Double dipping is a widespread example of friendly fraud that can cost businesses dearly in time, goods, and money. It’s also as common with opportunists as with committed fraudsters.

It is estimated that 39% of online shops in the world experienced friendly fraud in 2021 – but that could even be an underestimate, as these figures were self-reported by the merchants. Among these cases, double dipping has been prominent.

What Is a Double Dipping Scam?

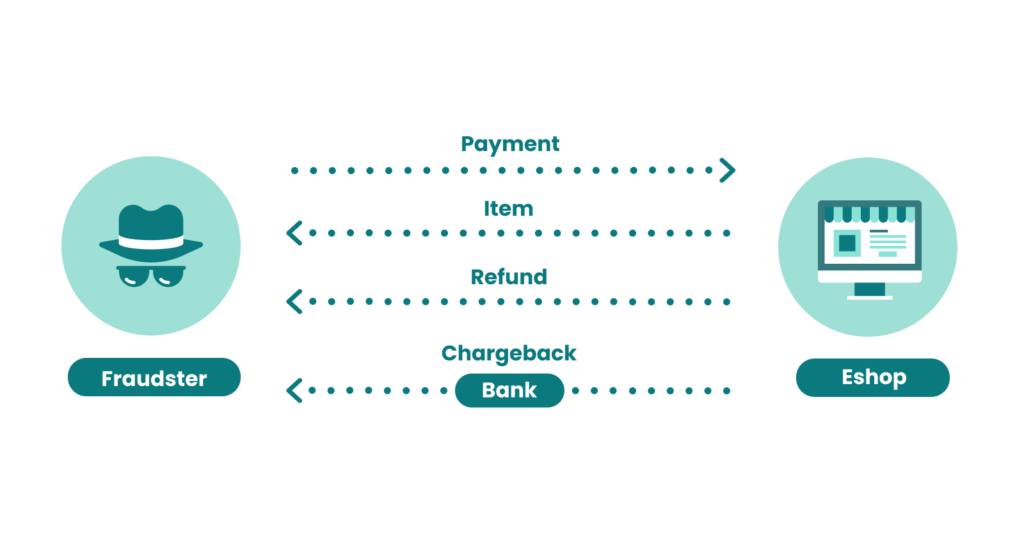

The chargeback-refund double dip is an increasingly prevalent ecommerce scam, which can cause considerable financial losses for affected companies. In short, it refers to various schemes to “have your cake and eat it too”, times two – that is:

- get a refund for an item

- receive a chargeback for the same item

- and also still keep the item

Double dipping in fraud can involve both goods and services. Taking goods as an example, a scammer may order an item and then claim not to have received it.

From there, they request and receive a refund. But at the same time, they put in a request for a chargeback with their card issuing bank, and receive the funds before the merchant has fully caught up.

As you can see, this means that companies can face losses that far exceed the value of the goods or services provided. This is then further compounded by the financial and administrative overhead of dealing with the refunds and chargebacks.

Double dip (or double refund) fraud is surprisingly common and estimated to be involved in around 10% of chargebacks, per MidMetrics.

How Does Double Dipping Work in Fraud?

Double dipping fraud involves a simple set of steps. It’s something that can be done on a large scale by professional fraudsters but is also an example of one-off friendly fraud sometimes committed by otherwise law-abiding individuals.

Here’s how it works:

- Somebody orders an item or service from an online seller.

- They claim that the item was not delivered or that it was faulty. In the case of services, they can claim that they were never provided or were inadequate.

- They complain to the retailer and request a refund.

- They also contact their card issuer and initiate a chargeback request.

The order of the final two steps of the scam can vary, with the fraudster requesting the chargeback or the refund first. In both cases, they take advantage of several weaknesses companies have in tackling this type of fraud:

- It’s often difficult to conclusively prove an item had been delivered – and to the correct place too. Consumer rights tend to place the burden of proof on the supplier.

