As businesses operate in an increasingly interconnected digital global landscape, combating fraud has become more urgent, complex and increasingly intertwined across company departments. What typically sat under legal’ purview for risk and compliance is now becoming an issue that permeates all aspects of business functionality, including product, marketing and customer success. Today, fighting fraud is a team sport.

With worldwide fraud costs topping $5.13 trillion each year, climbing a steady 56 percent over the last decade, much of its growth is attributable to long-term social and technological factors and the effects of economic cycles. On average, businesses lose five percent of their annual revenues to fraud – but this is just the tip of the iceberg. Fraudsters and cybercriminals are ramping up, leveraging advanced techniques to exploit digital infrastructure vulnerabilities and amplifying businesses’ susceptibility across sectors.

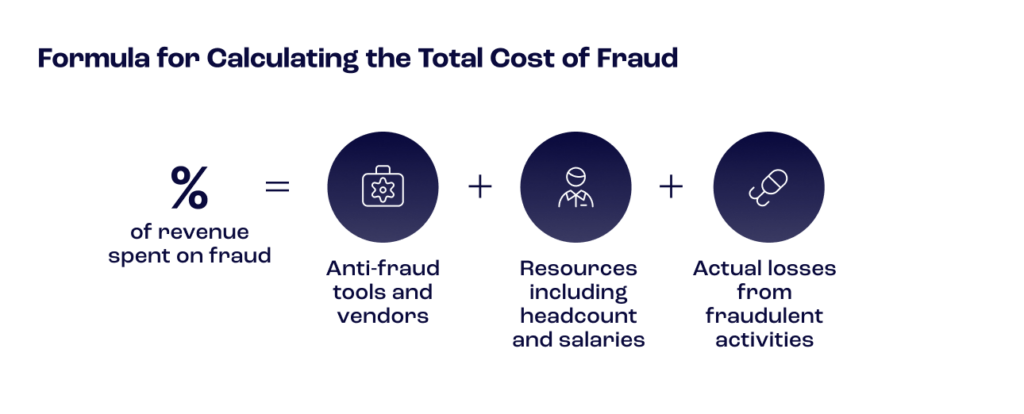

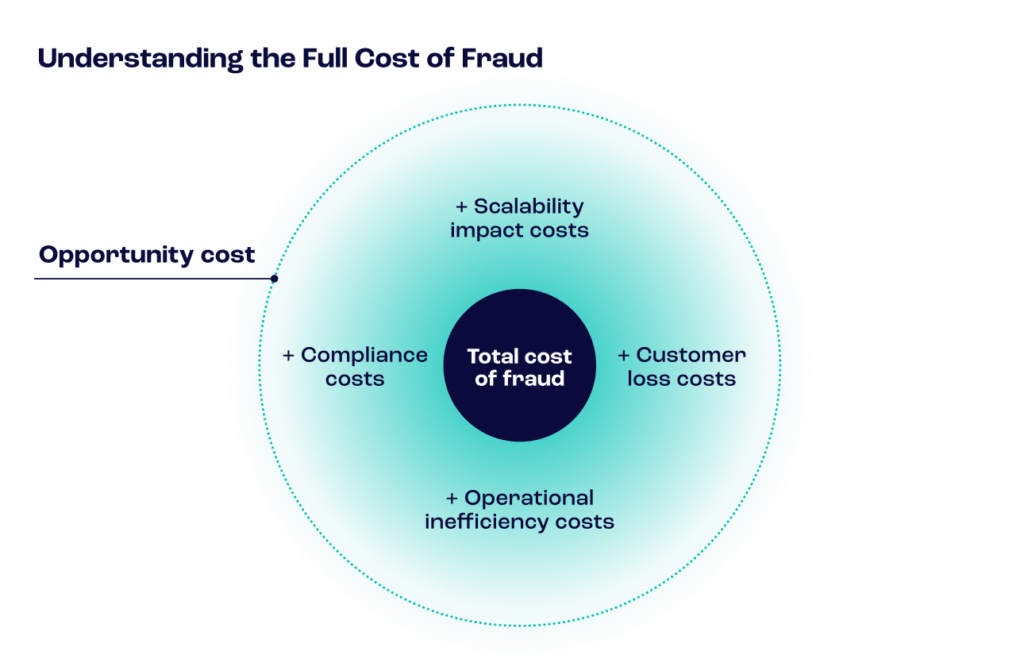

Traditionally, calculating the total cost of fraud relies on the percentage of revenue spent on fraud every month, including tools and vendors, resources such as headcount and salaries, and the actual losses from fraudulent activities. However, fraud’s ripple effect on opportunity costs can exponentially serve as a detriment to a company’s bottom line.

