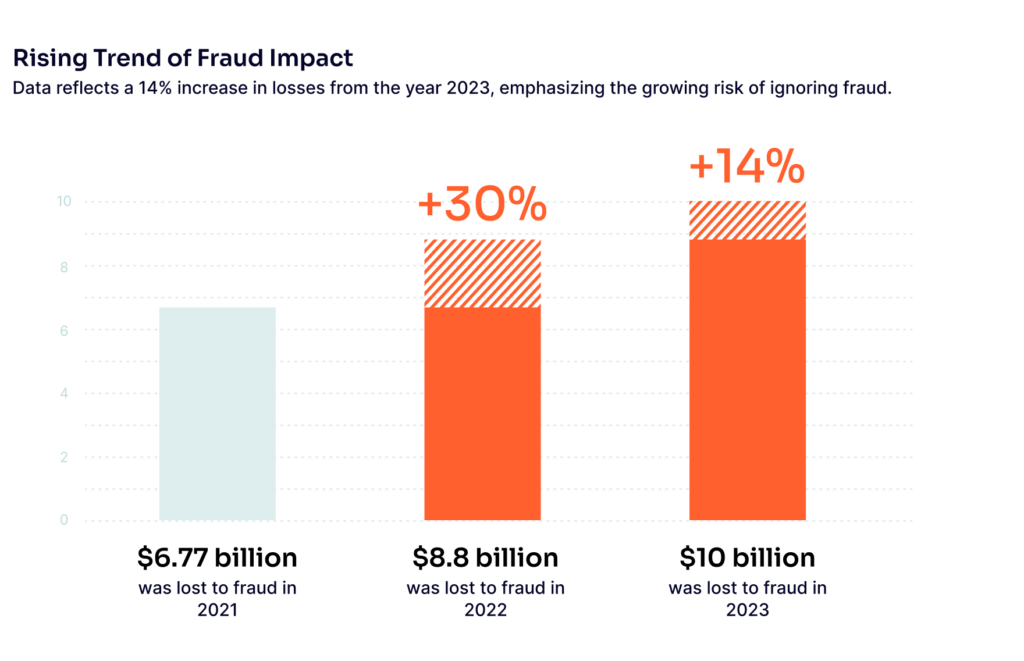

In today’s digital-first world, where online transactions exceed $5 trillion annually, the threat of fraud has reached alarming proportions. In 2023, reported losses exceeded $10 billion due to fraud – a 14% increase from the previous year. These numbers highlight not only the ingenuity of modern fraudsters but also a widespread misconception: too many businesses still view fraud as a one-off occurrence.

Fraud is relentless and adaptive – an ongoing threat that constantly tests businesses’ defenses. Yet many underestimate its far-reaching impact. Ignoring fraud doesn’t just erode a company’s bottom line – it undermines trust, disrupts operational stability and jeopardizes long-term growth. Businesses that fail to confront fraud proactively risk cascading consequences that ripple across every aspect of their operations.

Sources: Federal Trade Commission: As Nationwide Fraud Losses Top $10 Billion in 2023, FTC Steps Up Efforts to Protect the Public & Federal Trade Commission: New FTC Data Show Consumers Reported Losing Nearly $8.8 Billion to Scams in 2022

Explore proactive measures and actionable strategies to combat the most prevalent forms of fraud.

Speak with an Expert

Surveying the Modern Fraud Landscape

The digital transformation of commerce has fundamentally changed how businesses must approach fraud prevention, demanding a shift from static defenses to dynamic, comprehensive strategies. However, an organization’s approach to combatting fraud often depends on its size, resources and operational priorities.

While their scale and visibility make larger companies prime targets for sophisticated fraud schemes, they’ve elevated fraud prevention from an operational concern to a strategic priority. Equipped with dedicated fraud teams and advanced tools, they are better positioned to identify and mitigate risks. Yet their complexity introduces challenges, such as integrating fraud prevention systems seamlessly across global operations and staying ahead of increasingly sophisticated threats.

Mid-sized businesses are typically more aware of fraud risks but can struggle to implement comprehensive defenses. As a result, many rely on fragmented approaches, such as manual reviews or isolated point solutions, which can be inefficient and prone to errors. For these organizations, the key challenge lies in balancing the need for robust fraud defenses with maintaining operational efficiency and customer satisfaction.

