defensible approach is gathering open-source social signals as part of a broader digital footprint analysis, layered alongside other risk inputs.

Pros

- Real-time coverage for thin-file applicants: Social data is available in real time and doesn’t depend on bureau history. For BNPL providers, payday lenders or any operator expanding into underbanked markets, it fills a gap that traditional data can’t.

- A strong fraud signal: A complete absence of social presence is itself a signal. Synthetic identities and fabricated personas rarely carry the organic digital footprint of a real person, making social data a useful check during onboarding.

Cons:

- Inconsistent data quality: Social platforms don’t offer APIs for credit-relevant data, so gathering it at scale requires third-party tooling. Coverage varies significantly by market and platform — and because profiles are self-reported, false signal risk runs in both directions.

- Discriminatory outcome risk: Research has flagged that social data can encode demographic proxies, and there are documented cases of it being used to target financially vulnerable applicants. Any implementation needs to account for this before deployment.

- Regulatory and privacy exposure: Data minimization requirements under GDPR and fair lending constraints in other jurisdictions limit what can be collected, retained and used in a credit decision. Compliance posture matters before deployment, not after.

SEON’s digital footprint analysis helps lenders assess thin-file applicants, detect synthetic identities, and improve underwriting with real-time online presence data.

Speak with an Expert

How to Use Social Media for Credit Scoring

Social media scoring works as a structured enrichment layer: one input in a broader risk assessment, applied systematically across collection, cross-referencing and interpretation. Here’s how it works in practice.

Collect Digital Footprint Data

Data collection starts with checking whether a social profile exists, when it was created, how active it is and whether the details match the loan application. Software can flag high-risk customers by aggregating signals across professional profiles, social networks and email-to-platform matches. Account age and activity patterns matter as much as the content itself. No single signal is conclusive — the value comes from the full picture across sources.

Cross-Reference Against Application Data

Discrepancies between declared information and digital footprint data are among the most actionable signals in this process. A UK mortgage application from someone whose social activity is concentrated in another country, or a LinkedIn profile that conflicts with declared income, both warrant closer review.

Customer segmentation adds another dimension here. Social data helps validate whether an applicant’s profile is consistent with their declared market, income band or geography — a useful check that goes beyond what self-reported data alone can provide.

Treat Absence as a Signal

A completely absent digital footprint should increase risk weight in the scoring model. Synthetic identities rarely carry the organic online history of a real person: no registered profiles, no activity and no platform presence removes a layer of corroboration that legitimate applicants build up naturally over time.

Account age is equally relevant. A full set of profiles created days before a loan application reads differently from accounts with years of consistent activity.

Weight Signals, Not Platforms

Assigning reputational value to specific platforms (like treating a GitHub profile as more creditworthy than a Facebook one) carries discriminatory risk and has attracted regulatory scrutiny. The sounder methodology weights behavioral signals: identity consistency across platforms, account longevity and data matching accuracy. These are more legally defensible and operationally reliable than judgments based on platform choice.

Ensure Compliance Before Deployment

GDPR data minimization principles constrain what can be collected and retained in Europe. Fair lending laws in the US restrict the use of proxies that correlate with protected characteristics. Risk teams need to demonstrate what data was used, how it was weighted and that decision logic produces consistent outcomes across applicant groups.

The practical baseline is ensuring the anti-fraud platform is GDPR compliant and fully auditable. Compliance built into the implementation from day one is considerably less costly than addressing it after a model is in production.

How SEON Leverages Social Signals

For lenders assessing thin-file or underbanked applicants, the quality of social data depends entirely on how it’s sourced. SEON enriches email addresses, phone numbers and IP addresses against 300+ digital and social platforms in real time, aggregating 900+ proprietary signals at the moment of the request — not from resold, stale third-party databases.

The distinction matters for credit decisioning: signals are current, directly sourced and explainable, giving underwriting teams a defensible view of every applicant’s digital footprint from the first interaction. With five billion fraud checks processed annually across fintech, lending and payments, the enrichment layer is built for the data volumes and regulatory scrutiny that lenders actually operate under.

The output is a complete social and digital risk profile delivered through a single API — no additional forms, no friction added to the onboarding flow.

FAQ

Lenders analyze signals from registered social profiles, account age and activity patterns, email-to-platform matches and professional profile data. The most useful inputs are consistency across platforms and discrepancies between social data and application details.

It depends on jurisdiction and implementation. GDPR data minimization principles constrain collection and retention in Europe, while fair lending laws in the US restrict the use of proxies that correlate with protected characteristics. The legal baseline is using an auditable, GDPR-compliant platform and being able to demonstrate how every signal was weighted in a credit decision.

Yes — that’s its primary use case. For thin-file and unbanked applicants, bureau data is limited or absent. Social and digital footprint signals give lenders a corroborating layer that doesn’t depend on prior credit activity, making it particularly valuable for fintech lenders and digital banks expanding into underserved markets.

Sources