Focusing too narrowly on financial losses fails to accurately reflect fraud’s full consequences, which can impact core pillars, such as operational efficiencies, compliance, customer experience and scalability. Amid escalating risks and accumulating cost burdens, companies must thoroughly evaluate their evolving fraud exposure, including fraud’s wide-reaching ramifications across their business – to truly understand the total opportunity cost lost to fraud.

Factoring in ‘Soft’ Costs of Fraud

Fraud’s indirect consequences can jeopardize business success. These soft costs, which are harder to quantify in numbers, exacerbate and expand fraud’s cost footprint. Highlighting the more significant knock-on effect beyond direct losses contributes to understanding the total actual cost of fraud and the broader implications.

Operational Inefficiencies

Instances of fraud often trigger a chain reaction of operational inefficiencies, marked by labor-intensive manual reviews conducted by sizable teams of fraud analysts. These processes not only incur substantial labor costs but also introduce operational bottlenecks. While some market solutions integrate machine learning (ML), artificial intelligence (AI), and automation to streamline review processes and minimize reliance on manual intervention, many businesses operate with fragmented workflows, where separate departments are isolated, leading to gaps and weaknesses.

As fraudulent activities escalate in complexity and volume, companies allocate a significant workforce to sift through transactions, verify identities and flag suspicious behavior. Each manual review represents an expenditure of time and human capital and a delay in processing legitimate transactions, potentially souring customer experiences and impeding revenue streams. With analysts bogged down in repetitive tasks, critical alerts might go unnoticed or unresolved, exposing vulnerabilities and allowing fraudulent activities to persist unchecked.

The advancements in AI, ML and automation transform fraud detection and protection by augmenting human capabilities with algorithmic precision and scalability. By deploying sophisticated algorithms to analyze vast datasets in real-time, businesses can swiftly identify patterns indicative of fraudulent behavior, flagging suspicious transactions for further scrutiny while minimizing false positives. By adopting a holistic approach to fraud detection and fostering cross-departmental collaboration, businesses can transcend operational inefficiencies, unlocking new levels of agility, accuracy and scalability in combating fraud.

Loss of Customers

Balancing anti-fraud measures with seamless customer experience is critical to prevent attrition, preserve brand loyalty and uphold customer success. Influenced by the predictive experiences offered by behemoths like Amazon, Netflix and YouTube, customers now anticipate that companies will detect and address potential fraud incidents even before they become aware of them. Fraud’s impact resonates deeply within customer interactions, especially during transactions, where prolonged fraud checks increase inconvenience. Further, fraudulent events compound the issue and increase customer dissatisfaction. Research shows that after the event of a data breach, companies saw up to a seven percent increase in customer churn.

In the competitive landscape of modern commerce, customer experience reigns supreme, and each interaction shapes brand perception, influences purchase decisions and informs long-term loyalty. When fraud itself or the mechanisms to disrupt fraud disrupt the flow of transactions, customers bear the brunt of inconvenience. Lengthy verification processes, additional security checks and delayed approvals contribute to suboptimal experience. With speed and convenience paramount, every moment of friction increases the likelihood of abandonment – especially in competitive markets – as customers seek out alternative providers offering smoother transactions or experiences. When legitimate transactions are erroneously flagged as fraudulent, customers experience the inconvenience of delayed approvals and the indignity of suspicion. Such instances erode trust and undermine the perceived reliability of a company’s fraud detection systems.

The repercussions extend beyond individual transactions to broader brand trustworthiness and reliability perceptions. In the aftermath of a data breach or security incident, customers exhibit heightened sensitivity to potential risks, scrutinizing the company’s response and weighing the adequacy of its safeguards. Any perception of negligence or indifference can cause irreparable damage to the brand’s reputation. By leveraging advanced technologies, companies can preemptively identify and mitigate potential threats, safeguarding transactions and protecting customer activities without imposing undue burdens on customers.

