One question fraud managers get consistently asked: Are we certain our fraud detection tool is the right one?

More often than not, it has to do with the budget. So today, we’ll compare different pricing methods to help you select one that makes sense for your business.

While fraud protection comes in all shapes and sizes, two models tend to be favoured by vendors: micro fees and chargeback guarantee. We’ll describe them in detail and weigh their pros and cons to see which one should work for you.

What Is Chargeback Guarantee?

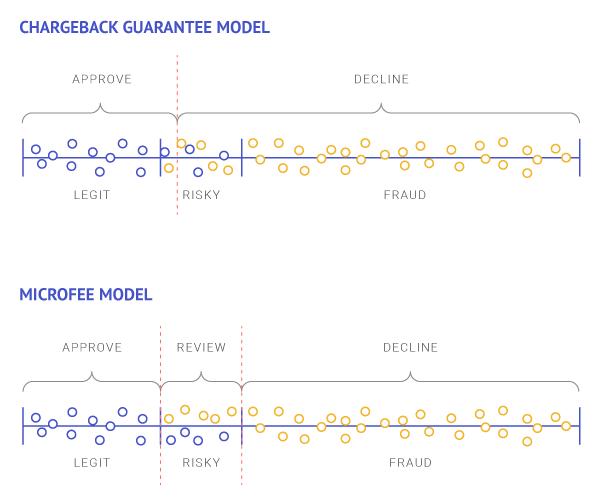

A chargeback guarantee model is one where your management tools offer to pay for chargebacks themselves. They guarantee chargeback protection, and prevent and pay for dispute resolution themselves.

Every online business knows chargebacks are a pain. Disputes regarding credit card purchases are time-consuming, sometimes complex, and incredibly costly. This is why a vendor with a platform who claims to take care of the fees may seem ideal.

Breaking down the process to its bare minimum, this is how it would look:

- You create an account with the vendor’s solutions

- The vendor accepts or denies payments based on analyzed data

- One payment goes through, but the customer asks for a chargeback

- The vendor takes care of losses incurred after chargeback

In short, these management tools are there to relieve you of the expenses, but also the stress associated with them. At least on paper….

Pros of the Model

Because the vendor will provide all the work for the chargeback admin, you won’t need a dedicated fraud team (at least if chargebacks are your main concern over declined orders). This makes the chargeback guarantee model ideal for:

- Small e-commerces

- Retail merchants

- Merchants processing high margin goods or services

- Startups who cannot (or don’t want to) pay for a risk prevention team

The Cons of the Model

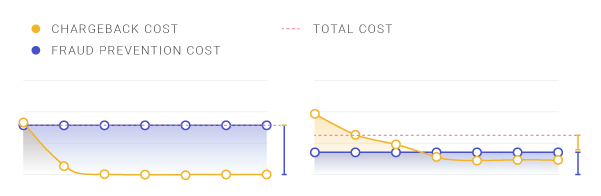

“If your fraud prevention vendor spends fortunes handling chargebacks, they have every incentive to decrease their frequency – even by risking more false positives.”

One of the biggest flaws in the model amounts to a conflict of interest. If your fraud prevention vendor spends fortunes refunding chargebacks, they have every incentive to decrease their frequency – even by risking more false positives.

Why? Because it is in their interest to decline more payments. Put simply, your vendor could very well calibrate their tool to be highly sensitive to low-risk credit card payments – just to protect themselves and to be on the safe side. This means fewer chargebacks, but also fewer sales and fewer profits for your company. Not to mention putting the value of your customers at risk in the long term – who would want to go back to a site that keeps declining their legitimate payments?

Tied to this problem is one of opacity. Vendors who take control over credit card chargebacks have few reasons to be open about their processes. As you lose insight into the mechanisms that govern your business, you are less likely to learn from your mistakes and understand why fraud happens – or how to fight it effectively.

Paying for Fraud Prevention via Micro Fees

Worried about all of the above? Maybe you’ll want to check out the micro fees model for chargeback management. The name is self-explanatory: you pay a small amount for each transaction checked by the risk prevention tool.

These micropayments for chargeback prevention can vary depending on the kind of API request, and most vendors will usually offer a sliding scale based on the number of monthly transactions. However, the average cost per transaction would be around a couple of cents maximum. This is why it’s the preferred model for high-risk merchants and payment service providers.

Pros of the Micro Fees Model

The obvious point – in direct opposition to the other model – is that the fraud detection vendor has 0 incentive to tweak their system behind the scenes. The payment is entirely based on the size and scale of your business.

While it may seem over the top for small businesses, it could end up being cheaper than the alternative. It is also completely transparent, and straightforward. No bad surprises for your budget, and it’s easy to make predictions on your ROI, including chargebacks and friendly fraud, for instance.

Cons of the Micro Fees Model

Paying through micro fees usually means keeping a risk team on call. This can be an additional expense, but worth it for managing manual reviews of potential fraud and friendly fraud. You cannot just rely on the algorithms to do the job – human intelligence is also necessary.

And talking about the system, it will have to be extremely well-calibrated. Rules must be properly defined for friendly fraud and chargebacks. If the engine isn’t set up properly, you could incur some costs that are hard to justify and slowly eat away at your profits.

Micro Fees or Chargeback Guarantee?

As you have probably figured by now, there is no magic bullet when it comes to paying for prevention. If the solution existed, everyone would use the same model. In short, the best solution has a lot to do with your risk aversion and how much you trust the system.

Just keep in mind that in fraud prevention, like with any other SaaS, flexibility and scalability is key. You may see noticeable short term benefits in slashing your chargeback rates, but is it really all you should worry about? How about account takeover and friendly fraud and promo abuse? A good fraud solution should let you pay to tackle all the problems at once.

You might also be interested in: