What Is Chargeback Recovery?

Chargeback recovery or chargeback representment is when a merchant asks for a chargeback to be repaid (or recovered). Following investigation, the chargeback recovery request is then either approved or reversed.

When a merchant believes a consumer’s chargeback request is incorrect, unfair, or fraudulent, and could constitute chargeback abuse, they are likely to attempt to recover the chargeback.

In simple terms, a chargeback is when a card issuer, acting on behalf of a customer, asks a merchant for money back for a disputed or fraudulent transaction. This measure is in place as a failsafe to protect consumers, but it can be abused through friendly fraud, scams and beyond. In fact, industry insiders estimate that 61% of all chargebacks in North America will be cases of friendly fraud by 2023.

And chargeback fraud overall is by far one of the top pain points for merchants in the 21st century.

Though merchants are eager to keep shoppers happy and earn return custom, it is understandable to want to push back against requests that take unfair and disproportionate advantage of the system.

This is when chargeback recovery comes in to help.

Proactiveness goes a long way. We dive into the problem of chargeback fraud, why it happens, and what you should do to solve it.

Learn More

How Does Chargeback Recovery Work?

For chargeback recovery, a merchant will respond to a chargeback request with evidence that both the goods/services purchased were up to par and that they were delivered as promised to the customer, in the hopes of demonstrating they did everything by the book and thus the chargeback request is not legitimate.

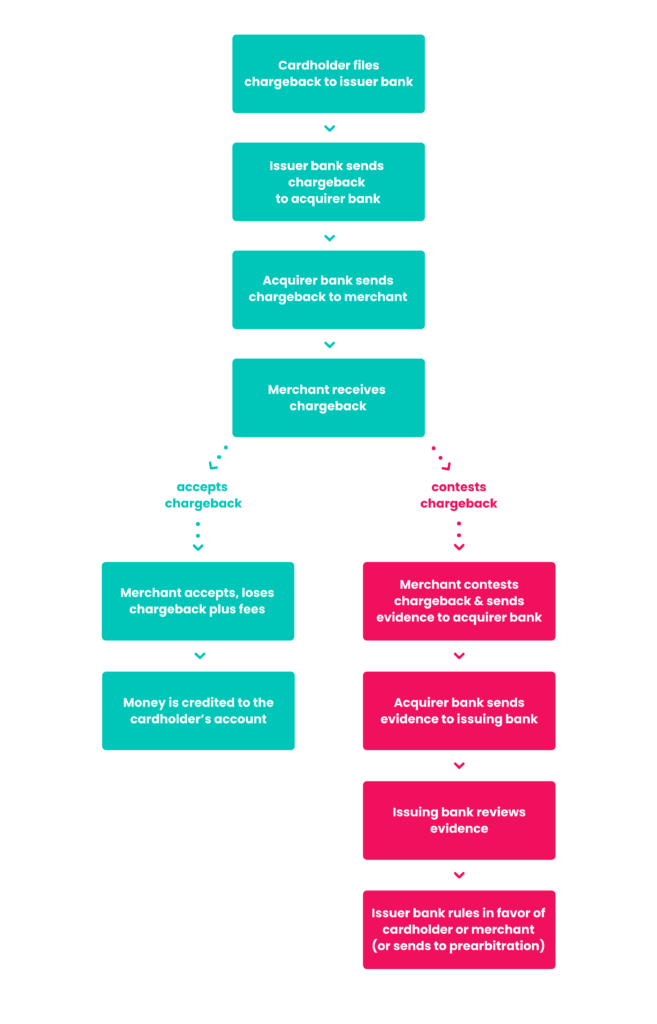

- Following a charge, a cardholder files a chargeback request with the card issuing bank.

- The issuing bank sends a request to the acquiring bank.

- The acquiring bank informs the merchant, requesting the money back.

- The merchant can either…

- accept the chargeback, refund the money plus pay fees. This ends the process, OR

- contest the chargeback.

- If the merchant disagrees and chooses to attempt chargeback recovery, they need to:

- Collect any and all evidence to support their claim that…

- the order was legitimate

- there was no reason to suspect fraud or stolen credentials

- the item was as described and expected

- the item was shipped

- the item was delivered to the buyer

- Send all this evidence to the acquiring bank.

- Collect any and all evidence to support their claim that…

- The acquiring bank forwards the evidence to the card issuer bank.

- The bank reaches a verdict, which can be:

- In favor of the cardholder – so the merchant needs to pay up.

- In favor of the merchant – the cardholder receives no money.

- Unclear – forwarded for arbitration/second chargeback.

Chargeback guarantees are provided for payments with several types of payment cards, including well-known credit cards such as American Express, Visa and Mastercard, debit cards from the above and other brands as well as certain types of prepaid cards – namely those by Visa and Mastercard.

Digital wallets such as PayPal sometimes have similar processes in place, although they are not as clear-cut as the former.

Who Abuses Chargebacks?

Chargebacks can be accidentally abused by legitimate buyers (friendly fraud) or taken advantage of by opportunistic shoppers (first-party fraud).

Of course, chargebacks can also be caused by merchant error, but those are normally not disputed and often never filed, as the merchant will settle this directly with the customer.

Chargebacks can also be the result of malicious activity by fraudsters and groups of fraudsters (when card data is stolen, for example). Though this negatively affects the merchant, it does not constitute chargeback abuse whatsoever – but merchants ought to still do their best to prevent it, to avoid bearing the brunt.