Costs Associated with Compliance

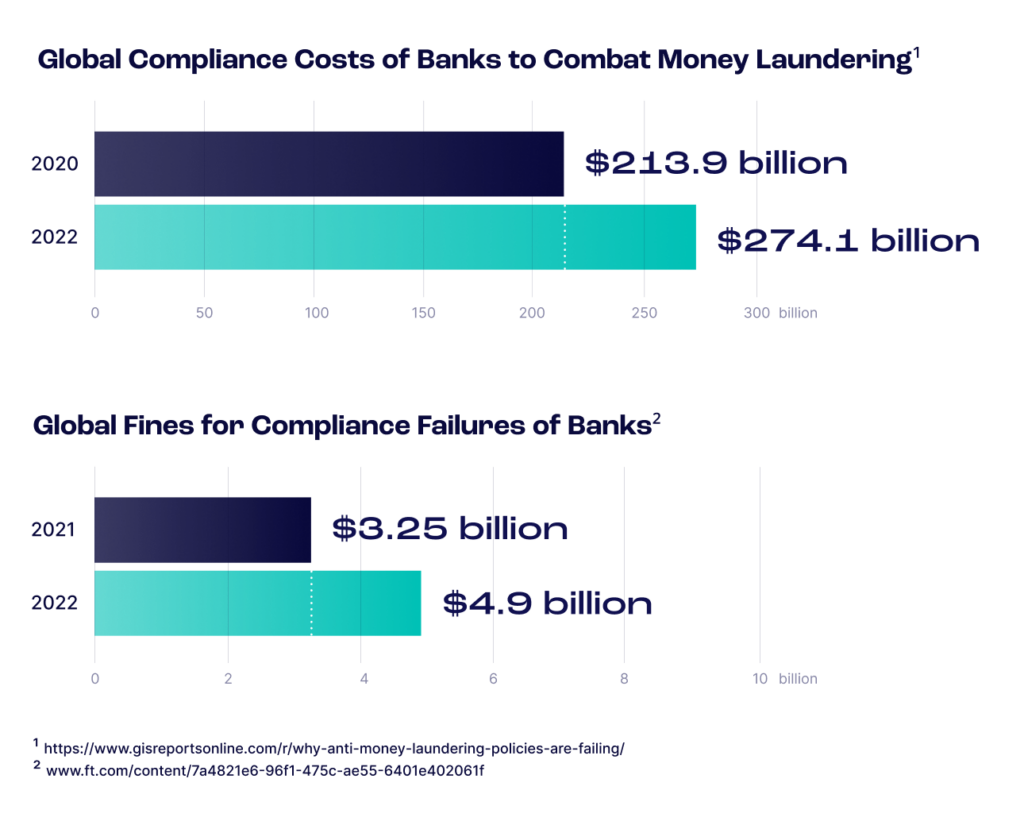

Fraud and anti-money laundering compliance costs have been rising sharply, driven by factors like new regulations, evolving financial crimes and the need for enhanced due diligence and monitoring capabilities. Globally, the total expenditure of financial crime compliance surged to approximately $274 billion in 2022. Today, companies and financial institutions face heightened vulnerability to illicit activities linked to real-time digital payments, profits from trafficking and trade-based money laundering schemes. And many are operating on tight budgets, with less than 5% of Thomson Reuters’ survey respondents citing that their budgets would increase for the next year. Managing the cost of AML compliance has become a growing concern for organizations balancing risks with limited resources.

Amid this escalating regulatory environment – with the volume of regulatory changes dominating the list of compliance challenges – the issue of managing cost pressures while concurrently fulfilling competitive and compliance imperatives looms large. However, despite the glaring necessity to keep a vigilant eye on expenditure, 45% of survey respondents admitted to a lack of comprehensive monitoring of compliance costs across their organizations. Another one-third of respondents said they expected compliance teams to grow, and the overall cost of compliance staff was expected to increase despite staff turnover and budgets remaining at 2022 levels.

The expenses entailed in upholding compliance standards extend far beyond the mere implementation of regulatory frameworks, encompassing a multifaceted spectrum of financial outlays, each bearing its own set of implications for organizational viability and reputation. Foremost among these costs are regulatory fines, which serve as punitive measures meted out by governing bodies in response to lapses in compliance adherence. In 2023, global AML fines reached beyond $5.8 billion for crypto and fintech groups, with the total for banks lower at $835 million. These fines take a tangible toll on financial resources and carry intangible repercussions in the form of reputational damage and erosion of stakeholder trust.

In addition to the financial burdens, compliance operations face significant hurdles in regulatory reporting, customer risk assessment and digital identity authentication. The convergence of these obstacles, compounded by the heightened risks of financial crime, is exerting a profound impact on various facets of business operations.