- Businesses keen to provide good customer service (and avoid negative reviews) often aim to refund with minimal friction, thus asking few, if any, questions. Part of the reason for this is the fear of bad reviews and online ratings directly affecting sales.

- Processing lags between a chargeback request being made and a retailer becoming aware of it can gift a scammer the time needed to pull off a successful double dip.

Is Double Dipping Illegal?

Double dipping is illegal, but the waters are muddy. The scam can often be pulled off in a way that leaves the fraudster with some level of plausible deniability. For example, they can simply claim that they weren’t aware of what exactly was happening or what they were requesting.

Moreover, evidence suggests that consumers (incorrectly) see double dipping as a somewhat acceptable form of friendly fraud. There are several posts online in forums where people ask whether they should “confess” about double refunds. Furthermore, 33.2% of US consumers admit to filing false claims to obtain improper refunds.

So, while double dipping is illegal, it’s a scam that’s falsely seen as a grey area by consumers, and one where it can be difficult to prove the criminal intent.

How Much Does Double Dipping Cost Retailers?

Double dipping can cost retailers sums that far exceed the value of the goods or services provided. As we’ll see in our example below, this is approximately 3.1x the original price the seller paid to procure the item.

Consider a case of double dip fraud on a $500 item sold with a 50% profit margin:

- The retailer pays $250 for the item.

- The customer initially pays $500.

- The retailer sends out the item.

- The customer receives the item but claims it wasn’t received.

- The retailer refunds $500.

- The customer requests the chargeback – which costs the merchant another $500, plus chargeback costs.

| The Seller Receives: | The Seller Pays Out: | |

| Individual sums | $500 (sale price of the item) | $250 (cost price of the “lost” item) $500 refund $500 chargeback refund $25 chargeback costs |

| TOTAL | $500 | $1275 |

| TOTAL LOSS | $1275-$500 = | $775 |

Here, we’re seeing a loss of $775 on an item that cost the merchant $250 to procure. That’s 310% the price of the item – and, of course, this adds up.

Double dip fraud is a problem across all industries and verticals.

In recent years, it’s become a particular issue in the travel industry. Disruption to global travel has resulted in people giving in to the temptation of requesting refunds from both the travel company and the card issuer when plans change or holidays are canceled.

ABTA, The Travel Association, has been working to grow awareness of the issue. As the figures above illustrate, the financial losses are considerable. ABTA says that entire companies are at risk of failure due to the problem.

Moreover, chargeback recovery rates are poor across all varieties of scams. While retailers respond to around 43% of chargebacks, they only succeed in overturning 12%. It is thus better to try to prevent chargebacks before they occur, as well as do your due diligence and keep records of the successful fulfillment of every purchase.

How to Prevent Double Dipping

Implementation of fraud prevention software, be it end-to-end or a stack of various tools, can reduce the risk of double dipping fraud by stopping incidents before they occur.

While some double dip fraud is opportunistic, committed fraudsters will likely take certain steps to evade detection. These can include things like using VPNs and proxies, ordering using throwaway email addresses, and using suspicious delivery addresses.

Thankfully, these are exactly the things that fraud prevention solutions can detect, flagging up when the results of device fingerprinting, behavioral checks, and digital footprint analysis don’t quite fit the right shoe.

Systems can also be used to flag people known to have committed these scams before. Data suggests that people who get away with these activities are nine times more likely to attempt them again.

Ensuring customer service and logistics operations are on point also helps to prevent double dipping and to dispute transactions when it occurs. Ensuring that delivery companies obtain solid proof of delivery is a wise starting point.

When refunds are requested, customer service teams should establish whether the bank has been contacted separately, making it clear that the response is documented. Merely asking the question can serve to deter the more opportunistic double dip scammers.

Finally, solid refund and customer communications documentation has its part to play when it does become necessary to dispute chargebacks.

Friendly fraud may be opportunitistic, but chargebacks can cost up to 3.60x the price of the lost merchandise. Stop them before they happen.

Stop Friendly Fraud