Depending on how and why a chargeback request has been filed, there are several things a merchant can and cannot do to dispute it – or rather different strategies that might work.

The most common selling point for chargeback recovery services is their promise to put an end to chargeback fraud and INR (item not received) fraud. Some say they will also help with cancellations, item-not-received claims, and processing errors as well, all providing different levels of guarantees.

How Bad Is Chargeback Abuse?

A successful chargeback request is more than a simple refund. Each case is estimated to cost merchants 2.40x to 3.60x the money lost in the disputed transaction.

Card issuer Mastercard projects global chargeback volume in 2021 to reach an astounding USD 615 million.

Though some total loss estimates are lower, the message is loud and clear that there’s much more involved than straightforward monetary loss. Merchants ought to remember that chargeback abuse costs businesses much more than the price of the item refunded.

Additional concerns include:

- chargeback fee imposed by the bank for handling the dispute

- loss of stock

- higher chargeback ratio, which can affect your partnership with payment networks

- increased fees and bans

- time and effort in dealing with chargebacks

- loss of employee morale

What’s Required for Chargeback Recovery?

Chargeback recovery requirements include as much detail, evidence, and documentation as possible so that the merchant can prove they did everything by the book and delivered the item or service described without any issues.

Documents and tools that are helpful for chargeback disputes include:

- all communication with the customer

- invoice, receipt of payment

- proof of shipping and proof of delivery – signed, if possible

- customer payment history (if they have a buyer account with you)

- all information you have about the customer’s shopping session, including IP address, device type, time taken from login to checkout, etc.

- any profiling you have of the buyer, including digital footprint results from SEON

- a letter breaking down the incident in simple, concise terms, and arguing your point against the chargeback as objectively as possible

- any additional documentation and evidence related to the case

The latter point is a very wide-ranging one and depends on the reasoning argued by the consumer.

For example, if the cardholder claims they have been charged for an item they never bought nor received, you could look at social media to see whether the recipient and cardholder are connected in any way. If they are, they could be trying to scam you together. Keep records of this evidence and include it in your submission.

What Are Chargeback Recovery Services?

Chargeback recovery companies provide help to those in the ecommerce sector looking to submit chargeback dispute claims.

They will either provide a digital platform to help streamline the process, featuring tools for you to prepare and submit your chargeback recovery, or even prepare and file the dispute on your behalf.

Chargeback management software and tools promise to help source and submit all the necessary documentation to make your chargeback recovery claim. This includes checklists, direct lines of contact to issuer banks, resolution letter templates, reconnaissance and more.

A related service you might see advertised is the chargeback guarantee model. It does seem an attractive proposal: The anti-fraud vendor is so confident in their work that they promise to pay on your behalf if some chargebacks do incur.

However, consider what this means for your customers. Because the vendor is so invested in minimizing all instances of chargebacks, they are likely to err on the side of caution – which means they will likely reject payments and users in an overzealous manner, at the risk of leaving your legitimate buyers unhappy due to false positives or false declines.

This model, though, can work for some merchants, subject to their size, risk appetite and sector.

Chargeback Prevention Strategies

Although chargeback recovery attempts can work, the most efficient and cost-effective method is to try and prevent chargebacks in the first place, especially when doing so means protecting one’s eshop from several other types of fraud as well.

Many merchants have accepted chargebacks as part and parcel of operating online, and something to deal with on a case-by-case basis when it does arise.

In fact, most merchants choose to walk on the razor’s edge when it comes to the card networks’ chargeback limits for their locale, in order to maximize their revenue. The idea is they’ll suffer more chargebacks in order not to miss out on sales.

But this is a false dichotomy. Chargeback prevention strategies can go a long way in preventing the need to deal with tedious chargeback dispute procedures that take up time and resources without any guarantee of success – as well as outright chargebacks.

In fact, according to Mastercard estimates from 2020, approximately 1 in 4 chargeback disputes could have been prevented simply by having merchants be clearer when charging the payment card.

Some anti-chargeback steps merchants can take at next to zero cost include:

- having customer service readily available for buyers to approach with any requests (thus avoiding the need to turn to their bank)

- being thorough in your descriptions of products and services sold

- only charging a payment card after shipping

- using Strong Customer Authentication (SCA)

- being actively courteous and responsive to customers

- ensuring your charges are recognizable on statements

- keeping a paper trail for all actions, including shipping, orders, etc.

From there, one can look into the next level of prevention. For instance, making use of the card issuer’s address verification service, only shipping to addresses that match the cardholder’s address, rejecting orders from high-risk locales and so on – or even implementing more sophisticated solutions.

Being proactive and vigilant in the face of possible chargebacks is a no-brainer, once you know the potential returns.

One of SEON’s clients, a VPN provider, saw its chargeback rate reduced by 91% within 30 days after deploying the anti-fraud platform.

Another case study involves a crypto exchange who reduced its chargebacks to zero within twelve months, as well as decreasing the required time for manual review to just one minute each.

Through techniques such as data enrichment, BIN checks, device fingerprinting, behavior analysis, machine learning and risk-scoring, an ecommerce business can prevent instances of fraud, inclusive of chargebacks, in the first place.

Sources

- The Paypers: What is the relationship between chargebacks and SCA? It’s complicated

- Mastercard: Mastercard Delivers Greater Transparency in Digital Banking Applications

- Chargebacks911: Chargeback Stats