Meanwhile, due diligence timelines are stretched thin as organizations grapple with verifying customer identities and assessing risk profiles in an increasingly digital and interconnected world. Moreover, the challenges associated with digital identity authentication add a layer of complexity, requiring sophisticated technological solutions and robust security measures. From deploying fraud detection solutions to conducting thorough investigations into suspicious activities, organizations must allocate substantial resources to safeguarding their assets and mitigating potential risks.

Detriment to Scalability

As businesses expand and scale their operations, the impact of fraud on their total cost can become increasingly pronounced, yet it often remains overlooked until later stages of growth. What may have initially appeared as manageable losses in the early stages can quickly escalate as the business footprint expands, encompassing a more comprehensive array of transactions, customers and operational complexities.

One of the critical challenges in addressing fraud at scale lies in the evolution of fraud tactics. What may have sufficed as viable point solutions in the initial stages of business development can quickly become inadequate in the face of sophisticated and evolving fraud schemes. The transition from piecemeal fraud prevention measures or outdated legacy systems to a more comprehensive fraud prevention solution is not always straightforward if building a platform internally can entail a complex rip-and-replace process. Such endeavors demand substantial financial investment and stringent planning and execution to ensure minimal disruption to ongoing operations.

Learn how to select the best fraud prevention for your business needs.

Download free guide

Moreover, the pursuit of scalability often necessitates a fundamental shift in mindset, wherein fraud prevention is accorded the same strategic importance as business expansion goals. Comprehensive fraud prevention strategies must seamlessly integrate into the organization’s fabric, aligning with broader scalability initiatives and operational objectives. This entails not merely reacting to instances of fraud as they arise but proactively embedding fraud detection and prevention mechanisms into every facet of the business, from product development to customer acquisition and beyond.

While fraud presents a tangible risk to business operations, it should not deter growth or hamper the organization’s ability to raise capital, increase sales or expand into new markets. Instead, a balanced approach is needed, wherein fraud prevention efforts are harmonized with strategic growth objectives, enabling the organization to realize its full potential while safeguarding against potential risks. By embracing a proactive stance toward fraud prevention – and partnering with an API-first anti-fraud solution that can scale and adapt alongside a company, businesses can navigate the complexities of growth with confidence and resilience.

Rising Concern Among Decision-Makers

The surge in fraud incidents has triggered a notable rise in concern among decision-makers across industries. Yet, this concern is often compounded by a lack of understanding regarding the true extent of risk exposure. As fraudsters continue to innovate and exploit vulnerabilities, decision-makers grapple with the elusive nature of fraud, unsure of how best to fortify their defenses. This uncertainty underscores the critical need for businesses to understand the impact of fraud on their revenue streams.

The statistics paint a stark picture: fraud inflicts substantial financial losses, significantly dragging revenue generation. The Global Economic Crime and Fraud survey, conducted in 2022, reported total losses attributed to fraud at $42 billion. These figures serve as a wake-up call, highlighting the urgent imperative for businesses to bolster their fraud prevention measures and safeguard their bottom lines against the pervasive threat of fraud.

The Need for Better Protection Now

It is no longer sufficient for businesses to react to instances of fraud as they arise; proactive measures must be taken to fortify defenses, mitigate risks preemptively and protect opportunities. This requires a concerted effort to embed fraud prevention mechanisms into every aspect of business operations. As advancements in technology enable fraudsters to commit a greater volume of fraud with unprecedented speed, fighting back with agility and precision entails harnessing the power of the same technologies: AI and machine learning algorithms.

Beyond direct financial losses, fraud inflicts a ripple effect of opportunity costs that undermine operational efficiencies, compromise compliance standards, erode customer trust, and impede scalability. To fully grasp the total cost of online fraud, businesses must acknowledge and account for these indirect consequences, which often exact a more profound toll on organizational viability and reputation.

Sources:

- Fraud isn’t just a security problem, it’s a marketing problem too – Marketing Interactive

- Crowe – Fraud costs the global economy over US$5 trillion

- AccountingToday – Organizations lose 5 percent of revenue to fraud every year

- SecurityMagazine – 80% of global businesses expect a breach of customer records in the next year

- GisReports – Why anti-money laundering policies are failing

- Thomson Reuters – 2023 Cost of Compliance

- PwC’s Global Economic Crime and Fraud Survey 2022