Smaller organizations often view fraud as an inevitable cost of doing business rather than a solvable problem. Limited resources usually yield reactive approaches, leaving these businesses vulnerable to repeated attacks. This perspective can lead to costly cycles of loss that compound over time. For many small businesses, overcoming this mindset is the first step toward adopting scalable solutions to mitigate risk without overburdening resources.

The Exponential Business Impacts of Fraud

To understand the actual cost of fraud, businesses must examine its varied and interconnected impacts:

Financial Losses: The Immediate Hit

Fraud’s most tangible impact is the financial strain it imposes on businesses. Beyond the immediate loss of funds, companies face mounting operational expenses to investigate and rectify fraud-related incidents. Over time, these costs snowball, eating into already narrow margins and stalling growth. Many businesses fail to realize that fraud costs go beyond the initial monetary hit with fees imposed by payment processors, lost revenue from declined legitimate transactions and additional expenses tied to reactive measures that create a cascade of financial damage. Addressing and detecting fraud proactively is not just about preventing theft – it’s about preserving the fiscal foundation of the business.

Eroding Customer Trust

A single fraud incident can shatter customer confidence, particularly if personal data is compromised. Customers expect businesses to protect their information, and when companies fall short, the loss of trust can lead to reduced loyalty and lost revenue. In a competitive market, reputation is everything. News of fraud can spread quickly, painting a business as careless or untrustworthy, and once trust is broken, it can take years – and significant resources – to rebuild. For businesses, preventing fraud isn’t just about protecting the bottom line but also safeguarding the relationships underpinning long-term success.

Operational Disruption

Fraud often forces businesses to divert resources from growth-focused initiatives to damage control. Instead, manual reviews, system updates and fraud investigations consume time, staff and budgets that should be spent innovating or expanding. This disruption isn’t just about inefficiency, it’s about opportunity cost. Every hour spent managing fraud is an hour not spent refining products, enhancing customer experience or scaling operations. Over time, this reactive approach stifles progress and limits a company’s ability to compete.

Payment Processor Penalties

Fraud doesn’t just affect businesses; it impacts their relationships with payment processors. As noted, high chargeback rates can lead to increased transaction fees, stricter terms or even the loss of payment processing privileges. For many businesses, these penalties are as damaging as the fraud itself. Payment processors view merchants with high fraud rates as liabilities, and the repercussions are swift. From increased reserve requirements to outright account terminations, businesses that don’t manage fraud risk effectively can be cut off from digital commerce’s lifeblood: payment processing.

Reputational Damage

Reputation is a fragile asset, and fraud can tarnish it in an instant. Whether it’s a data breach, widespread account takeovers or a rash of chargebacks, public perception of a business can shift rapidly. Negative news travels fast, leaving businesses little room for error. For many companies, the reputational fallout from fraud is more challenging to recover from than the financial losses. Customers and partners need to trust that their data and transactions are safe. Without this confidence, even the most innovative products or services can struggle to gain traction.

Compliance and Legal Risks

As data protection and anti-money laundering (AML) regulations grow stricter, failing to prevent fraud can lead to more than just financial penalties. Businesses that fall short of compliance standards face lawsuits, fines and long-term damage to their credibility. Staying ahead of these requirements demands a proactive fraud strategy that aligns with regulatory expectations. The cost of financial and reputational non-compliance is far greater than the investment needed to implement preventive measures.

Stifling Growth as a Long-Term Impact

Fraud doesn’t just affect the present – it jeopardizes the future. Businesses bogged down by fraud-related issues often hesitate to expand into new markets or adopt new technologies, fearing the increased risks. This hesitation stifles innovation and limits opportunities. Companies that fail to address fraud decisively find themselves outpaced by competitors that invest in more thoughtful, scalable fraud prevention strategies. Growth demands confidence, and confidence requires security.

Fraud Prevention is a Strategic Imperative

Fraud is a core challenge that demands immediate, strategic attention from businesses of all sizes. Ignoring its impacts isn’t just shortsighted; it directly threatens a company’s financial stability, reputation and growth potential. As fraud continues to evolve, so too must the defenses against it.

Free up time to concentrate on running your business, not fighting fraud.

Learn More